Epoxy

September 21, 2022

Container Rates Update

Fall In Container Spot Rates “Much Steeper”, “Less Orderly” Than Expected

Shipping liner executives predicted a continued drop in spot rates during their latest quarterly calls, while offering soothing assurances to investors that the fall would be gradual. Maersk CFO Patrick Jany said it would be a “progressive erosion,” not “a one-day drop.” Matson CEO Matt Cox emphasized rates were “adjusting slowly” in an “orderly marketplace” and not “falling off a cliff.”

Wednesday, Sep 21, 2022 – 11:20 AM

By Greg Miller of FreightWaves

{kind=link}

The decline may indeed be fairly steady, as opposed to the sudden, violent swings seen in bulk commodity shipping. Yet spot container rates appear to be falling more rapidly than some liner executives expected.

Stifel analyst Ben Nolan recently met with executives of Matson. “In our meetings, management indicated that … the downward softening has been much steeper and less orderly in the past two months,” Nolan wrote in a client note on Sunday.

Matson introduced its third trans-Pacific service — China-California Express — in June 2021 to meet booming demand. During the Aug. 1 conference call, Cox said CCX would run through October. It didn’t.

“As a result [of softening demand] the company has completed the last sailing of the temporary CCX service ahead of the targeted October conclusion date,” said Nolan.

Steepest decline in Asia-West Coast market

“Spot rates continue to plummet,” said Clarksons Securities analyst Frode Mørkedal on Monday. “The Shanghai-U.S. West Coast corridor has seen the most significant adjustment.”

The Freightos Baltic Daily Index China-West Coast assessment has fallen 76% over the past six months, to $3,799 per forty-foot equivalent unit as of Friday. The Drewry Shanghai-Los Angeles assessment is down 57% in the same period.

{kind=link}

In the week reported Thursday, the Drewry rate for Shanghai-LA fell another 11% week on week. The prior week, it had dropped 14%. “There is no clarity with respect to when or where market rates may bottom,” said Nolan.

More blank sailings predicted after Golden Week

The initial COVID-19 lockdowns in Europe and the U.S. slashed import demand in the second quarter of 2020. Ocean carriers were able to “blank” (cancel) enough sailings to bring capacity down in line with demand. Carriers successfully stopped the spot-rate slide.

What happened in that earlier period is frequently cited as proof that carriers can blank sailings in the future if demand falls too low, putting a floor on rates. “We would expect ships to be removed from vessel services,” said Mørkedal.

Sources told Platts they’re looking to China’s Golden Week holiday (Oct. 1-7) as a potential turning point. Market participants are “bracing for a blank sailing program to be announced by carriers,” reported Platts. “Most sources expect the period immediately after Golden Week to be marked by a tonnage reshuffling as carriers look to balance capacity against the evolving marketplace.”

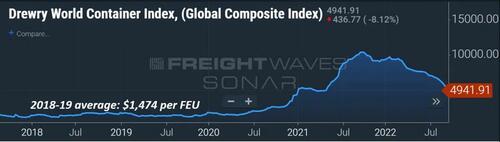

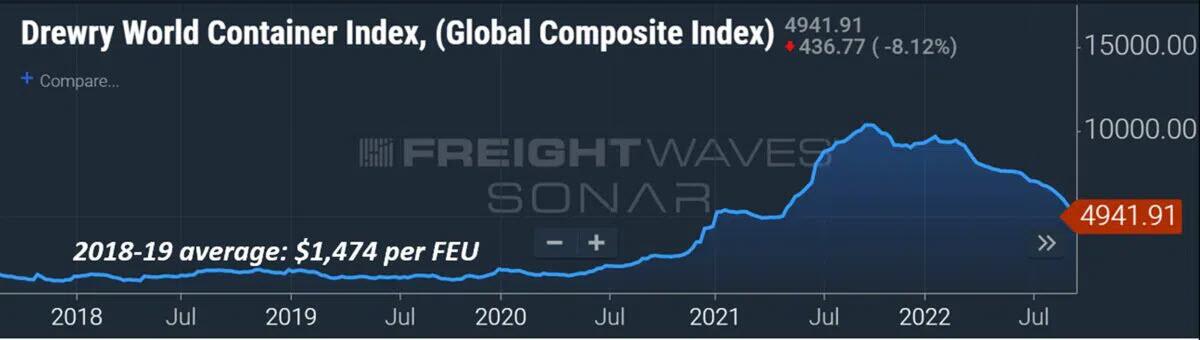

Spot rates still nowhere near past levels

Looking back to Q2 2020, the Drewry Global Composite Index fell to a low of $1,446 per FEU in late April. Blank sailings by carriers kept rates from falling even lower amid lockdowns.

