More than 40 years after The Buggles released “Video Killed the Radio Star”, radio is still alive and well.

As Statista’s Felix Richter notes, with all the chatter about about streaming and other digital media, it’s easy to forget how powerful traditional media such as radio and television still are. Radio in particular rarely gets credited for what it still is: a true mass medium.

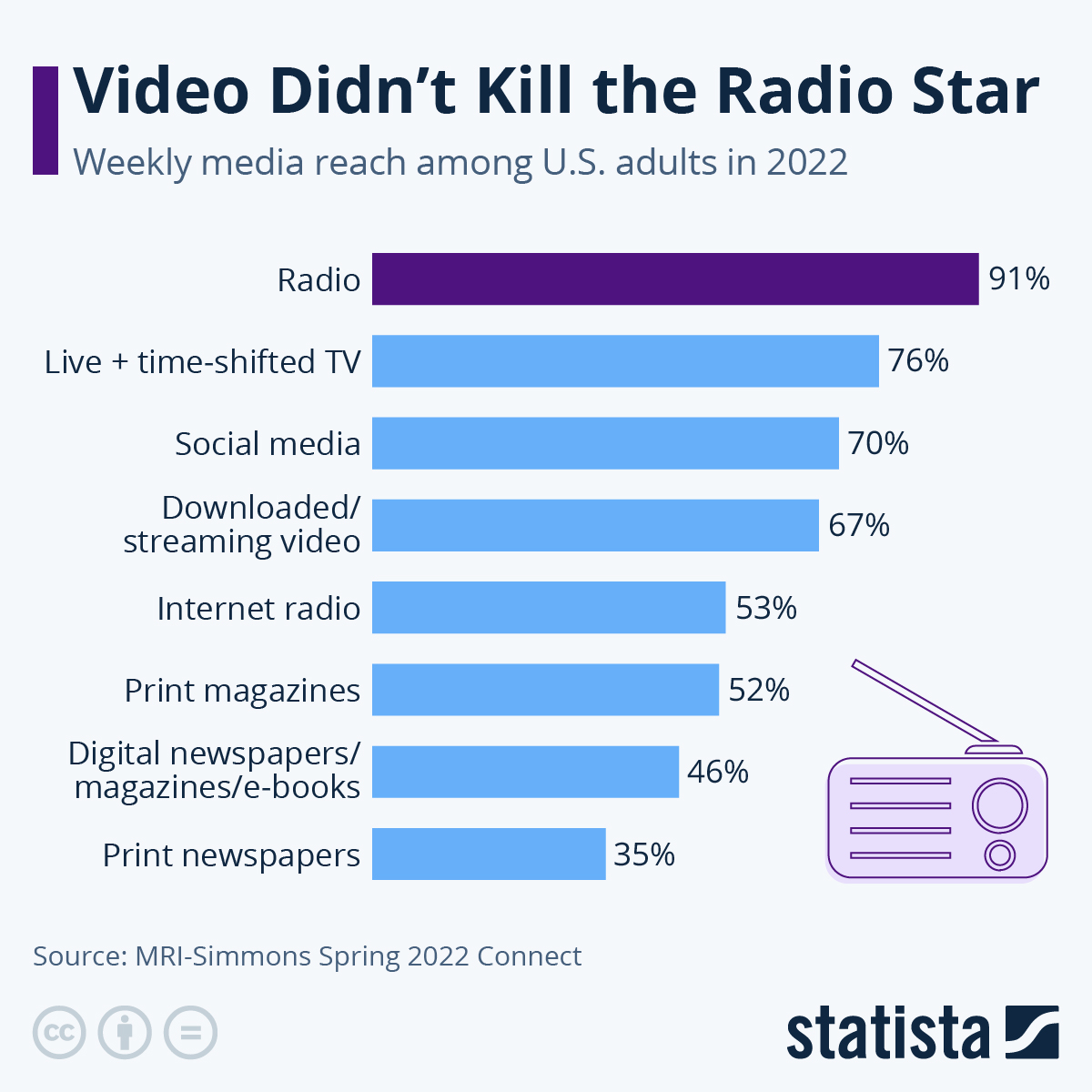

According to MRI-Simmons, radio even trumps TV in terms of its weekly reach among U.S. adults.

