Epoxy

March 21, 2023

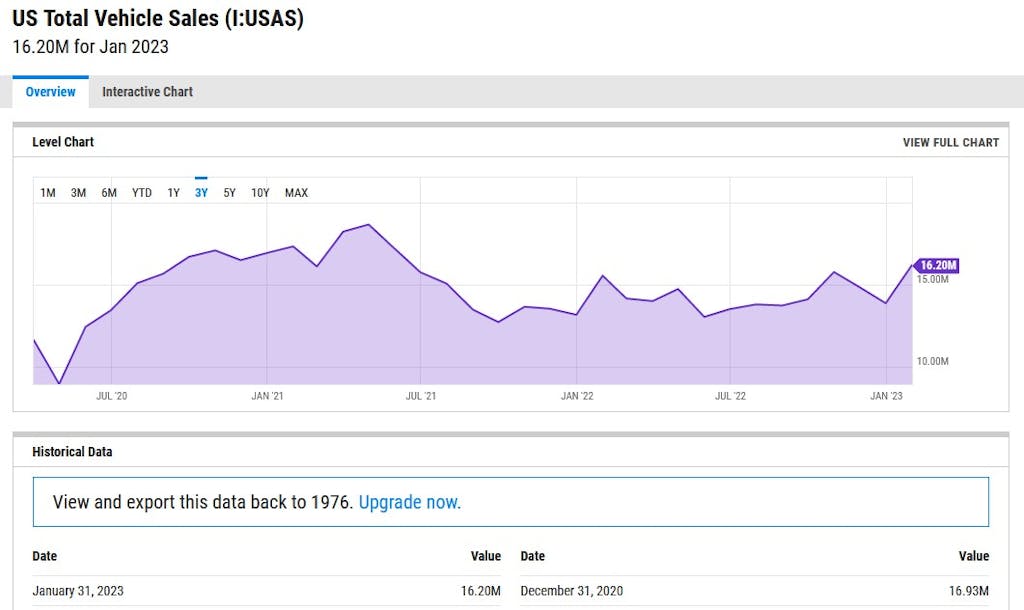

Auto Sales Rebound in January

March 14, 2023

Univar Solutions Going Private

Univar Solutions to be Acquired by Apollo Funds for

$8.1 Billion

3/14/2023

Shareholders to Receive $36.15 Per Share in Cash

DOWNERS GROVE, Ill. and NEW YORK, March 14, 2023 /CNW/ — Univar Solutions Inc. (NYSE: UNVR) (“Univar

Solutions” or the “Company”) and Apollo (NYSE: APO) announced today that funds managed by affiliates of Apollo

(the “Apollo Funds”) have entered into a definitive merger agreement to acquire the Company in an all-cash

transaction that values the Company at an enterprise value of approximately $8.1 billion. The transaction includes a

minority investment from a wholly owned subsidiary of the Abu Dhabi Investment Authority (“ADIA”).

The agreement provides that Univar Solutions shareholders will receive

$36.15 per share in cash, which represents a 20.6% premium to the Company’s

undisturbed closing stock price on November 22, 2022. The transaction

consideration also represents a premium of 33.6% to the volume-weighted average price of Univar Solutions for the

30 trading days ending on November 22, 2022.

“We are pleased to have reached this agreement with Apollo, which will provide immediate and certain cash value

for Univar Solutions shareholders,” said Chris Pappas, chairman of the Univar Solutions Board of Directors (the

“Board”). “The Board’s decision follows a comprehensive review of value creation opportunities for Univar

Solutions. We are conêdent this transaction is the right path forward and achieves our goal of maximizing value for

Univar Solutions shareholders.”

David Jukes, president and chief executive officer of Univar Solutions, said, “Over the last three years, we have

transformed the Company, putting the customer at the center of all we do, which has solidified our position as a

leading value-added service and solution provider. This transaction reflects the success of our strategy and delivers

substantial value to our shareholders. It is a testament to the tireless efforts of my colleagues, whose commitment

to our purpose of helping keep our communities healthy, fed, clean, and safe has enabled our success.

