Epoxy

October 8, 2021

Energy Price Increases Hit Korea

Soaring LPG prices rapidly deteriorate Korean petrochem makers’ profitability

|

| [Photo by Kim Ho-young] |

| <이미지를 클릭하시면 크게 보실 수 있습니다> |

A sharp surge in liquefied petroleum gas (LPG) prices driven by a surge in oil prices is threatening the profitability of South Korean petrochemical companies that heavily relay on propane to produce plastic materials.

According to industry sources on Tuesday, LPG prices soared nearly 30 percent in seven months from over $500 per ton in March to over $800 in September. The higher crude oil prices have led to a jump in LPG prices given that LPG is produced in the process of refining crude oil. The recent hike, however, is seen as excessive, sources say.

The anticipated higher demand for heating during the upcoming winter season should hike LPG prices further, industry observers concerned.

With the surge in LPG prices, Korean petrochemical companies are rapidly losing profit because they rely on import propane to make and sell plastic products.

Removing hydrogen from LPG-categorized propane creates propylene, which is a feedstock to make plastics. Petrochemical companies usually produced naphtha from crude oil before changing it to propylene but because the abundant supply of U.S. Shale gas had helped significantly lower LPG prices, producing propylene using propane began to generate more profit.

In recent years, major Korean petrochemical players such as Lotte Chemical, LG Chem, and Hanwha Total, expanded facility that produces propylene using propane. With the surge in LPG prices, however, the companies started losing price competitiveness.

Industry sources noted that in general, producing propylene using LPG creates more profit when LPG price per ton falls to below 90 percent of naphtha.

Until last year, LPG prices were kept low, leading many petrochemical companies to rush to ramp up propylene production using LPG instead of naphtha. But tith LPG prices hitting multi-year highs near naphtha prices, local petrochemical players are under mounting pressure to change their feedstock diversification strategies.

October 8, 2021

MGC to Expand Production of MXDA

Mitsubishi Gas Chemical Announces Expansion of MXDA Production

September 29, 2021

Mitsubishi Gas Chemical Company, Inc. (MGC; Head Office: Chiyoda-ku, Tokyo; President: Masashi Fujii) is pleased to announce expansion of Meta-xylenediamine (MXDA) production in Europe.

MGC is expanding its production capacity of MXDA to meet the market growth in the epoxy, polyamide and isocyanate sector. MGC will be constructing a 25,000 MTA plant in Rotterdam through its newly established subsidiary, MGC Specialty Chemicals Netherlands B.V. The new plant is scheduled to start its operation in mid-2024.

MGC has just started off its 3-year management plan ‘Grow UP 2023’ this April and aims to shift to a profit structure more resilient to environmental changes. MXDA is internally defined as a “differentiating” business, to which the company will proactively allocate its resources to further strengthen its competitive advantage.

MXDA is mainly used in epoxy coatings for infrastructure applications due to its excellent anticorrosion properties, and a long-term growth in the market is expected. The new plant will be located in Rotterdam to mainly meet the demand in Europe, which is the largest market for MXDA in this sector. With the establishment of the new manufacturing subsidiary, the MGC Group will be able to strengthen its business continuity plan (BCP) and ensure the stable supply of MXDA worldwide.

The two existing plants in Japan will be in full operation until the start-up of the new plant, and will continue to serve the fast growing markets in Asia.

(1)Company Name MGC Specialty Chemicals Netherlands B.V.

(2)Location Rotterdam, Kingdom of the Netherlands

(3)Managing Director Mr. Masatoshi Sato

(4)Establishment *January 2021

(5)Business Content Manufacture and Sales of MXDA

(6)Start of Manufacturing July 2024 (scheduled)

(7)Capacity 25,000 MTA

(8)Ownership Ratio MGC 100%

(9)Capital 1.67 million Euro

Capital increase to 85.27 million Euro scheduled for November 2021

*) Established for the purpose of initial investigation. After the capital increase scheduled for November 2021, it will become a manufacturing subsidiary.

October 8, 2021

MGC to Expand Production of MXDA

Mitsubishi Gas Chemical Announces Expansion of MXDA Production

September 29, 2021

Mitsubishi Gas Chemical Company, Inc. (MGC; Head Office: Chiyoda-ku, Tokyo; President: Masashi Fujii) is pleased to announce expansion of Meta-xylenediamine (MXDA) production in Europe.

MGC is expanding its production capacity of MXDA to meet the market growth in the epoxy, polyamide and isocyanate sector. MGC will be constructing a 25,000 MTA plant in Rotterdam through its newly established subsidiary, MGC Specialty Chemicals Netherlands B.V. The new plant is scheduled to start its operation in mid-2024.

