Epoxy

April 18, 2024

Trade Action on Epoxy Resin

Olin Among U.S. Epoxy Resin Producers Filing Trade Cases Against Five Countries

News provided by Olin Corporation

Apr 03, 2024, 16:05 ET

CLAYTON, Mo., April 3, 2024 /PRNewswire/ — Olin Corporation (NYSE: OLN) today announced the filing of antidumping and countervailing duty petitions against five countries related to certain epoxy resins, as part of the U.S. Epoxy Resin Producers Ad Hoc Coalition. The petitions charge that unfairly traded imports of certain epoxy resins from China, India, South Korea, Taiwan, and Thailand are causing material injury to the domestic epoxy resin industry. The petitions further charge that significant subsidies have been provided to the foreign producers by the governments of China, India, South Korea, and Taiwan. The U.S. producers in the Coalition, including Olin, produce epoxy resins, an essential component for which there are no practical substitutes, for various customer applications, including critical U.S. industries such as Aerospace, Automotive, Defense, Electrical Transmission, Semiconductors, and Wind Energy. Having domestically produced epoxy resins is vital to ensuring that the U.S. manufacturing industry is capable of meeting domestic preference requirements contained in important U.S. legislation like The Inflation Reduction Act (IRA), the Bipartisan Infrastructure Law, and the CHIPS and Science Act. The availability of domestic epoxy production is also important to ensure U.S. industry has supply chain resiliency.

“We have been facing a significant volume of what we believe are unfairly dumped and subsidized imports of epoxy resin into this country,” said Florian Kohl, President, Olin Epoxy. “These unfairly traded imports have seriously impacted pricing in the U.S. market, which has resulted in a significant negative effect on our production, sales, and earnings. Without relief under U.S. law, unfairly traded imports will undermine the sustainability of U.S. producers and the welfare of their workers and local communities.”

The petitions were filed today with the U.S. Department of Commerce (“Commerce Department”) and the U.S. International Trade Commission (“USITC”). The five countries covered by the antidumping petitions and the dumping margins alleged by the domestic industry are as follows:

| COUNTRY | DUMPING MARGINS ALLEGED |

| China | 264.87% – 351.97% |

| India | 11.43% – 17.50% |

| South Korea | 30.01% – 69.42% |

| Taiwan | 87.19% – 136.02% |

| Thailand | 163.94% – 205.63% |

The petitions also allege that the foreign producers benefit from numerous countervailable subsidies. The petitions were filed in response to large volumes of low-priced imports of epoxy resins from the subject countries over the past three years that have injured the domestic epoxy resin producers.

The petitions allege that producers in the subject countries have injured the U.S. epoxy resin producers by selling their products at unfairly low prices that significantly undercut the prices of U.S. producers. As a result, imports of epoxy resins have captured an increasing share of the U.S. market at the direct expense of the U.S. industry. The price declines that U.S. producers have suffered are likely to continue if duties are not imposed to level the playing field.

Antidumping duties are intended to offset the amount by which a product is sold at less than fair value, or “dumped,” in the United States. The margin of dumping is calculated by the Commerce Department. Estimated duties in the amount of the dumping are collected from importers at the time of importation. Countervailing duties are intended to offset unfair subsidies that are provided by foreign governments and benefit the production of a particular good. The USITC, an independent agency, will determine whether the domestic industry is materially injured or threatened with material injury by reason of the unfairly traded imports.

OLIN COMPANY DESCRIPTION

Olin Corporation is a leading vertically integrated global manufacturer and distributor of chemical products and a leading U.S. manufacturer of ammunition. The chemical products produced include chlorine, caustic soda, vinyls, epoxies, chlorinated organics, bleach, hydrogen, and hydrochloric acid. Winchester’s principal manufacturing facilities produce and distribute sporting ammunition, law enforcement ammunition, reloading components, small caliber military ammunition and components, industrial cartridges, and clay targets.

April 4, 2024

Arsenal Exits Seal for Life Platform with Sale to Henkel

Arsenal Completes Sale of Seal For Life to Henkel

PR Newswire

Thu, Apr 4, 2024, 8:45 AM EDT3 min read

NEW YORK, April 4, 2024 /PRNewswire/ — Arsenal Capital Partners (“Arsenal”), a private equity firm that specializes in investments in industrial and healthcare companies, announced today it has sold its portfolio company, Seal For Life Industries LLC (“Seal For Life”), to Henkel AG & Co. KGaA (“Henkel”), a publicly traded German manufacturer of industrial and consumer products. The terms of the transaction were not disclosed.

