Epoxy

November 1, 2021

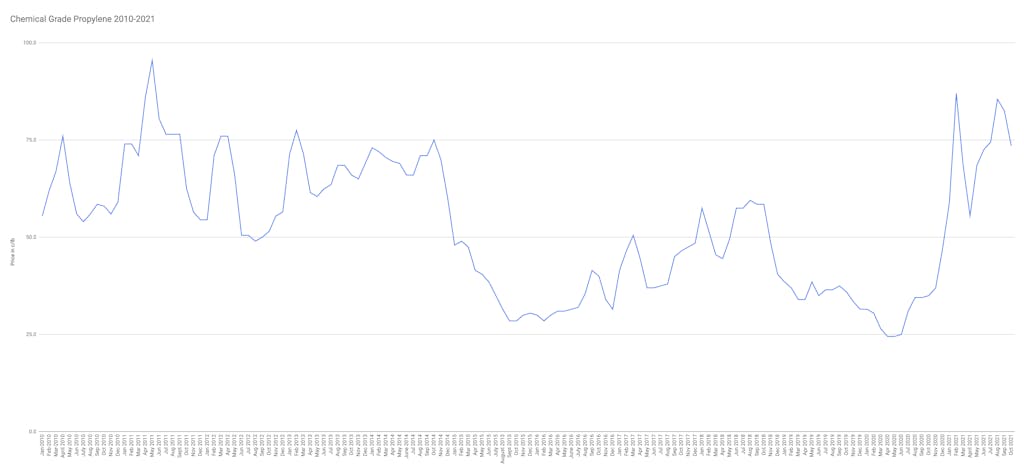

October Propylene Settles Down 9c/lb

Chemical grade is $0.735/lb

November 1, 2021

October Propylene Settles Down 9c/lb

Chemical grade is $0.735/lb

October 29, 2021

US Steel Discusses Automotive Builds

Surprising Disclosure From US Steel Suggests Chip Shortage Is Finally Over

by Tyler DurdenFriday, Oct 29, 2021 – 02:54 PM

Earlier this week, Morgan Stanley showed that more than inflation, more than concerns about the historic labor crisis, definitely more than covid, one thing has preoccupied the minds of most management teams this quarter: “supply chain issues“, a topic which has seen an explosion of mentions on Q3 earnings calls.

But while by now everyone is aware that the global supply-chain shock is truly historic and getting worse by the day, with used car prices rising sharply again and over 30 million tons of cargo waiting outside US ports ahead of the holiday season, few have considered what realistically could normalize these frayed supply chains.

To address this topic, we discussed a research report from Goldman Sachs in which the bank’s economists listed what they viewed as the three key drivers of supply chain normalization and their most likely timing:

- improved chip supply driven by post-Delta factory restarts (4Q21) and eventually by expanded production capacity (2H22 and 2023);

- improved US labor supply (4Q21 and 1H22); and

- the wind-down of US port congestion (2H22).

While some viewed Goldman’s forecast for a Q4 improvement in chip supply chains – a critical factor for renormalizing auto production – as overly optimistic a little noticed comment in today’s US Steel conference call suggests that Goldman may have been spot on.

Earlier today, US Steel jumped as much as 15%, its biggest gain since March 8, after the company announced a stock buyback, a hike in dividends and third-quarter EPS that beat analyst expectations. But it’s what US Steel CEO David Burritt said toward the end of the prepared remarks in its conference call that was most surprising.

Discussing the demand picture heading into Q4 and the new year, Burritt said that he was “delighted to hear from multiple auto customers, who are foreshadowing that the trough of the chip shortage could be behind us. They’re beginning to add to the fourth quarter and first quarter build schedules, and indicating to us, increasing usage rates, starting as early as next week.“

No surprise that former JPMorgan news aggregation maven and current publisher of VitalKnowledge Media, Adam Crisafulli, called US Steel’s observation “the most important (macro) comment from any earnings call this morning.”