MGC has just started off its 3-year management plan ‘Grow UP 2023’ this April and aims to shift to a profit structure more resilient to environmental changes. MXDA is internally defined as a “differentiating” business, to which the company will proactively allocate its resources to further strengthen its competitive advantage.

MXDA is mainly used in epoxy coatings for infrastructure applications due to its excellent anticorrosion properties, and a long-term growth in the market is expected. The new plant will be located in Rotterdam to mainly meet the demand in Europe, which is the largest market for MXDA in this sector. With the establishment of the new manufacturing subsidiary, the MGC Group will be able to strengthen its business continuity plan (BCP) and ensure the stable supply of MXDA worldwide.

The two existing plants in Japan will be in full operation until the start-up of the new plant, and will continue to serve the fast growing markets in Asia.

(1)Company Name MGC Specialty Chemicals Netherlands B.V.

(2)Location Rotterdam, Kingdom of the Netherlands

(3)Managing Director Mr. Masatoshi Sato

(4)Establishment *January 2021

(5)Business Content Manufacture and Sales of MXDA

(6)Start of Manufacturing July 2024 (scheduled)

(7)Capacity 25,000 MTA

(8)Ownership Ratio MGC 100%

(9)Capital 1.67 million Euro

Capital increase to 85.27 million Euro scheduled for November 2021

*) Established for the purpose of initial investigation. After the capital increase scheduled for November 2021, it will become a manufacturing subsidiary.

October 8, 2021

Update on China Power Situation

Coal For Christmas

by Tyler DurdenThursday, Oct 07, 2021 – 02:40 PM

Authored by Fortis Analysis via Human Terrain (emphasis ours),

In mid-April 2021, I began receiving reports from sources in China and the United States that certain regions in China had begun to experience ongoing power disruptions at their warehouses and manufacturing facilities. Most notable of these was in south China’s Guangdong megaregion, where in June operations at the Taishan Nuclear Power Plant had become disrupted by a small number of faulty claddings for the fuel rods, ultimately forcing state-owned General Nuclear Power Group to shut down Unit 1 (there are two units) for maintenance and repair. Concurrently, available power imported to the Guangdong region from Yunnan province’s considerable hydroelectric capacity was reduced due to drier-than-expected weather throughout the spring.

Taken together, some estimates are that total power available to the region fell by as much as 15% by June. In response, officials began quietly rationing power to factories, cutting business operation days by 1 or 2 days depending on the facilities’ power requirements.