Seal For Life is a specialized supplier of protective coating and sealing solutions for a broad variety of infrastructure markets such as renewable energy, oil & gas, and water. The company employs more than 650 people and has a global production network. Seal For Life offers innovative coating and sealing products such as heat-shrink sleeves, visco-elastic coatings, epoxy & urethane coatings, fire protection, insulation, and sound dampening coatings. The performance and application capabilities of these solutions, marketed under different industry-leading brands including STOPAQ®, CANUSA®, COVALENCE®, and LIFELAST®, are pioneering in the protection and retrofitting of a wide variety of customer infrastructure assets, including onshore and offshore pipelines, jetty piles, storage tanks, valves, flanges, and high- performance industrial flooring.

Arsenal completed its investment in Seal For Life in 2019 and through seven strategic acquisitions, built a global platform in innovative coating and sealing solutions for both existing and new build infrastructure assets. The company’s leading brands and technologies play a critical role in extending the asset life of aging infrastructure with a focus on sustainable materials. During Arsenal’s ownership, Seal For Life significantly invested in technology development and innovation as well as expanded its end market exposure with novel solutions into applications such as district energy and renewable applications for wind and solar infrastructure protection.

Sal Gagliardo, an Operating Partner of Arsenal, said, “We are delighted with the growth achieved during our ownership, with Seal For Life’s sales more than doubling and strengthening of the company’s global market position. Seal For Life’s team, led by Jeff Oravitz, achieved strong organic growth, completed and integrated complementary acquisitions, and created a best-in-class technology platform in the infrastructure coatings sector. We want to thank Jeff and the Seal For Life team for their efforts and leadership that drove to this successful outcome.”

Jeff Oravitz, CEO of Seal For Life, stated, “Arsenal has enabled the transformation of Seal For Life into a unique platform of coatings solutions. The firm brought significant expertise in technologies and applications that drove a focus on where the markets are going and how we can address the long-term trends. We are grateful to the Arsenal team for their partnership and support over the last five years and are excited for the growth opportunities as we join the Henkel organization.”

Roy Seroussi, an Investment Partner of Arsenal, commented, “Arsenal’s close collaboration with Jeff and the team and the success of the Seal For Life platform further strengthens Arsenal’s position as a leading investor and company builder in the coatings, adhesives, sealants, and elastomers sector. We wish the Seal For Life team and Henkel the very best in their future success.”

Arsenal is an active investor in the coatings, adhesives, sealants, and elastomers sector, with current investments including Applied Adhesives, ATP Tapes, Fenzi Group, Meridian Adhesives Group, Polycorp, and Polytek, and with several prior investments in this sector.

J.P. Morgan Securities LLC acted as financial advisor to Seal For Life and Kirkland & Ellis LLP served as legal counsel.

About Arsenal Capital Partners

Arsenal Capital Partners is a leading private equity firm that specializes in investments in industrial growth and healthcare companies. Since its inception in 2000, Arsenal has raised institutional equity investment funds totaling over $10 billion, completed more than 290 platform and add-on acquisitions, and achieved more than 35 realizations. The firm works with management teams to build strategically important companies with leading market positions, high growth, and high value-add. For more information, visit www.arsenalcapital.com.

https://finance.yahoo.com/news/arsenal-completes-sale-seal-life-124500648.html

March 13, 2024

DCM Shriram to Build Epoxy Resin Plant in India

DCM Shriram to invest Rs1,000 crore in epoxy resin plant

The diversified agricultural company DCM Shriram plans to invest Rs 1,000 crore in the next few years to build a greenfield plant that will produce epoxy resin.

The Board of the company has given its chemical division permission to invest in epoxy and other value-added products as a means of expanding into advanced materials. Furthermore, their epichlorohydrin (ECH) factory in Jhagadia, Gujarat, is almost finished and should be active in the first quarter of the 2024–2025 fiscal year.

With essential raw materials like caustic and ECH already in its inventory, the company is well-positioned to penetrate the market for value-added and epoxy products. The company is already well-known in a number of industries, such as value-added (fenesta building systems-UPVC windows & doors), agri-rural, and chloro-vinyl.

Additionally, the extensive line of advanced materials products, which includes solvent cuts, hardeners, formulated resins, liquid epoxy resins, and reactive diluents, is ready to serve a variety of industries, including electronics, wind-blades, electric vehicles (EVs), electronics, fire-proofing, and lightweighting.