In Apollo, we are pleased to gain a partner to support continued investment in our portfolio and I look forward to working

closely with their team as we grow Univar Solutions and serve our key suppliers and customers globally.”

Apollo Private Equity Partner Sam Feinstein said, “Univar is a global leader in specialty chemicals and ingredients

distribution, fueling a vast array of industries with innovative, safe and sustainable solutions. In recent years, David

and his team have made tremendous progress enhancing the customer experience, and we believe Univar can

accelerate its long-term strategy as an Apollo Fund portfolio company. We look forward to leveraging our extensive

experience in the sector to support management in this exciting next phase.”

Transaction Details

The merger agreement, which has been unanimously approved by the Univar Solutions Board of Directors,

provides that Univar Solutions shareholders will receive $36.15 in cash for each share of common stock they own.

The transaction will be enhanced with equity provided by the Apollo Funds, a minority equity investment from a

wholly owned subsidiary of ADIA and a committed debt ênancing package.

The transaction is expected to close in the second half of 2023, subject to customary closing conditions, including

approval by Univar Solutions shareholders and receipt of regulatory approvals. The transaction is not subject to a

ênancing condition.

Upon completion of the transaction, shares of Univar Solutions common stock will no longer trade on the New York

Stock Exchange, and Univar Solutions will become a privately held company. Univar Solutions will continue to

operate under the Univar Solutions name and brand and maintain a global presence.

The foregoing description of the merger agreement and the transactions contemplated thereby is subject to, and is

qualified in its entirety by reference to, the full terms of the merger agreement, which Univar Solutions will file with

the U.S. Securities and Exchange Commission as an exhibit to a Current Report on Form 8-K.

March 3, 2023

Epoxy Highlights from Westlake Investors Call

Westlake Corporation (WLK) Q4 2022 Earnings Call Transcript

Feb. 21, 2023 2:46 PM ETWestlake Corporation (WLK)

Q4: 2023-02-21 Earnings Summary

EPS of $1.86 misses by $0.43 | Revenue of $3.30B (-5.93% Y/Y) misses by $111.98M

Westlake Corporation (NYSE:WLK) Q4 2022 Results Conference Call February 21, 2023 11:00 AM ET

Company Participants

Jeff Holy – Vice President & Treasurer

Albert Chao – President and Chief Executive Officer

Steven Bender – Executive Vice President and Chief Financial Officer

Roger Kearns – Chief Operating Officer and Executive Vice President, Performance and Essential Materials

Albert Chao

Thank you, Jeff. Good morning, everyone. We appreciate you joining us to discuss our fourth quarter and full year 2022 results. For the full year of 2022, we reported record net income of over $2.2 billion or $17.34 per share and record EBITDA of $4.2 billion on record sales of $15.8 billion.

While 2022 was a record year, it was also a challenging year as we experienced energy volatility, rapidly rising interest rates, evolving COVID policies impacting Asian demand and market dislocations due to the war in Ukraine. As these obstacles evolved and drove more difficult economic conditions in the second half of the year, Westlake took proactive actions to navigate a slower GDP growth with cost savings initiatives.

These broad-based 2022 initiatives included reductions in overhead and energy costs, synergies from acquisitions and investments in digital and automation that lowered our cost by approximately $50 million and also drove operational efficiencies. Thanks in part to these actions and despite the challenging external environment. For a second consecutive year, we achieved records for sales, EBITDA and net income, with EBITDA almost doubling from the previous cycle high in 2018.

I want to take a few minutes to review several of our major accomplishments in 2022. We generated record cash from operations of $3.4 billion. This significant level of cash flow allowed us to return $270 million to investors in the form of dividends and share repurchases, retire $250 million in debt, deploy $1 billion to improve the reliability of our plants and grow our production capacity to meet customers’ needs, close $1.4 billion in acquisitions and grow our ending cash balance by $300 million.

The evolution and integration of our business continued in 2022 as we closed the Epoxy acquisition and increase our ethylene integration with the additional investment into our LACC Ethylene joint venture. Integrating these businesses into Westlake, as we have with Boral, DASCO and Dimex acquisitions which closed in 2021, drove synergies in 2022.