According to MRI-Simmons, 91 percent of U.S. adults listen to the radio at least once a week, far exceeding the reach of live and time-shifted TV at 76 percent, social media at 70 percent an online video at 67 percent.

While radio does win in terms of sheer reach, TV remains unparalleled with respect to average daily usage.

According to Nielsen, U.S. adults spent an average of 3 hours and 41 minutes watching live and time-shifted TV in Q3 2020, which is roughly 2.5 times the amount of time they spent listening to the radio (1 hour and 31 minutes).

But if the fear of losing your job hovers over you like a dark cloud, you’re not alone. Nearly 40% of US workers said they “are nervous about being laid off,” a LinkedIn survey of more than 2,000 US employees conducted in December found.

What are the real chances of that happening? To find out, Insider spoke with three experts: Nick Bunker, the head of economic research at Indeed Hiring Lab; Wayne Cascio, an industrial-organizational psychologist at the University of Colorado; and Andrew Flowers, a labor economist at Appcast, the recruitment-advertising technology company. Highlights of what they had to say might help you sleep a little more soundly.

How worried should we be about layoff contagion?

Flowers: Recessions are psychological phenomena. They’re about a loss of confidence in the future.

In the tech sector, there was a collective awareness that companies were operating with a different outlook than they had been previously. Before, growth was the priority and there was lots of optimism — let’s take advantage of low interest rates and hire a bunch of people. That sentiment flipped as the unit economics came under more pressure, along with higher interest rates and more consumer spending on services.

Andrew Flowers is a labor economist at Appcast.Andrew Flowers

As for whether these layoffs spread into other sectors, the risk is not that business leaders will see what’s happening in tech, get spooked, and say, “We need to batten down the hatches and lay off our people, too!” That’s not the channel through which layoff contagion happens.

The risk is if consumers get spooked.

You’re scaring me a little. What happens when consumers get jittery?

Flowers: Over the last year, we’ve seen a disconnect between hard and soft data. The hard data, including GDP, has been relatively strong. But the soft data, including consumer sentiment, which is based on surveys, has been weaker. The fundamentals are good, but the vibes feel off.

Flowers: There’s potential for a recession to become a self-fulfilling prophecy. That could happen if consumers get nervous about the layoffs news. They’ll think, “Maybe I won’t go out to eat. Maybe I won’t buy a new refrigerator.” If their spending falls, the effect on the economy could cause contagion.

Why is there such a disconnect between what the data says about the economy and how we feel about it?

Bunker: I get why people are voicing discontent — inflation is a lot higher than it’s been in the recent past.

But there’s what people say and what they do. They say it’s not great and they complain about it. But they’re still quitting their jobs and going out to dinner. What people are doing is indicative of a strong economy.

And by “people,” do you mean CEOs, too? Are they operating in a way that’s indicative of a strong economy?

Bunker: Unfortunately, I can’t read the mind of the CEOs. Economic growth is slowing down, but there’s still growth.

We could see a rise in layoffs if that takes a hit moving forward. But that would be based on economic growth, not based on what other CEOs are doing.

That’s encouraging. As long as fundamentals stay solid, we’re not all in danger of getting pink slips, right?

Cascio: You don’t need to hit the panic button. In this tight labor market, the demand for talent is high and supply is limited. The last thing enlightened CEOs want to do is cut people when things look like they’re turning south.

So I guess we all should hope we work for an enlightened CEO then?

Cascio: One of the things you want to look at is what your employer did in past downturns. Did they turn to layoffs during the financial crisis? What about in the tech wreck of 2001? Research shows that’s the best predictor of future behavior. If they’ve done it once, they’re going to do it again.

I’ve been doing research on downsizing since the ’90s and one thing is clear: Companies that move quickly to lay off their workers never outperform their competitors in the same field. If companies are doing layoffs to cut costs, there are better ways than cutting people.

