Urethane Blog

Analyst Overview of Tempur Sealy

July 2, 2015

Tempur Sealy International (NYSE:TPX) is a beginning-to-end distributor of bedding products. The company manufactures, markets, and distributes its products globally under some of the most renowned names in the industry, including Tempur-Pedic, Sealy, Posturpedic, and Stearns & Foster. While most readers are most familiar with its retail operations that you'll find in furniture and department stores, the company has also developed its direct-selling program (e-commerce, company-owned stores) and its sales to commercial users (hospitality and healthcare).

From an industry perspective, trends remain strong. Consumers over the years have begun to place more emphasis on sleep quality, driving average selling prices up. Likewise, American consumers continue to follow the "bigger is better" mantra, with sales of king/queen size beds to be the leading drivers of growth for the company. The mattress industry has also pushed the "replace your mattress every eight years" mantra, driving up replacement rates causing a steady stream of recurring revenue for the industry.

Tempur Sealy also has room to grow internationally, with 73% of sales currently coming from North America. The international market is more highly fragmented and in many countries growing faster than North American markets. Countries like Brazil, Mexico, and Japan are likely to be key markets for the company in the future.

Erosion of Margins, Stagnant Sales

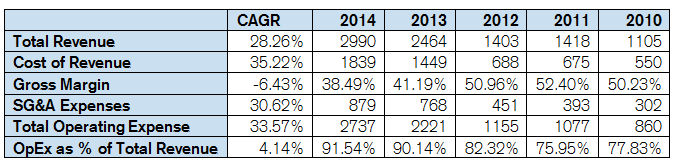

(click to enlarge)

Tempur Sealy, as it stands today, was formed by the acquisition of Sealy Corporation in 2013 for $1.3B. At the time, this was pushed as a merger of two iconic brands. Sealy's strength in innerspring mattresses would complement Tempur-Pedic's prowess in non-traditional mattress design. Annual cost synergies expected to total $40M/year by fiscal 2015.

From the income statement, we can see that there has definitely been improvement in SG&A expenses post-merger. Pre-merger Tempur-Pedic International devoted 32% of revenue to SG&A expenses; currently the figure stands at 29% post-merger due to synergies and general benefits of increased scale. However, Sealy's innerspring mattresses always traditionally carried much lower margins than those found in the Tempur-Pedic brand. In 2013, gross margins took a tumble as results were consolidated and have continued their downtrend since then. In addition to a less favorable mix, consolidation and increased competition within the industry beyond this tie-up has led to margin pressures industry-wide. Investors shouldn't expect this trend to abate. Tempur Sealy has targeted margin expansion through cost cuts, but I don't know how much it can squeeze out of the process without impacting quality and potentially impacting consumer confidence in its core brands.

What this all means is that after interest expenses associated with the acquisition (total debt now stands at $1.6B and the company paid $92M in interest expenses in 2014), net income has barely budged. Net income was $109M in 2014 compared to $107M in 2012. These results are likely not what shareholders had in mind with this tie-up. Increased leverage through the acquisition has thus far not led to any additional net income generation.

On a segment basis, Sealy has been the performer from a revenue standpoint, further contributing to margin pressure based on a less favorable mix. Tempur-Pedic brand sales have been relatively poor over the past few years as competition has increased in non-innerspring markets, pressuring margins and stunting sales growth. Unfortunately, management is getting rid of these reporting segments in 2015, breaking sales down only by North America and International. We will lose this visibility going forward.

http://seekingalpha.com/article/3298755-tempur-sealy-investors-should-remain-concerned?auth_param=7a357:1ap9oo4:f71505a28f6bd80272ac637cf4609485&uprof=25