This evolution of our business spurred the changing of our name from Westlake Chemical to Westlake Corporation, which better represents the significant breadth of the products we produce and industries we serve. Decarbonizing our assets and drive sustainability remain important initiatives and growth opportunities for Westlake. As part of our sustainability efforts, we established a carbon reduction goal to reduce our Scope 1 and Scope 2 emission intensity by 20% by 2030.

Albert Chao

Thank you, Steve. During the fourth quarter, we saw deteriorating economic conditions that led to inventory destocking, resulting in lower demand for our products in well-supplied markets. Since year-end, we have seen modest improvements early in the first quarter in demand for polyethylene and PVC with improving feedstock and energy costs providing some margin tailwinds.

The large market for epoxy in Asia and Europe reflect sluggish demand as China begins its economic recovery and Europe continues to address its own economic and energy challenges. Looking ahead, while uncertainties remain in the macroeconomic outlook, we believe there are some positive trends appearing.

Energy costs have improved, particularly in Europe, albeit still at elevated levels. Forecast for U.S. housing starts ranging from 1.1 million to 1.3 million units over the next two years, which will be a 20% decline from the 2021, 2022 levels.

Even with the strength in housing construction that occurred over the past two years, annual new housing construction largely remained below the 50-year average of 1.5 million units. Therefore, we continue to have a deficit from underbuilding that occurred since 2007.

Duffy Fischer

Good morning. First question is just around the Epoxy acquisition. You’re kind of a year into it now. It’s been at the tough year here. So, can you do an after-action review? I mean, does the industry need to have some structural change? Does your business need to have some structural change? Or is this just really kind of a bad supply-demand setup right now that will fix itself over the next couple of years?

Roger Kearns

Yes. Thanks, Duffy, it’s Roger. Maybe a couple of comments there. I think Epoxy business for our first year, we started extremely strong. The first part of the year was a very strong part of the business. But as we move through the year, it certainly got weaker.

And by the end of the year, I would say the fourth quarter was really quite weak. I think there’s a couple of things as we look forward. We have seen China announced already in ’23 nearly a doubling of the wind energy installations over ’22. So, we’ll have to watch and see how that plays out.

But that should be kind of a nice boost in the markets. As you know, there’s — I mean, there’s a limited number of Western players. We’ll continue to do what we do, which is make our plants run more efficiently, more cost effective.

We’ll copy our Westlake model into those sites. So, I think there’s some self-help work we’ll do, but hopefully as well with aviation, automotive and some wind energy picking up a little bit in ’23, we can get the ’23 looking better than certainly the end of ’22.

Duffy Fischer

Fair enough. And then the stat or the projection you threw in there on remodel and repair at 2.6% for the year, one, is you’re just talking to your customers as you’re looking at your order book, does that feel like kind of the right number? And then maybe like a follow-on to the last question, if that ends up being the right number, how does that look first half versus second half do you think?

Steven Bender

So, Duffy, it’s Steve. And I would say that the tone that we saw at the builder show recently was constructive, and I think it aligns with the tone that we saw from those that visited the builder show. And certainly, there is some expectation that will continue on as we go forward. Typically, when housing starts slow, repair and remodeling show strength.

And so, there is a typical investment cycle that homeowners always undertake. And that is they’re either improving their home either to sell to move forward or improving their home because affordability to move on to a new home is too expensive.

So, we do think that, that aligns with the tone we’re hearing from our customers and consistent with the contributions we think it will make to the business over the course of ’23.

Jeffrey Zekauskas

Okay. My follow-up, there was the vinyl chloride release in Ohio. Do you think that, that has implications for the chlorovinyl industry? Or do you think that, that will lead to some kind of change? Or do you have any general comment?

Albert Chao

Yes. I think people are waiting for the surface transportation safety board come back with the report. I’m sure there’ll be more government regulation on railroads and possibly on the shippers on safety.

These are very important products that ship around the country. So, the demand has to be satisfied. But definitely, we need to increase the safety by the variables primarily. I will think on the equipment, some of them getting old, and we heard new technologies out there to improve the safety aspect of the railroads.