Has The Housing Market Bottomed? The Surprising Result From A Little-Known Market Indicator

by Tyler Durden

Monday, Jan 30, 2023 – 03:20 PM

It may come as a bit of a shock to those who have been following the creeping freeze in housing transactions as the bid-ask spread grows to monstrous proportions, leading to a record crash in pending home sales…

… but even though mortgage rates ticked higher back to 6% in January, there is growing speculation that the housing market has bottomed. Why? Because as Goldman’s Rich Provorotsky notes, “bet you didn’t know there were housing price futures…they bottomed in Q4 and have been rallying.” Indeed, the Housing Composite Index traded on the CME is up decidedly in the past month after hitting a 16 month low in November.

Why this surprising bounce? A big reason for the unexpected rebound may be a recent report from real estate company Redfin which last Wednesday reported that “the housing market has begun to recover from a trough in the second week of November with buyers returning at a faster pace than sellers. The number of Redfin customers asking for first tours has improved by 17 percentage points from the November low, and the number of clients contacting.”

Furthermore, according to the report, Redfin agents to begin the home-buying process has improved by 13 points: “I’ve seen more homes go under contract this month than in the entire fourth quarter,” Angela Langone, a San Jose, California, agent, said in the report.

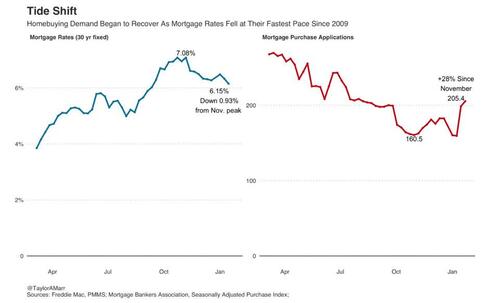

Among notable market moves, Redfin points to mortgage applications which are up 28% from early November as the average 30-year-fixed mortgage rate has dropped to 6.15% from its peak of 7.08% in November, the biggest decline since 2009. Pending home sales rose 3% in December from November.

Preliminary data on the share of Redfin agents’ offers facing bidding wars points to small upticks in the Seattle and Tampa markets this month (however, since this is an uneven trend, expect it to take some time before bidding wars nationally show an upward trend).

“Bidding wars are back in Seattle,” said local Redfin real estate agent Shoshana Godwin. “One of our Issaquah listings got 12 offers and is under contract for $155,000 over the $1.4 million list price. The buyer waived every contingency, handed over $300,000 of earnest money and is letting the seller stay for free for two months after closing. Another home in Seattle’s popular Ballard neighborhood was recently delisted after sitting on the market for over three months. The seller relisted it last week and it went pending in under a day.”

Eric Auciello, Redfin’s team manager in Tampa, has seen three modest single-family homes priced around $300,000 wind up in bidding wars in central Florida this month, with 16, 17 and 23 competing offers, respectively.

