Epoxy

November 5, 2020

Olin Earnings

Olin Announces Third Quarter 2020 Results

Wed November 4, 2020 5:33 PM|PR Newswire|About: OLNQ3: 11-04-20 Earnings Summary

EPS of $-0.1307 beats by $0.10 Revenue of $1.44B (-8.82% Y/Y) beats by $22.97M

CLAYTON, Mo., Nov. 4, 2020 /PRNewswire/ — Olin Corporation (OLN) announced financial results for the third quarter ended September 30, 2020.

The third quarter 2020 reported net loss was $736.8 million, or $4.67 per diluted share, which compares to the third quarter 2019 reported net income of $44.2 million, or $0.27 per diluted share. Third quarter 2020 adjusted EBITDA of $195.5 million excludes depreciation and amortization expense of $142.1 million, a goodwill impairment charge of $699.8 million, information technology integration costs of $25.5 million, and restructuring charges and other non-recurring costs of $7.0 million. Third quarter 2019 adjusted EBITDA was $292.9 million. Sales in the third quarter 2020 were $1,437.6 million compared to $1,576.6 million in the third quarter 2019.

Scott Sutton, President and Chief Executive Officer, said, “Third quarter 2020 sales for the Chemicals businesses increased sequentially from second quarter 2020 by approximately 17%, and sales have increased every month since the low point in April. Additionally, Olin drove sequential pricing improvement in the third quarter 2020 for chlorine and almost all chlorine derivatives and our newly established ECU (Electrochemical Unit) Profit Contribution Index improved in the third quarter compared to the second quarter. Looking ahead, Olin’s recent price increases for chlorine, epoxy resins, bleach, ethylene dichloride and chlorinated organics are expected to positively contribute to our ECU Profit Contribution Index in the fourth quarter. Fourth quarter volumes are expected to be challenged based on customer year-end inventory reductions and Olin selectively selling less into poor quality markets, slightly more than offsetting the positives from driving price increases.

“The Winchester business continued to drive improved segment earnings from strong commercial ammunition demand. On October 1st, Winchester began to operate the Lake City U.S. Army Ammunition Plant (Lake City) and expects to generate sequential incremental adjusted EBITDA of approximately $10 million in fourth quarter 2020 from both Lake City and price increases across the commercial ammunition portfolio.”

Sutton added, “Our employees are engaged in implementing a new winning model focused on leveraging Olin’s leadership across the whole ECU and ammunition landscape regardless of singular product demand.”

SEGMENT REPORTING

Olin defines segment earnings as income (loss) before interest expense, interest income, goodwill impairment charges, other operating income (expense), non-operating pension income, other income, and income taxes.

CHLOR ALKALI PRODUCTS AND VINYLS

Chlor Alkali Products and Vinyls sales for the third quarter 2020 were $755.1 million compared to $876.3 million in the third quarter 2019. Third quarter 2020 segment earnings were $37.8 million compared to $112.7 million in the third quarter 2019. The decreases in the third quarter sales and segment earnings compared to the third quarter of 2019 were primarily due to lower ECU pricing, mainly caustic soda and ethylene dichloride, and lower volumes. The decline in segment earnings was partially offset by lower raw material and operating costs. Chlor Alkali Products and Vinyls third quarter 2020 results included depreciation and amortization expense of $112.1 million compared to $122.2 million in the third quarter 2019.

EPOXY

Epoxy sales for the third quarter 2020 were $476.1 million compared to $511.6 million in the third quarter 2019. The decrease in Epoxy sales was primarily due to lower product prices and lower epoxy resin volumes. The third quarter 2020 segment earnings were $14.9 million compared to $24.2 million in the third quarter 2019. The decrease in Epoxy segment earnings was primarily due to lower product prices and lower epoxy resin volumes, partially offset by lower raw material costs, primarily benzene and propylene, and lower operating costs. Epoxy third quarter 2020 results included depreciation and amortization expense of $23.9 million compared to $26.9 million in the third quarter 2019.

https://seekingalpha.com/pr/18072103-olin-announces-third-quarter-2020-results

November 5, 2020

Olin Earnings

Olin Announces Third Quarter 2020 Results

Wed November 4, 2020 5:33 PM|PR Newswire|About: OLNQ3: 11-04-20 Earnings Summary

EPS of $-0.1307 beats by $0.10 Revenue of $1.44B (-8.82% Y/Y) beats by $22.97M

CLAYTON, Mo., Nov. 4, 2020 /PRNewswire/ — Olin Corporation (OLN) announced financial results for the third quarter ended September 30, 2020.

