Urethane Blog

Upbeat Economic News

August 15, 2019

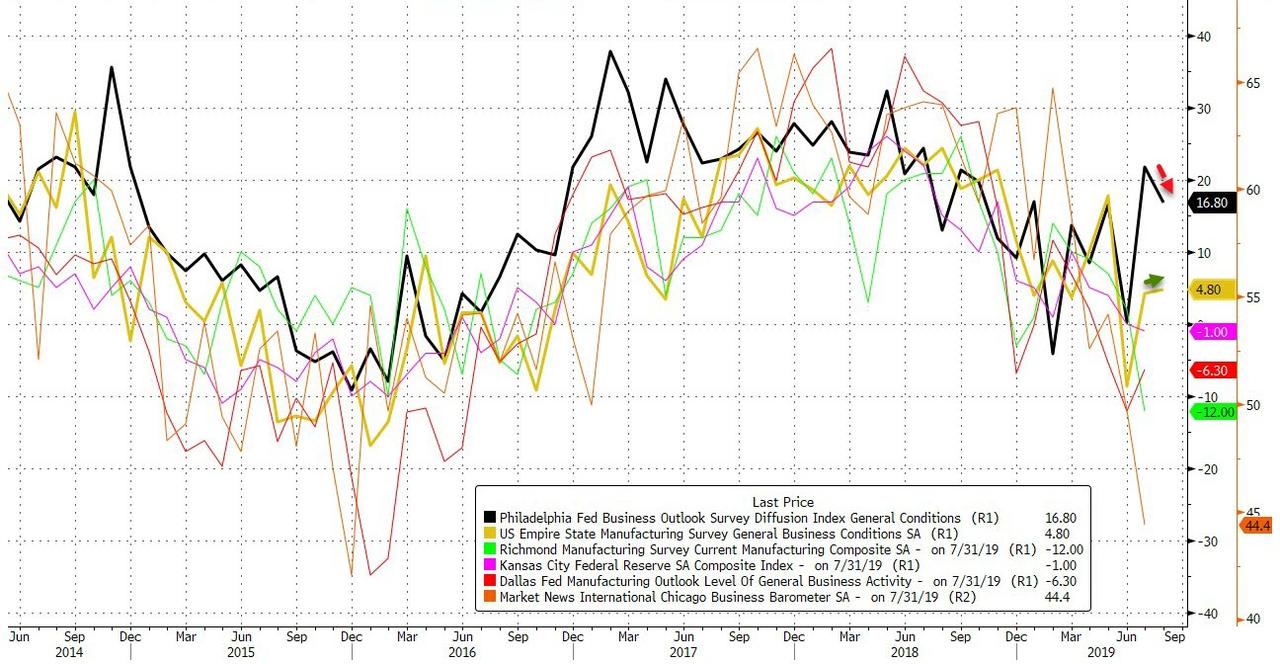

Philly, Empire Fed Beat Expectations, Confirming Economic Rebound

Following an unexpectedly strong retail sales report which saw a solid, 0.9% increase in sales ex autos and gas, almost double the 0.5% expected, we got further confirmation the US economy may be rebounding thanks to both the Philly and New York Fed, both of which printed well above expectations.

- Empire Manufacturing (NY) Fed August: 4.8. up from 4.3, and well above the 2.0% expected.

- Philadelphia Fed Business Outlook August: 16.8, down from 21.8 but also well above the 9.5% expected.

Commenting on the latest Philadelphia Fed, the survey organizers said that manufacturing activity in the region continued to grow, with “general activity, shipments, and employment indicators decreased from their readings last month, but the indicator for new orders increased.” The survey’s future activity indexes remained positive, suggesting continued optimism about growth for the next six months.

- The diffusion index for current general activity fell 5 points this month to 16.8, after increasing 22 points in July. Movements in the indexes for current shipments and new orders were mixed: The current new orders index increased 7 points, while the shipments index decreased 6 points. Both the unfilled orders and delivery times indexes remained positive this month, suggesting higher unfilled orders and slower delivery times.

- The firms continued to report increases in the prices paid for inputs. The percentage of firms reporting increases in input prices (25 percent) remained higher than the percentage reporting decreases (12 percent). The prices paid diffusion index decreased 3 points and remains well below readings over the past two and a half years. The current prices received index, reflecting the manufacturers’ own prices, increased 4 points to a reading of 13.0 but is also still well below readings of the past few years.

Meanwhile, the Empire Fed was even more optimistic, noting that “new orders increased after declining for the prior two months, and shipments continued to expand. Unfilled orders fell, delivery times were steady, and inventories increased.” On the other hand, the employment and average workweek indexes were both slightly below zero, pointing to sluggishness in labor market conditions. Input prices increased at a slightly slower pace than last month, and selling price increases were little changed. Some more details:

- Manufacturing firms in New York State reported that business activity grew modestly in August. The general business conditions index was little changed at 4.8, pointing to two months of modest growth after a brief decline in activity in June. Twenty-seven percent of respondents reported that conditions had improved over the month, while 22 percent reported that conditions had worsened. The new orders index climbed above zero, and at 6.7, indicated that orders increased. The shipments index moved slightly higher to 9.3, pointing to an increase in shipments. Unfilled orders declined for a third consecutive month. Delivery times were steady, and inventories rose for the first time since April.

- The index for number of employees held below zero for a third consecutive month, coming in at -1.6, and the average workweek index was -1.3, pointing to ongoing sluggishness in employment levels and hours worked. The prices paid index edged down two points to 23.2, suggesting a slightly slower pace of input price increases than last month. The prices received index was little changed at 4.5, with selling price increases maintaining a modest pace.

Where the news was less good was in the outlook, with indexes assessing the six-month outlook suggesting that firms were somewhat less optimistic about future conditions than they were last month. The index for future business conditions fell five points to 25.7, and the index for future new orders also moved lower.

The bottom line: the barrage of economic data today – from the beat in productivity and retail sales, to the stronger than expected Philly and Empire Fed indexes – suggest that the Fed may have a tough time pushing for a 50bps rate cut, or even a 25bps, absent a dramatic deterioration in financial conditions and/or further escalation in trade war.

Which probably explains why US futures are unable to decide what to do with today’s strong economic data, and if anything have drifted lower.

https://www.zerohedge.com/news/2019-08-15/philly-empire-fed-beat-expectations-confirming-economic-rebound