We remind, Shriram Fertilizers & Chemicals (SFC), a unit of DCM Shriram Ltd. and the third largest chlor-alkali producer in India, will use Topsoe’s ClearView solution for digitalizing its ammonia plant. The digital platform was operational in early 2022.

DCM Shriram Ltd is a diversified Indian conglomerate whose business portfolio spans across multiple sectors including Agri-business – Urea, Sugar, Ethanol, Farm Solution Business covering the entire range of inputs, R&D based Hybrid Seeds. Chlor-Vinyl Business – Caustic Soda, Chlorine, Aluminum Chloride, Calcium Carbide, PVC Resins, PVC Compounds, Power and Cement. And Value Added Business Fenesta Building Systems makes UPVC and Aluminium Windows & Doors. Chemicals is one of the company’s largest businesses and is expected to continue as one of the key growth drivers for the company, it said.

Furthermore, the company board of directors have inter-alia declared an interim dividend for the financial year 2023-24 on the paid-up equity share capital of the company, at 200 per cent (Rs 4 per equity share of face value of Rs 2 each). The record date fixed for the purpose of the said interim dividend shall be March 6, 2024.

February 19, 2024

A Familiar Name in Urethanes Now New CEO of Olin

Olin taps LyondellBasell executive Lane as new President/CEO, succeeding Sutton

Feb. 19, 2024 8:14 PM ETOlin Corporation (OLN) StockLYBBy: Carl Surran, SA News Editor

Olin (NYSE:OLN) said Monday it named LyondellBaseel (LYB) executive Kenneth Lane as its new President and CEO effective March 18, when Scott Sutton will step down from those positions; no explanation was given for Sutton’s departure.

Lane was Executive VP of Global Olefins and Polyolefins at LyondellBasell (LYB), which he joined in 2019 after serving BASF for 13 years and holding executive positions across a wide range of businesses including Polyurethanes, Monomers and Catalysts; previously, he had spent time at BP Chemicals and Amoco Chemical.

Kim Foley will assume Lane’s previous role at LyondellBasell (LYB) after serving as Senior VP of Global Engineering, Turnarounds and Health, Safety and Environment.

February 6, 2024

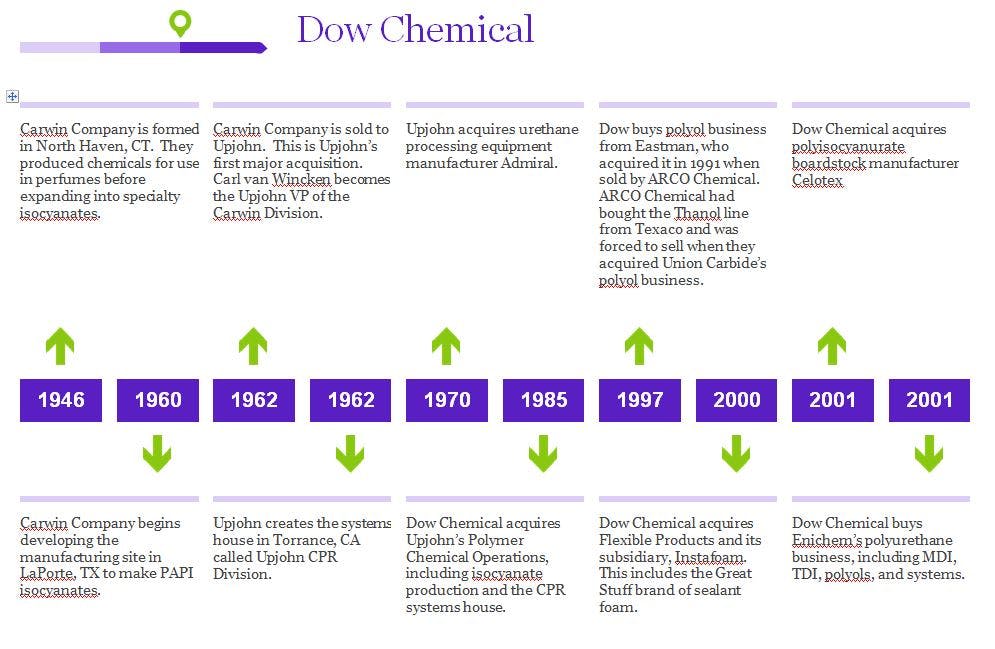

Dow Chemical Urethane History Part I