Eric Petrie

Thank you, Albert. And then maybe a question for Roger on your comment of the doubling of installations in China. What does that do to kind of supply-demand balances in the country? And then how much capacity is China adding this year and kind of what needs to be absorbed from last year?

Roger Kearns

Yes. So, I think wind in China is — China is a big driver of the wind market. And so, they’ve got RFQs out there, say, about double this year what they’ve done last year. That’s a good first step, I think, in really starting to absorb the extra capacity that’s come in as well as avoid the exports, right?

So as Albert mentioned, with the China domestic market so slow, the China producers are exporting significant amounts. I think that will turn back inside and be used in China as opposed to hitting the export markets.

https://seekingalpha.com/article/4580333-westlake-corporation-wlk-q4-2022-earnings-call-transcript

February 28, 2023

New Epoxy Line From PPG

PPG launches an epoxy fire protection coating

MOSCOW (MRC) — PPG announces the launch of PPG STEELGUARD 951 coating, an innovative epoxy intumescent fire protection coating designed to meet the demands of modern architectural steel, including up to three hours of cellulosic fire protection, said the company.

In a fire situation, the coating expands from a thin, lightweight film into a thick, foam-like layer that insulates the steel and maintains its structural integrity, providing more time for people to escape and limiting damage to buildings and assets.

PPG STEELGUARD® 951 coating also provides effective corrosion protection for very corrosive atmospheric environments up to ISO 12944 C5 without the need for a topcoat, which also reduces project time and costs to achieve results. It can provide up to 3,500 microns dry film thickness in a single coat and cures rapidly, making it ready to handle the day after application.

“Structural steel plays a critical role in modern architecture by enabling buildings to meet specific fire protection and corrosion resistance according to their function,” said Richard Mann, PPG global product manager, passive fire protection, Protective and Marine Coatings.

“PPG Steelguard 951 coating is unique in combining an aesthetically pleasing finish with high corrosion protection and, most importantly, the ability to maintain the steel’s stability in the event of a fire,” added Mann.

We remind, PPG will invest USD11 million to double the production capacity of its powder coatings plant in San Juan del Rio, Mexico. The expansion project is expected to be completed by mid-2023 and will allow the plant to meet the expected future demand for powder coatings in Mexico.

PPG is a leading supplier of powder coatings to the automotive, transportation, appliance, furniture and other markets. The company expanded the business with its 2020 acquisition of Alpha Coating Technologies, which manufactures powder coatings for light industrial applications and heat-sensitive substrates, and its 2021 acquisition of Worwag, which makes liquid, powder and film coatings for industrial and automotive applications. PPG recently agreed to acquire the powder coatings business of Arsonsisi, including a manufacturing plant in Verbania, Italy.

https://www.mrchub.com/news/406444-ppg-launches-an-epoxy-fire-protection-coating

February 21, 2023

Huntsman Q4 Results

Huntsman Announces Fourth Quarter 2022 Earnings; Approximately $1.2 Billion in Buybacks and Dividends in 2022; Huntsman Board Approves 12% Dividend Increase

Download as PDFFebruary 21, 2023 6:00am EST

Related Documents

Fourth Quarter and Recent Highlights

- Fourth quarter 2022 net loss of $91 million compared to net income of $597 million in the prior year period; fourth quarter 2022 diluted loss per share of $0.48 compared to diluted earnings per share of $2.73 in the prior year period.

- Fourth quarter 2022 adjusted net income of $8 million compared to adjusted net income of $195 million in the prior year period; fourth quarter 2022 adjusted diluted earnings per share of $0.04 compared to adjusted diluted earnings per share of $0.89 in the prior year period.

- Fourth quarter 2022 adjusted EBITDA of $87 million compared to adjusted EBITDA of $327 million in the prior year period.

- Fourth quarter 2022 net cash provided by operating activities from continuing operations was $297 million. Free cash flow from continuing operations was $211 million for the fourth quarter 2022 compared to free cash flow from continuing operations of $648 million in the prior year period.