The third quarter 2020 reported net loss was $736.8 million, or $4.67 per diluted share, which compares to the third quarter 2019 reported net income of $44.2 million, or $0.27 per diluted share. Third quarter 2020 adjusted EBITDA of $195.5 million excludes depreciation and amortization expense of $142.1 million, a goodwill impairment charge of $699.8 million, information technology integration costs of $25.5 million, and restructuring charges and other non-recurring costs of $7.0 million. Third quarter 2019 adjusted EBITDA was $292.9 million. Sales in the third quarter 2020 were $1,437.6 million compared to $1,576.6 million in the third quarter 2019.

Scott Sutton, President and Chief Executive Officer, said, “Third quarter 2020 sales for the Chemicals businesses increased sequentially from second quarter 2020 by approximately 17%, and sales have increased every month since the low point in April. Additionally, Olin drove sequential pricing improvement in the third quarter 2020 for chlorine and almost all chlorine derivatives and our newly established ECU (Electrochemical Unit) Profit Contribution Index improved in the third quarter compared to the second quarter. Looking ahead, Olin’s recent price increases for chlorine, epoxy resins, bleach, ethylene dichloride and chlorinated organics are expected to positively contribute to our ECU Profit Contribution Index in the fourth quarter. Fourth quarter volumes are expected to be challenged based on customer year-end inventory reductions and Olin selectively selling less into poor quality markets, slightly more than offsetting the positives from driving price increases.

“The Winchester business continued to drive improved segment earnings from strong commercial ammunition demand. On October 1st, Winchester began to operate the Lake City U.S. Army Ammunition Plant (Lake City) and expects to generate sequential incremental adjusted EBITDA of approximately $10 million in fourth quarter 2020 from both Lake City and price increases across the commercial ammunition portfolio.”

Sutton added, “Our employees are engaged in implementing a new winning model focused on leveraging Olin’s leadership across the whole ECU and ammunition landscape regardless of singular product demand.”

SEGMENT REPORTING

Olin defines segment earnings as income (loss) before interest expense, interest income, goodwill impairment charges, other operating income (expense), non-operating pension income, other income, and income taxes.

CHLOR ALKALI PRODUCTS AND VINYLS

Chlor Alkali Products and Vinyls sales for the third quarter 2020 were $755.1 million compared to $876.3 million in the third quarter 2019. Third quarter 2020 segment earnings were $37.8 million compared to $112.7 million in the third quarter 2019. The decreases in the third quarter sales and segment earnings compared to the third quarter of 2019 were primarily due to lower ECU pricing, mainly caustic soda and ethylene dichloride, and lower volumes. The decline in segment earnings was partially offset by lower raw material and operating costs. Chlor Alkali Products and Vinyls third quarter 2020 results included depreciation and amortization expense of $112.1 million compared to $122.2 million in the third quarter 2019.

EPOXY

Epoxy sales for the third quarter 2020 were $476.1 million compared to $511.6 million in the third quarter 2019. The decrease in Epoxy sales was primarily due to lower product prices and lower epoxy resin volumes. The third quarter 2020 segment earnings were $14.9 million compared to $24.2 million in the third quarter 2019. The decrease in Epoxy segment earnings was primarily due to lower product prices and lower epoxy resin volumes, partially offset by lower raw material costs, primarily benzene and propylene, and lower operating costs. Epoxy third quarter 2020 results included depreciation and amortization expense of $23.9 million compared to $26.9 million in the third quarter 2019.

https://seekingalpha.com/pr/18072103-olin-announces-third-quarter-2020-results

November 4, 2020

German Auto Update

German automotive improves but recovery may stall as second wave hits

Author: Morgan Condon

2020/11/04

LONDON (ICIS)–The German automotive sector performed better in October but the pace of recovery could stall before the end of the year, according to data from the Ifo Institute.

Newly imposed lockdowns in major European economies, including Germany, caused automotive industry’s expectations to decline for the fourth consecutive month as the restrictions could weigh heavily on economic activity.