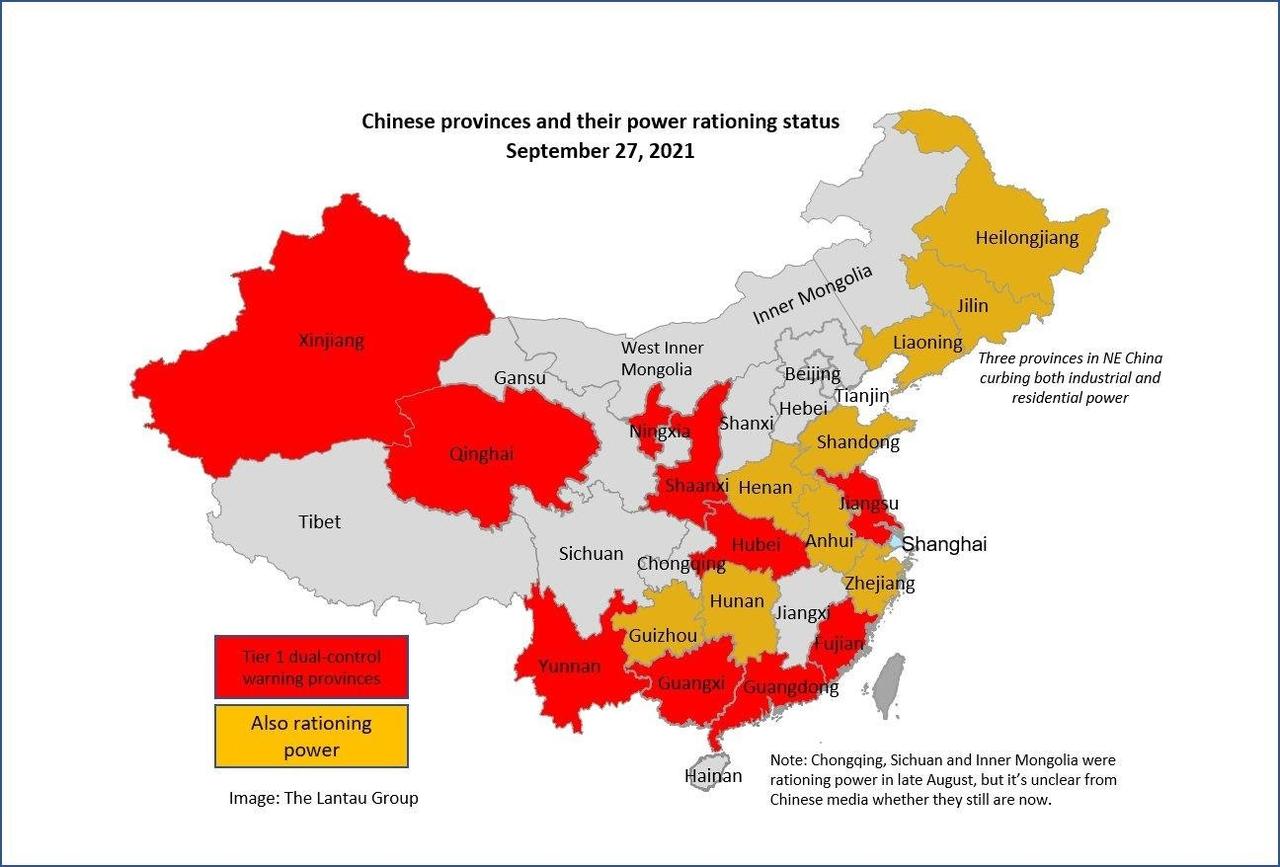

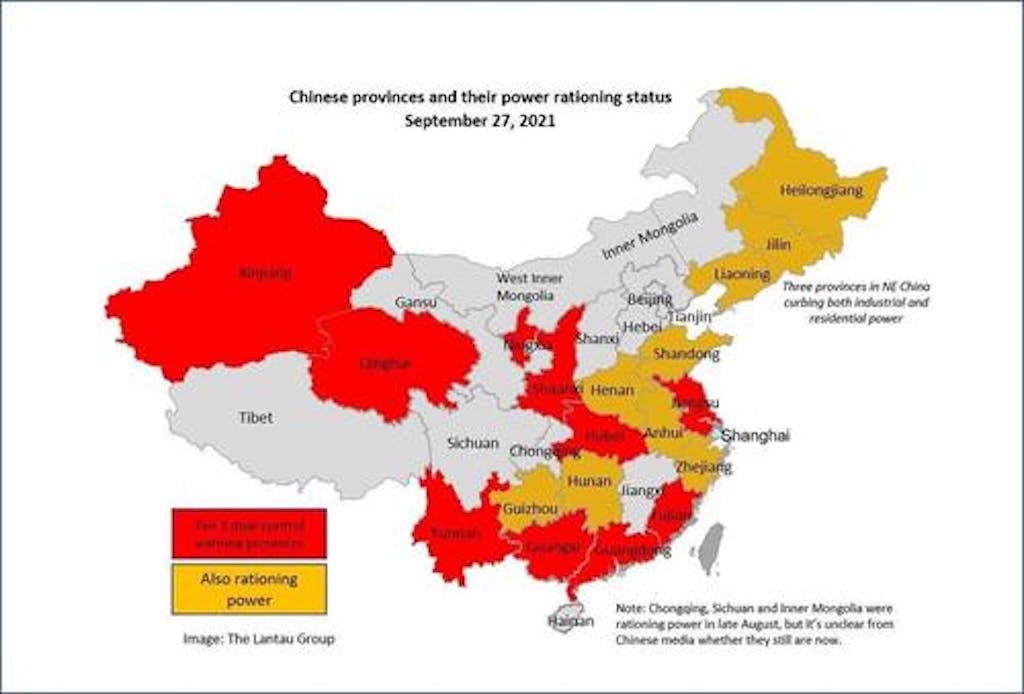

In recent weeks, however, officials have begun a much more aggressive rationing program (Figure 1), with factories in much of Guangdong now seeing only 1-2 days per week of power use allowed. Similar situations are reportedly occurring in Jiangsu, Hubei, and Fujian provinces, all major manufacturing regions. As just one example, one of my US-based import customers has reported that a key supplier in Jiangsu is down to a single day per week of power availability. Limited-but-expanded power rationing is also occurring in Zhejiang, Shandong, Liaoning, and other important heavy industrial, chemical, and energy-product hubs.Figure 1 – Chinese Province Power Rationing Regime – Courtesy of The Lantau Group

{kind=link}

The primary causes of power disruptions are the aforementioned reduced availability of hydroelectric power in much of southern China, as well as limited supplies of coal due to the ongoing China/Australia trade dispute. The latter cause is expected to be more sustained in impact, as the year-long embargo by China on Australian thermal coal has depleted China’s strategic reserves and caused commercial and residential prices to rapidly spike. China imports about 10% of its annual thermal coal needs; of this, Australia was close to 70% of the total prior to the mid-2020 embargo. It is expected that China will be forced to drop the embargo ahead of the fourth quarter, but this is not certain. Reopening its markets to Australian coal imports would be an important stabilizing step for China’s manufacturing base, but would nonetheless take weeks or even months to ramp back up to normal output.