{kind=link}

Prior to the pandemic, Drewry’s global index averaged $1,474 per FEU in 2018-2019. Several carriers lost money in those years.

As of last Thursday, Drewry’s global index was at $4,942 per FEU, still 3.4 times higher than the pre-COVID average and the COVID lockdown low — even after a 44% decline over the past half year, an average drop of $650 per FEU per month.

{kind=link}

If this same pace of decline were to continue, the Drewry global index would not reach pre-COVID levels until mid-Q1 2023.

If the same pace of decline continued for the next three months, the index would still be double pre-COVID levels.

Contract rates support carrier profits

Furthermore, a decline in spot rates does not have the same effect on ocean carriers as it did pre-pandemic because of changes in the contract market.

Carriers have more of their volume on annual contracts. In 2019, Maersk said it had only 46% of its long-haul business on long-term contracts. It now has 71% secured for one or more years.

Contract rates are also dramatically higher than they used to be. While a portion of this year’s contract business will be renegotiated, or not honored, the remainder will allow carriers to offset spot-business declines.

Chart source: Xeneta

Ocean carrier Zim said its contract rates this year were double 2021’s. Hikes of 50% or more were reported by carriers in 2021 versus 2020. Xeneta publishes an index that tracks long-term freight rates. Its global index hit 453 points in August, about 4.5 times pre-COVID levels. The index is up 121% year on year.

Thus, not only do spot rates still have a long way to fall before they’re back where they started — even at the steeper-than-expected pace of decline — they’re also overshadowed by contract rates when it comes to near-term carrier profits and shipper costs.

https://www.zerohedge.com/economics/fall-container-spot-rates-much-steeper-less-orderly-expected

September 20, 2022

Housing Upside but Concern

In a nice surprise to the upside, the Census Bureau housing report indicated that housing starts jumped a larger-than-expected 12.2% to a 1.575-million-unit pace, leaving starts off only 0.1% Y/Y. Both single-family and multi-family segments gained. Starts peaked in April at a 1.805-million-unit pace. With the rebound in mortgage interest rates, we may see housing starts reverse direction again in September. The more forward-looking building permits, however, continued to decline, falling by 10.0%, to a 1.517-million-unit pace. The weakness was both segments, leaving total building permits off 14.4% Y/Y. The single-family segment is more sensitive to higher interest rates and housing costs, and the August weakness reflects eroding affordability. There are several measures in the report that reflect an easing of the labor and material shortages that homebuilders are facing. The number of housing units authorized but not started fell and housing units under construction rose. Housing completions, however, declined.

Yesterday, the National Association of Home Builders (NAHB) reported that homebuilder confidence (as measured by the NAHB Housing Market Index) dropped three points to 46 in September, a more negative reading. This marked the ninth consecutive decline and is the lowest level since May 2014. Confidence was hurt by elevated interest rates, persistent building material supply chain disruptions, and high home prices that continue to take a toll on affordability. The gauge for the traffic of prospective buyers fell further into negative territory.

The National Association of Realtors (NAR) housing-affordability index, which factors in family incomes, mortgage rates and the sales price for existing single-family homes, is near its lowest level since 1989. That is, it is more expensive to buy a U.S. home that it has been in more than three decades.

Freddie Mac reported that the average rate on a 30-year fixed mortgage rate climbed to over 6.0% recently, the highest level since 2008. As a result, more borrowers are choosing adjustable-rate loans to make lower payments now with the hope of refinancing later. This will create risk down the road.

