HOUSTON (ICIS)–US August propylene contracts have settled at a 2 cent/lb increase for the majority of the market, although one seller did not settle at that level, market sources said on Tuesday and Wednesday.

The August settlement puts contract prices for polymer-grade propylene (PGP) at 61.0 cents/lb ($1,345/tonne) and for chemical-grade propylene at 59.5 cents/lb. The August settlement follows a rollover for July.

Propylene contracts faced upward pressure in early August following outages at US Gulf propane dehydrogenation (PDH) units in June and July and limited production from crackers due to lighter feedstocks.

However, some of that upward pressure eased while contract talks were underway as the lack of major outages in August allowed supplies to recover. Earlier in the month, propylene contract talks included increases of 3 cents/lb, and one contract nomination was as high as a 5 cent/lb increase.

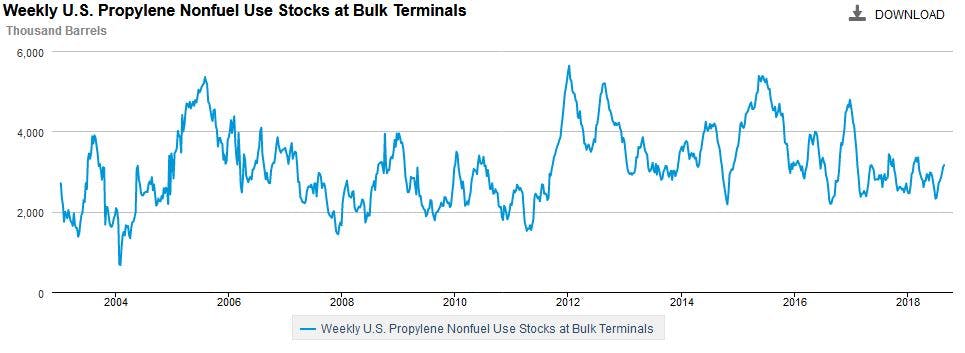

Propylene inventories have increased since early July. But after a near two-year low at the end of June, inventory levels remained relatively low heading into August. By mid-August, propylene inventory levels had risen to their highest point since March.

As inventories increased, spot prices softened. Spot polymer-grade propylene (PGP) fell into the high 50s cents/lb by mid-August after starting the month in the low 60s cents/lb.

Despite the supply recovery during August, propylene production from crackers remains constrained. An oversupply of ethylene has narrowed margins and encouraged increased usage of lighter ethane feedstocks, which produce the least amount of propylene.

Ethane’s share of the cracker feedslate has risen to 74.2% by June, up from 65.0% the previous June. The daily rate of propylene production from crackers in June was lower by 14.1% than the previous June, according to data from the Jacobs Consultancy.

“Propylene production has been in the longest period of ethane favoured cracking in years,” one market source said.

The combination of limited production from crackers and recent PDH outages has kept US propylene contract prices elevated compared with other regions since June. This puts domestically-produced derivatives at a cost-disadvantage to derivatives produced in other regions.

US, Europe, Asia propylene

While higher US prices have so far caused little demand destruction, derivative imports may increase as the US remains the high-priced region.

“Some derivatives may have been OK with higher prices in July, thinking it would only hurt for a month, but that bit them. So they may be more likely to look for imports due to further increases,” the market source said.

In response to an early 2018 propylene price spike, downstream polypropylene production rates had fallen significantly.

US propylene contracts are typically settled in the middle of the month for the current month.

Major US propylene producers include Chevron Phillips Chemical, ExxonMobil, Flint Hills Resources and Shell Chemical.

Major buyers include Arkema, Ascend Performance Materials, Braskem, Dow Chemical, INEOS, Oxea and Total.

Focus article by Jessie Waldheim