The Urethane Blog

Everchem Updates

VOLUME XXI

September 14, 2023

Everchem’s exclusive Closers Only Club is reserved for only the highest caliber brass-baller salesmen in the chemical industry. Watch the hype video and be introduced to the top of the league: — read more

August 28, 2020

Remember when ICI convinced Huntsman to buy the TiO2 business and the Wilton cracker in order to obtain the urethanes business back in 1999? So this divestiture finalizes the total change of Huntsman from a commodity polystyrene business to today’s entity that is now about 60% urethanes . . . A throwback article from the original sale is attached at the bottom.

Huntsman Agrees to Sell its Remaining Interest in Venator Materials PLC

Download as PDF August 28, 2020 5:16pm EDT

THE WOODLANDS, Texas, Aug. 28, 2020 /PRNewswire/ — Huntsman Corporation (NYSE: HUN) announced today that it has entered into a definitive agreement with funds advised by SK Capital Partners, LP to sell approximately 42.5 million of the shares it holds in Venator Materials PLC for a cash purchase price of approximately $100 million, including a 30-month option for the sale of the remaining approximate 9.5 million shares it holds at $2.15 per share. The transaction is subject to regulatory approvals and is expected to close near year-end.

Together with estimated cash tax savings of approximately $150 million anticipated by offsetting the capital loss on the sale of Venator shares against the capital gain realized on the sale of our chemical intermediates and surfactants businesses that closed this year in January, we expect to secure an aggregate total benefit of approximately $250 million in cash near year end.

Peter Huntsman, Chairman, President and CEO, further commented, “I am pleased to have reached an agreement to sell our remaining interest in Venator to SK Capital. We enjoy an ongoing relationship with SK Capital and their co-founder Barry Siadat. They are a great owner and operator of businesses and we are pleased for them to acquire Huntsman’s stake in Venator, a world class functional and specialty TiO2 business. The proceeds to be received will further bolster our balance sheet and only enhance our flexibility for further growth.“

News | May 4, 1999

ICI Divests Urethanes, Titanium Dioxide, Petrochemicals to Huntsman; Refinishing, Industrial Coatings to PPG

Imperial Chemical Industries (ICI, London, UK) continues to divest commodity chemicals in order to concentrate on specialty products. Its latest actions include the £1.7 billion sale of polyurethanes, titanium dioxide and selected petrochemicals businesses to Huntsman Chemical Corp. (Salt Lake City, UT). It will also sell most of its global automotive refinishing and industrial coatings units to PPG Industries Inc. (Pittsburgh, PA) for £425 million.

The first transaction includes polyurethanes, titanium dioxide, and paraxylene. It nearly doubles the size of Huntsman, North America’s largest privately owned chemical company, to more than $7.5 billion. The urethanes and titanium dioxide businesses both have solid technology positions and major global markets.

A German automotive refinisher repairs a car using a PPG waterborne system designed to reduce emissions to comply with increasingly stringent environmental regulations. The purchase of ICI’s global automotive refinish and industrial coatings operations augments PPG’s already-strong franchise in this field.

The deal suddenly makes Huntsman a major presence in 11 countries. It also increases Huntsman capacity by 8.7 billion lb/y, to more than 28 billion lb/y, and adds 7000 to its payroll, bringing it to 16,000. The companies expect to close the deal this summer. Huntsman also says it is interested in purchasing ICI’s acrylics business, which is also up for sale.

The purchase involves three segments:

- Polyurethane: ICI operates facilities in Wilton, UK; Rozenburg, the Netherlands; and Geismar, LA; with an aggregate net asset value of £523 million. Total capacity is just over 1 billion lb/y, mostly in MDI-based materials though ICI also manufactures some TDI-based materials as well as polyols. It has 50 sales/representative offices worldwide. In 1998, the business achieved a trading profit (after corporate charges) of £90 million on sales of £816 million.

- Titanium dioxide: ICI’s Tioxide titanium dioxide business has manufacturing sites in Canada, France, Italy, Spain, United Kingdom, and Malaysia, and joint ventures in South Africa and the United States. Its total nameplate capacity approaches 1.3 billion lb/yr with an asset value of £661 million. Trading profits were £58 million on sales of £574 million.