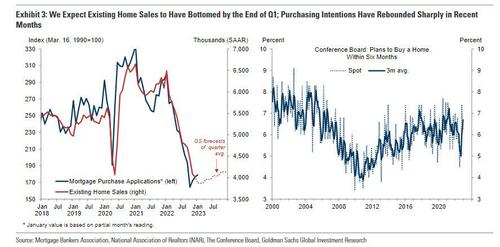

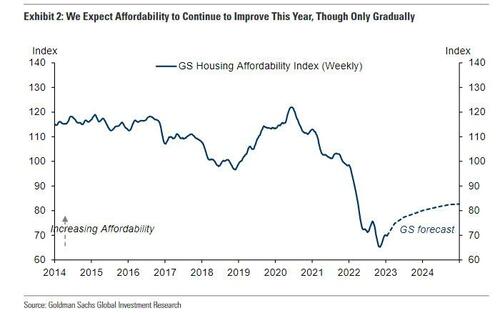

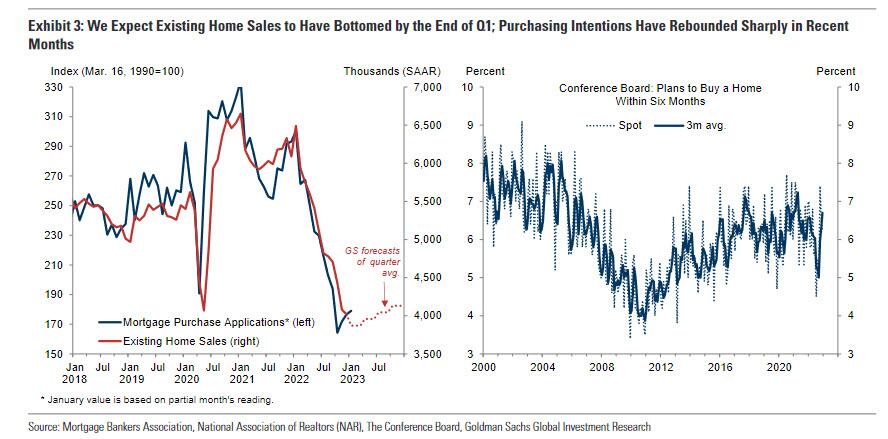

But while one can accuse Redfin of bias – after all the company recently laid off some 13% of its employees due to the housing market collapse so it is certainly interested in sparking some animal spirits in the sector – it is not alone in predicting a housing recovery. One week ago, Goldman’s Jan Hatzius published the bank’s Housing Outlook for 2023 in which he predicted that “home sales appear set to turn higher.” That’s because “mortgage purchase applications have averaged 9% above their October trough so far in January and survey-based measures of purchasing intentions have rebounded sharply” and while Goldman expects that existing home sales could decline slightly further “but will likely bottom in Q1 (GS forecast: Q1 average of 3.85mn saar vs. 4.02mn in December) before rebounding modestly by year-end (GS forecast: Q4 average of 4.1mn).”

Here are some more observations from the Goldman note (full report available to pro subs):

We forecast that housing starts will take longer to stabilize, declining to a trough pace of 1¼mn in 2023Q4 (vs. 1.4mn in 2022Q4) before recovering next year. We expect completions to total 1½mn this year, the most since 2007, which will help to clear the backlog of homes under construction and contribute to a modest increase in the homeowner vacancy rate (GS forecast of 1.2% in 2023Q4 vs. 0.9% now and 1.4% in 2019Q4).

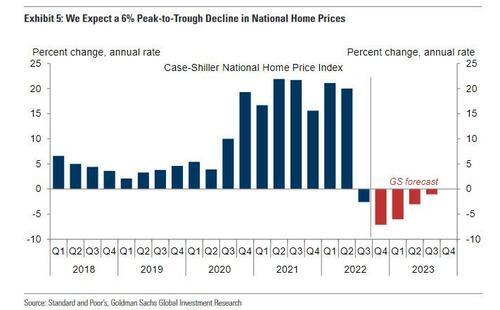

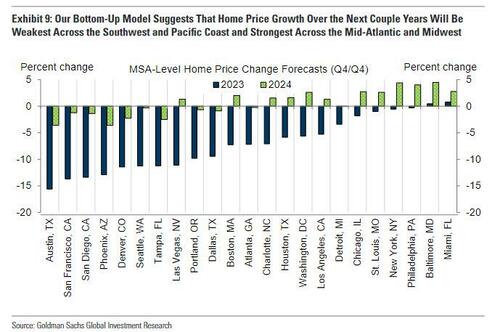

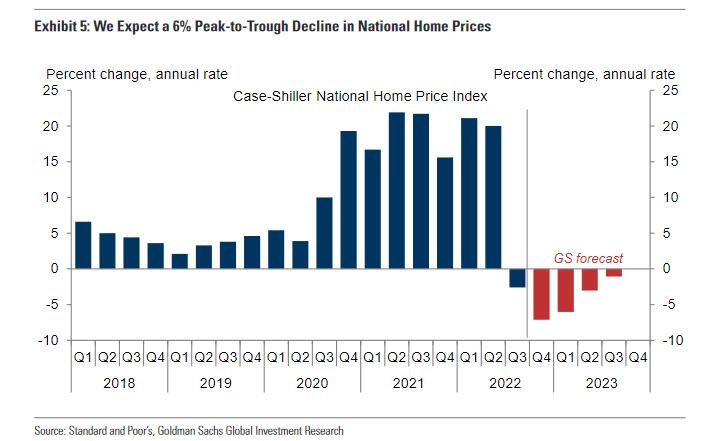

We expect a peak-to-trough decline in national home prices of roughly 6% and for prices to stop declining around mid-year.