However, current sentiment among automotive players increased to -0.2 points in October, up sharply from -20.4 points in September.

Both figures are up from the record low of -86.2 points posted in April.

Capacity utilisation rose to 86% in October, rising significantly from levels of 73% in July.

Companies are still planning to increase production, although at a more modest rate than in September.

Increased demand from the automotive sector has led to improved sentiment across various chemicals markets.

An upward tick in demand has provided some buoyancy for markets including polyethylene (PE), polymethyl methacrylate (PMMA), caprolactam (capro), methylene chloride (MEC), nylon, and toluene diisocyanate (TDI).

This has given some traction to chemicals producers; Germany’s Evonik said this week September demand for its materials, including from automotive, had been healthy.

“Replacement products like silica for tyres have led the way in the recovery but also nylon 6,6 has shown improving trends towards the end of the third quarter,” said Evonik’s CEO Christian Kullmann in a call with analysts.

The strength of automotive manufacturing was key in boosting sales in the specialty producer’s Smart Materials business unit.

Equity chemicals analysts at Baader Bank said Evonik’s Smart Materials division had “demonstrated stability” in inorganics such as hydrogen peroxide (H2)2) or catalysts.

“And [Evonik] benefited from improving trends in the automotive-related businesses.” said analyst Markus Mayer.

DRIVING FORCE

According to data from the European Automobile Manufacturers’ Association (ACEA), September was the first month to stem losses on the previous year, with an 8.4% increase compared to the same time a year prior.

Newly registered cars in Germany increased 5% in September, compared to the previous year, but this was not a boon to domestic industry as it was driven by demand for hybrid and electric vehicles (EVs).

While German manufacturers have some models available, there is a wider range from producers based in other countries.

Expectations declined for the fourth consecutive month in October, down sharply from 27.6 points in September to 17.7 points as new mobility restrictions kick in across Europe.

Order backlogs also shrank from September’s unusually high level of 51.5 points, down to 29.2 points in October.

Ifo’s research showed automobile manufacturers in Germany are looking to make further staff reductions.

CHANGING LANES

Although the domestic market may be suffering, Germany’s automotive industry is mainly reliant on exports.

Ifo said 74.8% of vehicles produced in 2019 were exported.

Dynamics for the export market are also expected to soften in coming months, falling from 31.3 points to 23.2 points in October.

Export demand already dropped 34% in January-September, year on year, with further losses prevented by more solid demand for German vehicles in China.

In 2019, China was the third largest export market for German producers, behind the UK and the US.

However, the course of the pandemic, hitting both the UK and the US hard, may erode the recovery.

“While the main European customer countries the UK, France, Italy or Spain, and also the US, are still firmly in the grip of the corona pandemic, the demand for German cars in China is picking up again noticeably,” said Ifo’s head for industrial organisation Oliver Falck.

Despite the challenges facing the automotive industry, German – and indeed European – chemicals makers could feel less impact as they are not confined to selling automotive materials and parts to domestic markets.

Buoyant demand in China and gradual recoveries in other regions could keep the automotive industry on stable ground to close off 2020.

However, as the pandemic can change course quickly, uncertainty is set to be the reigning trend for the time being.

Front page picture: Assembly line at a Volkswagen plant in Zwickau, east Germany

Source: Jens Meyer/AP/Shutterstock

Focus article by Morgan Condon

November 4, 2020

German Auto Update

German automotive improves but recovery may stall as second wave hits

Author: Morgan Condon

2020/11/04

LONDON (ICIS)–The German automotive sector performed better in October but the pace of recovery could stall before the end of the year, according to data from the Ifo Institute.

Newly imposed lockdowns in major European economies, including Germany, caused automotive industry’s expectations to decline for the fourth consecutive month as the restrictions could weigh heavily on economic activity.

However, current sentiment among automotive players increased to -0.2 points in October, up sharply from -20.4 points in September.

Both figures are up from the record low of -86.2 points posted in April.

Capacity utilisation rose to 86% in October, rising significantly from levels of 73% in July.

Companies are still planning to increase production, although at a more modest rate than in September.

Increased demand from the automotive sector has led to improved sentiment across various chemicals markets.

An upward tick in demand has provided some buoyancy for markets including polyethylene (PE), polymethyl methacrylate (PMMA), caprolactam (capro), methylene chloride (MEC), nylon, and toluene diisocyanate (TDI).