- Petrochemicals: Huntsman will purchase ICI’s aromatics business (primarily benzene and paraxylene, which is used in polyester and polyurethane production) and ICI’s share of olefins production (chiefly ethylene and propylene for polymers) from the cracker at Wilton, Teeside. The assets are valued at £96 million. The business lost £27 million on sales of £659 million in 1998.

Huntsman will acquire the businesses by forming a new company, Huntsman ICI Holdings (HICI) in partnership with ICI. HICI will include Huntsman’s US propylene oxide business, which earned $79 million on $339 million sales in 1998. ICI will retain a £300 million investment in the new business for a minimum of three years. It will use the remaining £1.4 billion from the transaction to reduce debt incurred with its £8 billion purchase of Unilever’s specialty chemical business in 1997.

https://www.chemicalonline.com/doc/ici-divests-urethanes-titanium-dioxide-petroc-0001

August 28, 2020

Remember when ICI convinced Huntsman to buy the TiO2 business and the Wilton cracker in order to obtain the urethanes business back in 1999? So this divestiture finalizes the total change of Huntsman from a commodity polystyrene business to today’s entity that is now about 60% urethanes . . . A throwback article from the original sale is attached at the bottom.

Huntsman Agrees to Sell its Remaining Interest in Venator Materials PLC

Download as PDF August 28, 2020 5:16pm EDT

THE WOODLANDS, Texas, Aug. 28, 2020 /PRNewswire/ — Huntsman Corporation (NYSE: HUN) announced today that it has entered into a definitive agreement with funds advised by SK Capital Partners, LP to sell approximately 42.5 million of the shares it holds in Venator Materials PLC for a cash purchase price of approximately $100 million, including a 30-month option for the sale of the remaining approximate 9.5 million shares it holds at $2.15 per share. The transaction is subject to regulatory approvals and is expected to close near year-end.

Together with estimated cash tax savings of approximately $150 million anticipated by offsetting the capital loss on the sale of Venator shares against the capital gain realized on the sale of our chemical intermediates and surfactants businesses that closed this year in January, we expect to secure an aggregate total benefit of approximately $250 million in cash near year end.

Peter Huntsman, Chairman, President and CEO, further commented, “I am pleased to have reached an agreement to sell our remaining interest in Venator to SK Capital. We enjoy an ongoing relationship with SK Capital and their co-founder Barry Siadat. They are a great owner and operator of businesses and we are pleased for them to acquire Huntsman’s stake in Venator, a world class functional and specialty TiO2 business. The proceeds to be received will further bolster our balance sheet and only enhance our flexibility for further growth.“

News | May 4, 1999

ICI Divests Urethanes, Titanium Dioxide, Petrochemicals to Huntsman; Refinishing, Industrial Coatings to PPG

Imperial Chemical Industries (ICI, London, UK) continues to divest commodity chemicals in order to concentrate on specialty products. Its latest actions include the £1.7 billion sale of polyurethanes, titanium dioxide and selected petrochemicals businesses to Huntsman Chemical Corp. (Salt Lake City, UT). It will also sell most of its global automotive refinishing and industrial coatings units to PPG Industries Inc. (Pittsburgh, PA) for £425 million.

The first transaction includes polyurethanes, titanium dioxide, and paraxylene. It nearly doubles the size of Huntsman, North America’s largest privately owned chemical company, to more than $7.5 billion. The urethanes and titanium dioxide businesses both have solid technology positions and major global markets.

A German automotive refinisher repairs a car using a PPG waterborne system designed to reduce emissions to comply with increasingly stringent environmental regulations. The purchase of ICI’s global automotive refinish and industrial coatings operations augments PPG’s already-strong franchise in this field.

The deal suddenly makes Huntsman a major presence in 11 countries. It also increases Huntsman capacity by 8.7 billion lb/y, to more than 28 billion lb/y, and adds 7000 to its payroll, bringing it to 16,000. The companies expect to close the deal this summer. Huntsman also says it is interested in purchasing ICI’s acrylics business, which is also up for sale.

