Urethane Blog

Chinese Spandex Update

January 12, 2023

Spandex market may embrace a good start after LNY holiday

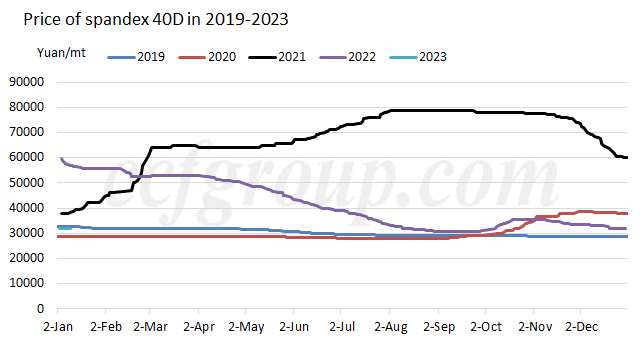

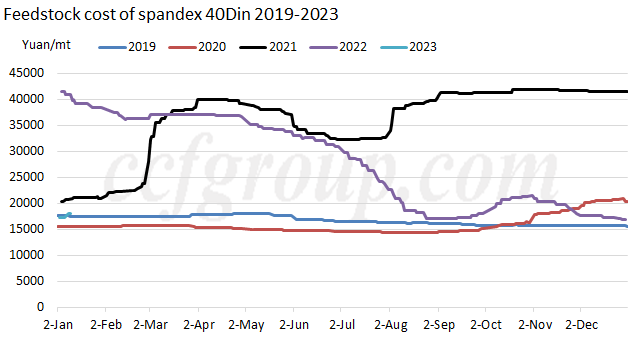

| The COVID-19 pandemic infection peak has been passed in fabric manufacturing bases in Zhejiang and Jiangsu. The worry of production resumption after the Lunar New Year’s (LNY) holiday has been mitigated. Buyers were active in purchasing spandex after the New Year’s Day. Price of PTMEG and MMDI stabilized and slightly rallied. Spandex market witnesses better supply, demand and cost. A good start after the Lunar New Year’s holiday may be deserved anticipation. In terms of price, the price of spandex 40D has been close to the historic bottom. Current price of spandex 40D has been higher than the low level in Sep 2,022. According to the data from CCFGroup, price of spandex 40D was at 32,000yuan/mt now, mainly discussed at 31,000-33,000yuan/mt. The discounts of some varieties have been canceled after inventory dropped substantially. Price of some medium-to-high end spandex 40D was at 33,000-36,000yuan/mt.  As for the feedstock cost, price of major feedstock PTMEG, BDO and MMDI all bottomed out. That meant the cost of spandex market climbed up. With rising price of BDO and in expectation of better demand, price of some PTMEG was required to rise by 2,000yuan/mt over Dec. Under the cost pressure, the discussion was in stagnation and the actual price increment was smaller at 500-1,000yuan/mt. Price of MMDI also rebounded. Wanhua Chemical updated liquid MMDI Jan nominations at 20,500yuan/mt, up by 500yuan/mt on the month.  From the angle of supply, the operating rate of spandex plants rose by 15 percentage points to 72% now from 57% before the New Year’s Day holiday, which was mainly driven by better sales in Jan, but it was still low compared with the same period in recent five years. From the angle of supply, the operating rate of spandex plants rose by 15 percentage points to 72% now from 57% before the New Year’s Day holiday, which was mainly driven by better sales in Jan, but it was still low compared with the same period in recent five years. More leading companies resumed operation from earlier production curtailment or suspension. Some big spandex plants will further ramp Looking at the inventory, the inventory of spandex was rapidly transferred to medium-to-downstream market. The inventory of spandex suppliers has reduced to 27 days, the second lowest during the corresponding period in recent five years. Some buyers were active in restocking even before the Lunar New Year’s Day holiday. Stocks fell rapidly in plants who cut or suspended much production before. Sellers reduced discounts. Some suppliers even controlled the volume of orders, worrying price of major feedstock to increase in Feb. Some fabric mills may continue replenishing after recouping some capital. The spandex inventory can guarantee the production for 15 days in some downstream plants, longer for near one month. The logistics will gradually suspend from this weekend affected by Spring Festival holiday. Spandex market witnesses better supply and demand at the beginning of 2023. The operating rate of spandex plants increases but some plants still control the run rate. The price of MMDI and PTMEG bottoms out. Many market players are optimistic about the sales and price of spandex after the Lunar New Year’s holiday. Supported by the factors such as supply, cost and demand, price of spandex may be hard to reduce but easy to increase before and after the Lunar New Year’s holiday. However, cautious mindset is held toward the spandex market at the end of Q1 2023. After the capacity expansion peak in 2022-2023, spandex market will see apparent oversupply. The increase of demand may be hard to chase up that of supply, which will restrict the rebounding range of spandex price. |

http://www.ccfgroup.com/newscenter/newsview.php?Class_ID=D00000&Info_ID=2023011230066