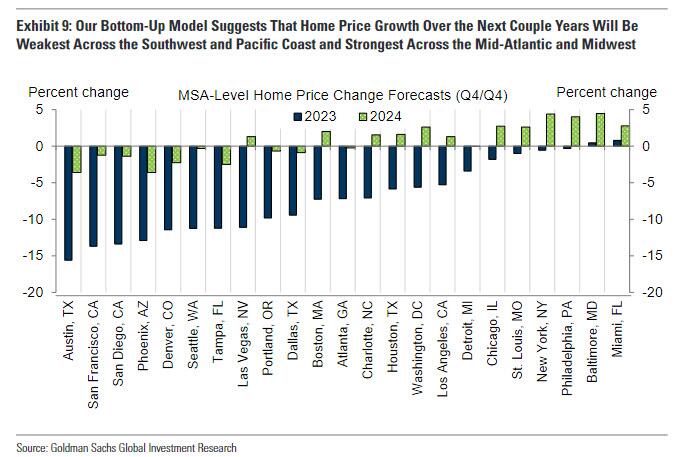

On a regional basis, we project larger declines across the Pacific Coast and Southwest regions—which have seen the largest increases in inventory on average—and more modest declines across the Mid-Atlantic and Midwest—which have maintained greater affordability over the past couple years.

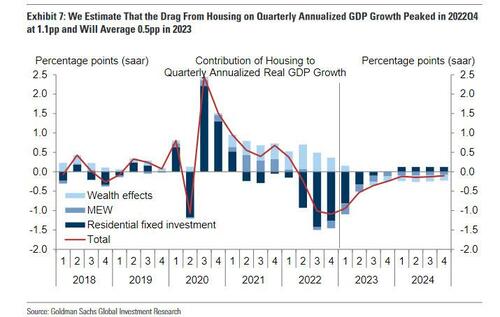

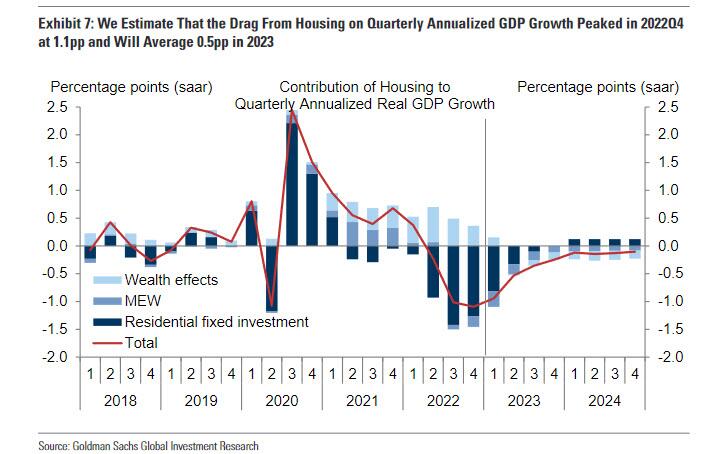

Higher rates and lower home prices will increase the drag on GDP growth from negative wealth effects and declining mortgage equity withdrawal, but we believe that the aggregate drag on GDP growth from the housing sector peaked in 2022Q4 at 1.1pp and will moderate to just 0.25pp by 2023Q4.