The purchase involves three segments:

- Polyurethane: ICI operates facilities in Wilton, UK; Rozenburg, the Netherlands; and Geismar, LA; with an aggregate net asset value of £523 million. Total capacity is just over 1 billion lb/y, mostly in MDI-based materials though ICI also manufactures some TDI-based materials as well as polyols. It has 50 sales/representative offices worldwide. In 1998, the business achieved a trading profit (after corporate charges) of £90 million on sales of £816 million.

- Titanium dioxide: ICI’s Tioxide titanium dioxide business has manufacturing sites in Canada, France, Italy, Spain, United Kingdom, and Malaysia, and joint ventures in South Africa and the United States. Its total nameplate capacity approaches 1.3 billion lb/yr with an asset value of £661 million. Trading profits were £58 million on sales of £574 million.

- Petrochemicals: Huntsman will purchase ICI’s aromatics business (primarily benzene and paraxylene, which is used in polyester and polyurethane production) and ICI’s share of olefins production (chiefly ethylene and propylene for polymers) from the cracker at Wilton, Teeside. The assets are valued at £96 million. The business lost £27 million on sales of £659 million in 1998.

Huntsman will acquire the businesses by forming a new company, Huntsman ICI Holdings (HICI) in partnership with ICI. HICI will include Huntsman’s US propylene oxide business, which earned $79 million on $339 million sales in 1998. ICI will retain a £300 million investment in the new business for a minimum of three years. It will use the remaining £1.4 billion from the transaction to reduce debt incurred with its £8 billion purchase of Unilever’s specialty chemical business in 1997.

https://www.chemicalonline.com/doc/ici-divests-urethanes-titanium-dioxide-petroc-0001

August 28, 2020

![]()

Press Release of Recticel – 28 August 2020 First half-year 2020 results – Mitigated COVID-19 impact and key strategic moves

Net sales: from EUR 453.8 million to EUR 374.3 million (-17.5%), including a -0.5% currency effect Adjusted EBITDA: from EUR 34.6 million to EUR 19.0 million (-44.9%) Result of the period (share of the Group): from EUR 16.1 million to EUR 60.1 million, including net capital gain and result for the period from discontinued operations Net financial debt: EUR 43.8 million (including EUR 55.2 million IFRS 16 lease obligations) Closing of the divestments of the participation in Eurofoam and of the Automotive Interiors division

Olivier Chapelle (CEO): “After a good start of the year, the COVID-19 pandemic has severely impacted the topline of the Group from mid-March onwards, resulting in a sales decline of -3.0% in 1Q2020 and -32.3% in 2Q2020. After reaching a low point of -51.5% in April 2020 versus April 2019, the sales shortfall versus last year has improved to -35.4% in May and -9.3% in June. This recovery trend continues with July 2020 being -4.1% lower than July 2019.

After having ensured that all sanitary measures had been put in place in all our locations to protect our employees, the Group immediately implemented measures to reduce costs and preserve cash. These measures include the adjustment of the production capacity, the use of temporary unemployment, strict spending and capital expenditure control. As a consequence, the cash consumption of our continued operations and the negative impact on Adjusted EBITDA have been reduced to the maximum extent possible.

On June 30th, the transactions related to the divestment of our participation in the Eurofoam joint venture and to the partial divestment of our Automotive Interiors division have been closed as planned and announced. As a consequence, the Group ended the second quarter with a net positive cash position of EUR 11.4 million (excluding the IFRS 16 lease obligations), and ample financial headroom to focus and engage in the execution of its growth strategy in its higher value added business segments.”

OUTLOOK Subject to there being no further COVID-19 impacts, the dynamics of the recovery observed during the 2nd quarter and the month of July lead the Group to expect the 2H2020 consolidated net sales and Adjusted EBITDA of its retained business to be at the level of 2H2019.

August 28, 2020

![]()

Press Release of Recticel – 28 August 2020 First half-year 2020 results – Mitigated COVID-19 impact and key strategic moves

Net sales: from EUR 453.8 million to EUR 374.3 million (-17.5%), including a -0.5% currency effect Adjusted EBITDA: from EUR 34.6 million to EUR 19.0 million (-44.9%) Result of the period (share of the Group): from EUR 16.1 million to EUR 60.1 million, including net capital gain and result for the period from discontinued operations Net financial debt: EUR 43.8 million (including EUR 55.2 million IFRS 16 lease obligations) Closing of the divestments of the participation in Eurofoam and of the Automotive Interiors division

Olivier Chapelle (CEO): “After a good start of the year, the COVID-19 pandemic has severely impacted the topline of the Group from mid-March onwards, resulting in a sales decline of -3.0% in 1Q2020 and -32.3% in 2Q2020. After reaching a low point of -51.5% in April 2020 versus April 2019, the sales shortfall versus last year has improved to -35.4% in May and -9.3% in June. This recovery trend continues with July 2020 being -4.1% lower than July 2019.