This has given some traction to chemicals producers; Germany’s Evonik said this week September demand for its materials, including from automotive, had been healthy.

“Replacement products like silica for tyres have led the way in the recovery but also nylon 6,6 has shown improving trends towards the end of the third quarter,” said Evonik’s CEO Christian Kullmann in a call with analysts.

The strength of automotive manufacturing was key in boosting sales in the specialty producer’s Smart Materials business unit.

Equity chemicals analysts at Baader Bank said Evonik’s Smart Materials division had “demonstrated stability” in inorganics such as hydrogen peroxide (H2)2) or catalysts.

“And [Evonik] benefited from improving trends in the automotive-related businesses.” said analyst Markus Mayer.

DRIVING FORCE

According to data from the European Automobile Manufacturers’ Association (ACEA), September was the first month to stem losses on the previous year, with an 8.4% increase compared to the same time a year prior.

Newly registered cars in Germany increased 5% in September, compared to the previous year, but this was not a boon to domestic industry as it was driven by demand for hybrid and electric vehicles (EVs).

While German manufacturers have some models available, there is a wider range from producers based in other countries.

Expectations declined for the fourth consecutive month in October, down sharply from 27.6 points in September to 17.7 points as new mobility restrictions kick in across Europe.

Order backlogs also shrank from September’s unusually high level of 51.5 points, down to 29.2 points in October.

Ifo’s research showed automobile manufacturers in Germany are looking to make further staff reductions.

CHANGING LANES

Although the domestic market may be suffering, Germany’s automotive industry is mainly reliant on exports.

Ifo said 74.8% of vehicles produced in 2019 were exported.

Dynamics for the export market are also expected to soften in coming months, falling from 31.3 points to 23.2 points in October.

Export demand already dropped 34% in January-September, year on year, with further losses prevented by more solid demand for German vehicles in China.

In 2019, China was the third largest export market for German producers, behind the UK and the US.

However, the course of the pandemic, hitting both the UK and the US hard, may erode the recovery.

“While the main European customer countries the UK, France, Italy or Spain, and also the US, are still firmly in the grip of the corona pandemic, the demand for German cars in China is picking up again noticeably,” said Ifo’s head for industrial organisation Oliver Falck.

Despite the challenges facing the automotive industry, German – and indeed European – chemicals makers could feel less impact as they are not confined to selling automotive materials and parts to domestic markets.

Buoyant demand in China and gradual recoveries in other regions could keep the automotive industry on stable ground to close off 2020.

However, as the pandemic can change course quickly, uncertainty is set to be the reigning trend for the time being.

Front page picture: Assembly line at a Volkswagen plant in Zwickau, east Germany

Source: Jens Meyer/AP/Shutterstock

Focus article by Morgan Condon

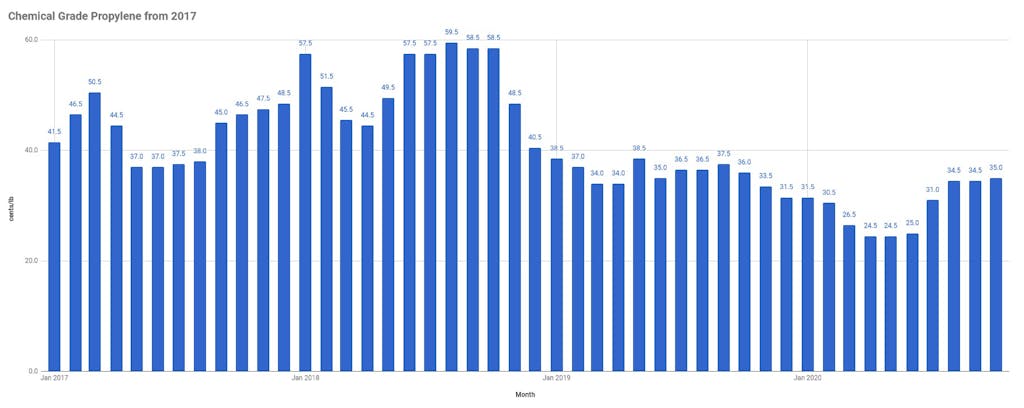

November 3, 2020

Propylene Update

October chemical grade propylene settled on the 28th up 0.5 cents/lb to $0.35/lb.