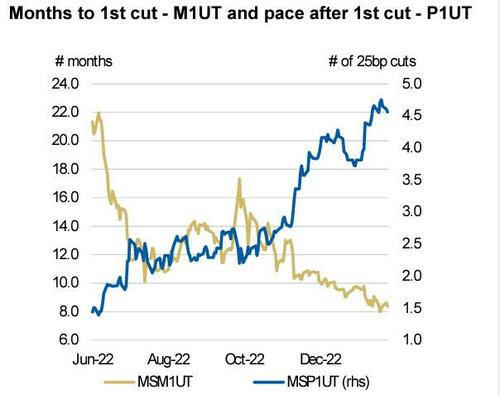

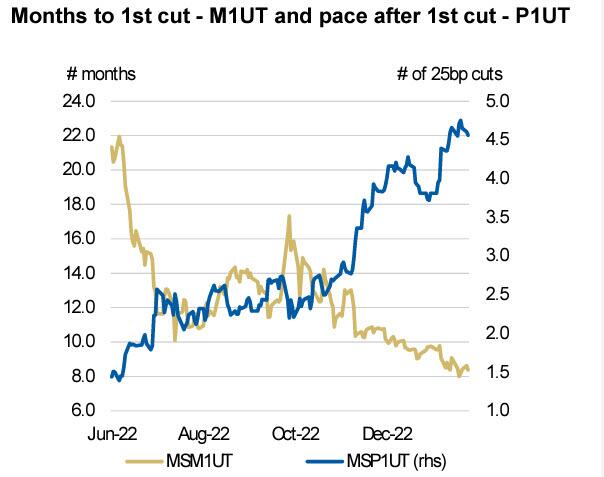

If the housing price futures market – and Goldman – is right in pricing in a housing trough than the consequences could confound markets: on one hand, a stabilization in housing will likely make any coming recession less severe; on the other, since housing is the primary channel by which the Fed can slowdown the economy, any failure to cripple this key US asset, could mean that Powell will be stuck in a “higher for longer” mode for, well, longer than the market expects. As a reminder, as the following Morgan Stanley chart shows, consensus is that the Fed is about 8 months away from its first rate cut, which will be promptly followed by ~4.5 25bps rate cuts.

Manufacturers accepted 57,300 trailer orders in December, the second-highest monthly total since tracking began in 1996. (Photo: Jim Allen/FreightWaves)

Trailer manufacturers posted 57,300 orders in December, the second-highest monthly intake since ACT Research began tracking in 1996. The volume appeared to be a catch-up after OEMs blocked many orders from April to August because they lacked pricing visibility.

“I cannot speak for other OEMs. However, our higher booking in December was driven by the later opening of the order books as we awaited required quoting information from the supply base,” Sean Kenney, chief sales officer for Hyundai Translead, told FreightWaves.

“Hyundai Translead is anticipating continued higher-than-normal orders for the next few months as we work through the impact of this.”

Trailer orders in December 2022 came in at the second-highest volume since ACT Research began tracking in 1996. (Chart: ACT Research)

December net U.S. trailer orders came in 46% higher compared to November and 115% above December 2021, ACT Research reported. The highest month on record was September 2018, with 57,800 net orders.

Some manufacturers report that the supply of parts has deteriorated despite their acceptance of the huge number of December orders.

Lingering supply chain concerns for future trailer orders

“Supply-chain concerns still linger,” with no short-term improvement in sight, Jennifer McNealy, ACT director of commercial vehicle market research and publications, said in a news release. “Regarding demand, most trailer makers continue to see demand exceeding capacity through the end of 2023.”

One major OEM, Wabash, announced a long-term supply agreement Jan. 10 with J.B. Hunt Transport covering up to 15,000 trailers over the next few years.

Some OEMs mentioned an erosion in confidence to ACT, but so far it is not showing up in order cancellations.

Mike Baudendistel, a FreightWaves market expert, expressed surprise at the order volume in December.

“It could be some makeup orders to compensate for the supply constraints the past couple years,” he said. “I would think the orders were even more heavily weighted toward the large enterprise carriers than they usually are since they are well capitalized and their business holds up better in a weakening market.”

Total net orders placed in 2022 were 361,500 compared to 249,400 in 2021. The industry produced approximately 306,000 trailers in 2022.

“Our projections point to a continuation of that upward trend into 2023,” McNealy said.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}