After having ensured that all sanitary measures had been put in place in all our locations to protect our employees, the Group immediately implemented measures to reduce costs and preserve cash. These measures include the adjustment of the production capacity, the use of temporary unemployment, strict spending and capital expenditure control. As a consequence, the cash consumption of our continued operations and the negative impact on Adjusted EBITDA have been reduced to the maximum extent possible.

On June 30th, the transactions related to the divestment of our participation in the Eurofoam joint venture and to the partial divestment of our Automotive Interiors division have been closed as planned and announced. As a consequence, the Group ended the second quarter with a net positive cash position of EUR 11.4 million (excluding the IFRS 16 lease obligations), and ample financial headroom to focus and engage in the execution of its growth strategy in its higher value added business segments.”

OUTLOOK Subject to there being no further COVID-19 impacts, the dynamics of the recovery observed during the 2nd quarter and the month of July lead the Group to expect the 2H2020 consolidated net sales and Adjusted EBITDA of its retained business to be at the level of 2H2019.

August 27, 2020

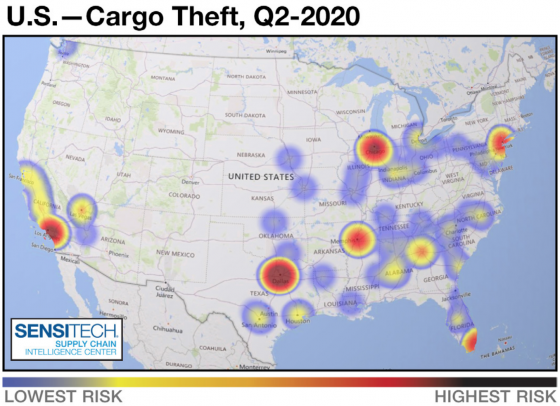

US Cargo Thefts Erupt As Violent Crime Spreads Across America

by Tyler Durden Wed, 08/26/2020 – 19:25

The latest trucking news from Overdrive is particularly disturbing, outlines how cargo theft across the US surged during the virus-induced downturn in the second quarter.

Overdrive, citing data from SensiGuard, a cargo theft recording firm aggregating data from transportation security councils, insurance companies and law enforcement organizations, said cargo theft surged 56% year-over-year in the quarter.

“One significant note is that April, which was at the height of the supply chain disruption caused by COVID-19, experienced more than double the volume of April 2019 (+109%). While both May (+31%) and June (+30%) also beat their 2019 totals, it was by a decreasing amount in each case,” SensiGuard noted in its 2Q20 cargo theft report.

The cargo theft monitoring firm recorded 227 thefts over the three months ending June, with 96 in April, 67 in May, and 64 in June. In dollar amount, the average theft was about a quarter-million dollars. It said 23% of all cargo thefts were miscellaneous products for retailers. Food and drinks made up about 20% of all thefts.

California, for the first time since 3Q17, was dethroned as the state with most cargo thefts. Texas became the epicenter of thefts in 2Q20, followed by California, Illinois, Florida, and Tennessee.

{kind=link}

In a separate report, we noted truckers on a popular trucking app called “CDLLife” polled its user base. They found an overwhelming number of drivers wouldn’t “pickup/deliver to cities with defunded/disbanded police departments.”

A rapid increase in cargo thefts, robberies, and violent crime across US metros is not surprising whatsoever as a virus-induced recession has unleashed depressionary unemployment levels for the bottom 90% of Americans. Tens of millions of folks are still unemployed, and now, have not received Trump stimulus checks in three weeks as they go broke and hungry, also at risk of eviction.

https://www.zerohedge.com/markets/us-cargo-thefts-erupt-violent-crime-spreads-across-america