- Repurchased approximately 9.1 million shares for approximately $250 million in the fourth quarter 2022.

- On February 17, 2023, the Board approved a 12% increase to the quarterly dividend.

- Huntsman has secured all regulatory approvals required to complete the sale of its Textile Effects division to Archroma, a portfolio company of SK Capital Partners. The transaction is expected to close on February 28, 2023. Huntsman expects the net after tax cash proceeds to be approximately $540 million before customary post-closing adjustments.

| Three months ended | Twelve months ended | |||||||

| December 31, | December 31, | |||||||

| In millions, except per share amounts | 2022 | 2021 | 2022 | 2021 | ||||

| Revenues | $ 1,650 | $ 2,112 | $ 8,023 | $ 7,670 | ||||

| Net (loss) income attributable to Huntsman Corporation | $ (91) | $ 597 | $ 460 | $ 1,045 | ||||

| Adjusted net income (1) | $ 8 | $ 195 | $ 636 | $ 726 | ||||

| Diluted (loss) income per share | $ (0.48) | $ 2.73 | $ 2.27 | $ 4.72 | ||||

| Adjusted diluted income per share(1) | $ 0.04 | $ 0.89 | $ 3.13 | $ 3.28 | ||||

| Adjusted EBITDA(1) | $ 87 | $ 327 | $ 1,155 | $ 1,246 | ||||

| Net cash provided by operating activities from continuing operations | $ 297 | $ 733 | $ 892 | $ 915 | ||||

| Free cash flow from continuing operations(2) | $ 211 | $ 648 | $ 620 | $ 589 |

| See end of press release for footnote explanations and reconciliations of non-GAAP measures. |

THE WOODLANDS, Texas, Feb. 21, 2023 /PRNewswire/ — Huntsman Corporation (NYSE: HUN) today reported fourth quarter 2022 results with revenues of $1,650 million, net loss of $91 million, adjusted net income of $8 million and adjusted EBITDA of $87 million.

Peter R. Huntsman, Chairman, President, and CEO, commented:

“In 2022 we delivered almost $1.2 billion of adjusted EBITDA and Free Cash Flow of over $600 million. We increased our dividend and in total returned approximately $1.2 billion to shareholders. We made great progress in our cost reduction programs to offset historically high inflation and energy costs and strengthen our core businesses. We also announced the agreement to sell our Textile Effects business, which we expect to be completed at the end of this month.

“Turning to 2023, we are optimistic that destocking will end in the first part of 2023 and fundamentals in our businesses will begin to modestly improve as we move through the year, but visibility into the second half is still low. We are seeing some green shoots in areas like China, automotive, and aerospace, but construction demand globally is still under pressure. Regardless of how much demand improves through the year, we will remain focused on delivering our previously announced cost reduction programs, returning cash to shareholders, and looking for strategic investments to improve our core business while maintaining a strong balance sheet. We look forward to updating you of our progress as we move through 2023.”

Segment Analysis for 4Q22 Compared to 4Q21

Polyurethanes

The decrease in revenues in our Polyurethanes segment for the three months ended December 31, 2022 compared to the same period of 2021 was primarily due to lower sales volumes and the negative impact of weaker major international currencies against the U.S. dollar, partially offset by higher MDI local prices. Sales volumes decreased primarily due to lower demand, particularly in our European and American regions. The decrease in segment adjusted EBITDA was primarily due to lower sales volumes, lower MDI margins, the negative impact of weaker major international currencies against the U.S. dollar and lower equity earnings from our minority-owned joint venture in China, partially offset by lower fixed costs.

Advanced Materials

The decrease in revenues in our Advanced Materials segment for the three months ended December 31, 2022 compared to the same period of 2021 was primarily due to lower sales volumes, partially offset by higher average selling prices. Sales volumes decreased primarily due to deselection of lower margin business and lower customer demand in industrial markets, partially offset by higher demand in our Aerospace market. Average selling prices increased largely in response to higher raw material, energy, and logistics costs as well as improved sales mix. The decrease in segment adjusted EBITDA was primarily due to lower sales volumes, partially offset by higher sales prices and improved sales mix.