September 20, 2022

Housing Upside but Concern

In a nice surprise to the upside, the Census Bureau housing report indicated that housing starts jumped a larger-than-expected 12.2% to a 1.575-million-unit pace, leaving starts off only 0.1% Y/Y. Both single-family and multi-family segments gained. Starts peaked in April at a 1.805-million-unit pace. With the rebound in mortgage interest rates, we may see housing starts reverse direction again in September. The more forward-looking building permits, however, continued to decline, falling by 10.0%, to a 1.517-million-unit pace. The weakness was both segments, leaving total building permits off 14.4% Y/Y. The single-family segment is more sensitive to higher interest rates and housing costs, and the August weakness reflects eroding affordability. There are several measures in the report that reflect an easing of the labor and material shortages that homebuilders are facing. The number of housing units authorized but not started fell and housing units under construction rose. Housing completions, however, declined.

Yesterday, the National Association of Home Builders (NAHB) reported that homebuilder confidence (as measured by the NAHB Housing Market Index) dropped three points to 46 in September, a more negative reading. This marked the ninth consecutive decline and is the lowest level since May 2014. Confidence was hurt by elevated interest rates, persistent building material supply chain disruptions, and high home prices that continue to take a toll on affordability. The gauge for the traffic of prospective buyers fell further into negative territory.

The National Association of Realtors (NAR) housing-affordability index, which factors in family incomes, mortgage rates and the sales price for existing single-family homes, is near its lowest level since 1989. That is, it is more expensive to buy a U.S. home that it has been in more than three decades.

Freddie Mac reported that the average rate on a 30-year fixed mortgage rate climbed to over 6.0% recently, the highest level since 2008. As a result, more borrowers are choosing adjustable-rate loans to make lower payments now with the hope of refinancing later. This will create risk down the road.

September 20, 2022

Olin Reduces Guidance

Olin Updates Third Quarter 2022 Outlook and Announces Earnings Conference Call

Sep. 20, 2022 8:00 AM ETOlin Corporation (OLN)

CLAYTON, Mo., Sept. 20, 2022 /PRNewswire/ — Olin Corporation (OLN) announced today it now expects third quarter 2022 adjusted EBITDA to be in the range of $530 – $550 million. On July 28, 2022, we previously guided third quarter 2022 adjusted EBITDA to decline approximately 15% from our second quarter 2022 adjusted EBITDA of $727 million.

Scott Sutton, Chairman, President, and Chief Executive Officer, said, “We have seen global economic conditions worsen faster than expected with an accelerated deterioration in both European and North American demand particularly in epoxy and vinyls intermediates, which has been aggravated by increased Chinese exports precipitated by continuing weak Chinese domestic demand. Winchester experienced lower than expected commercial ammunition volumes as customers’ supply chain inventories were overfilled across some ammunition calibers. Olin proactively further reduced our participation in these weaker markets and increased our purchases of global product liquidity. Olin’s proactive actions and strategy have us well-positioned with a strong balance sheet, meaningful levered free cash flow, and solid positive earnings profile, to deliver on our previously anticipated recession scenario results in fourth quarter 2022 and continuing into 2023. Core electrochemical unit (ECU) pricing for merchant chlorine and caustic soda continues to move higher.”

September 20, 2022

Olin Reduces Guidance

Olin Updates Third Quarter 2022 Outlook and Announces Earnings Conference Call

Sep. 20, 2022 8:00 AM ETOlin Corporation (OLN)

CLAYTON, Mo., Sept. 20, 2022 /PRNewswire/ — Olin Corporation (OLN) announced today it now expects third quarter 2022 adjusted EBITDA to be in the range of $530 – $550 million. On July 28, 2022, we previously guided third quarter 2022 adjusted EBITDA to decline approximately 15% from our second quarter 2022 adjusted EBITDA of $727 million.

Scott Sutton, Chairman, President, and Chief Executive Officer, said, “We have seen global economic conditions worsen faster than expected with an accelerated deterioration in both European and North American demand particularly in epoxy and vinyls intermediates, which has been aggravated by increased Chinese exports precipitated by continuing weak Chinese domestic demand. Winchester experienced lower than expected commercial ammunition volumes as customers’ supply chain inventories were overfilled across some ammunition calibers. Olin proactively further reduced our participation in these weaker markets and increased our purchases of global product liquidity. Olin’s proactive actions and strategy have us well-positioned with a strong balance sheet, meaningful levered free cash flow, and solid positive earnings profile, to deliver on our previously anticipated recession scenario results in fourth quarter 2022 and continuing into 2023. Core electrochemical unit (ECU) pricing for merchant chlorine and caustic soda continues to move higher.”