If China does not capitulate on the importation of Australian coal and cannot close the gap with imports from Brazil, South Africa, and the US, the southern region will continue to see constrained power availability, reducing export volumes especially from Shenzhen’s ports, Hong Kong, and Xiamen, as well as Tianjin, Dalian, and Qingdao in the north. We would expect in this scenario to see these ports be utilized by ocean carriers for more transshipments out of Southeast Asia or central China, while export-focused capacity shifts to Ningbo and Shanghai, as well as alleviating significant congestion pressure at Kaohsiung and Busan. Freight rates are anticipated by some maritime industry players to soften somewhat, though a bullish case for barely-reduced rates could be made that a very large backlog of existing cargo and ongoing delays at US and European ports will keep volumes at a high level through Lunar New Year at least, with a strong likelihood of continuing through the ILWU negotiations.

October 8, 2021

Update on China Power Situation

Coal For Christmas

by Tyler DurdenThursday, Oct 07, 2021 – 02:40 PM

Authored by Fortis Analysis via Human Terrain (emphasis ours),

In mid-April 2021, I began receiving reports from sources in China and the United States that certain regions in China had begun to experience ongoing power disruptions at their warehouses and manufacturing facilities. Most notable of these was in south China’s Guangdong megaregion, where in June operations at the Taishan Nuclear Power Plant had become disrupted by a small number of faulty claddings for the fuel rods, ultimately forcing state-owned General Nuclear Power Group to shut down Unit 1 (there are two units) for maintenance and repair. Concurrently, available power imported to the Guangdong region from Yunnan province’s considerable hydroelectric capacity was reduced due to drier-than-expected weather throughout the spring.

Taken together, some estimates are that total power available to the region fell by as much as 15% by June. In response, officials began quietly rationing power to factories, cutting business operation days by 1 or 2 days depending on the facilities’ power requirements.

In recent weeks, however, officials have begun a much more aggressive rationing program (Figure 1), with factories in much of Guangdong now seeing only 1-2 days per week of power use allowed. Similar situations are reportedly occurring in Jiangsu, Hubei, and Fujian provinces, all major manufacturing regions. As just one example, one of my US-based import customers has reported that a key supplier in Jiangsu is down to a single day per week of power availability. Limited-but-expanded power rationing is also occurring in Zhejiang, Shandong, Liaoning, and other important heavy industrial, chemical, and energy-product hubs.Figure 1 – Chinese Province Power Rationing Regime – Courtesy of The Lantau Group

The primary causes of power disruptions are the aforementioned reduced availability of hydroelectric power in much of southern China, as well as limited supplies of coal due to the ongoing China/Australia trade dispute. The latter cause is expected to be more sustained in impact, as the year-long embargo by China on Australian thermal coal has depleted China’s strategic reserves and caused commercial and residential prices to rapidly spike. China imports about 10% of its annual thermal coal needs; of this, Australia was close to 70% of the total prior to the mid-2020 embargo. It is expected that China will be forced to drop the embargo ahead of the fourth quarter, but this is not certain. Reopening its markets to Australian coal imports would be an important stabilizing step for China’s manufacturing base, but would nonetheless take weeks or even months to ramp back up to normal output.

If China does not capitulate on the importation of Australian coal and cannot close the gap with imports from Brazil, South Africa, and the US, the southern region will continue to see constrained power availability, reducing export volumes especially from Shenzhen’s ports, Hong Kong, and Xiamen, as well as Tianjin, Dalian, and Qingdao in the north. We would expect in this scenario to see these ports be utilized by ocean carriers for more transshipments out of Southeast Asia or central China, while export-focused capacity shifts to Ningbo and Shanghai, as well as alleviating significant congestion pressure at Kaohsiung and Busan. Freight rates are anticipated by some maritime industry players to soften somewhat, though a bullish case for barely-reduced rates could be made that a very large backlog of existing cargo and ongoing delays at US and European ports will keep volumes at a high level through Lunar New Year at least, with a strong likelihood of continuing through the ILWU negotiations.