While it isn’t clear what specific macro economic shift may have catalyzed this improvement: after all, West Coast port logjams are about the worst they have ever been, if US Steel’s channel checks are accurate and automakers are indeed ramping up production, then one of the biggest supply chain bottlenecks may indeed now be behind us (even if there is still along way to go before the bigger picture renormalizes).

https://www.zerohedge.com/markets/surprising-disclosure-us-steel-suggests-chip-shortage-finally-over

October 29, 2021

US Steel Discusses Automotive Builds

Surprising Disclosure From US Steel Suggests Chip Shortage Is Finally Over

by Tyler DurdenFriday, Oct 29, 2021 – 02:54 PM

Earlier this week, Morgan Stanley showed that more than inflation, more than concerns about the historic labor crisis, definitely more than covid, one thing has preoccupied the minds of most management teams this quarter: “supply chain issues“, a topic which has seen an explosion of mentions on Q3 earnings calls.

But while by now everyone is aware that the global supply-chain shock is truly historic and getting worse by the day, with used car prices rising sharply again and over 30 million tons of cargo waiting outside US ports ahead of the holiday season, few have considered what realistically could normalize these frayed supply chains.

To address this topic, we discussed a research report from Goldman Sachs in which the bank’s economists listed what they viewed as the three key drivers of supply chain normalization and their most likely timing:

- improved chip supply driven by post-Delta factory restarts (4Q21) and eventually by expanded production capacity (2H22 and 2023);

- improved US labor supply (4Q21 and 1H22); and

- the wind-down of US port congestion (2H22).

While some viewed Goldman’s forecast for a Q4 improvement in chip supply chains – a critical factor for renormalizing auto production – as overly optimistic a little noticed comment in today’s US Steel conference call suggests that Goldman may have been spot on.

Earlier today, US Steel jumped as much as 15%, its biggest gain since March 8, after the company announced a stock buyback, a hike in dividends and third-quarter EPS that beat analyst expectations. But it’s what US Steel CEO David Burritt said toward the end of the prepared remarks in its conference call that was most surprising.

Discussing the demand picture heading into Q4 and the new year, Burritt said that he was “delighted to hear from multiple auto customers, who are foreshadowing that the trough of the chip shortage could be behind us. They’re beginning to add to the fourth quarter and first quarter build schedules, and indicating to us, increasing usage rates, starting as early as next week.“

No surprise that former JPMorgan news aggregation maven and current publisher of VitalKnowledge Media, Adam Crisafulli, called US Steel’s observation “the most important (macro) comment from any earnings call this morning.”

While it isn’t clear what specific macro economic shift may have catalyzed this improvement: after all, West Coast port logjams are about the worst they have ever been, if US Steel’s channel checks are accurate and automakers are indeed ramping up production, then one of the biggest supply chain bottlenecks may indeed now be behind us (even if there is still along way to go before the bigger picture renormalizes).

https://www.zerohedge.com/markets/surprising-disclosure-us-steel-suggests-chip-shortage-finally-over

October 29, 2021

Huntsman Q3 Results

Huntsman Announces Improved Third Quarter 2021 Earnings; Repurchases Approximately $102 million of Shares During the Quarter; Wins Significant Arbitration Award Against Albemarle

Download as PDF October 29, 2021 6:00am EDT

Related Documents

Audio Earnings WebcastEarnings Slides PDF

THE WOODLANDS, Texas, Oct. 29, 2021 /PRNewswire/ —

Third Quarter Highlights

- Third quarter 2021 net income of $225 million compared to net income of $57 million in the prior year period; third quarter 2021 diluted earnings per share of $0.94 compared to diluted earnings per share of $0.22 in the prior year period.

- Third quarter 2021 adjusted net income of $239 million compared to adjusted net income of $70 million in the prior year period; third quarter 2021 adjusted diluted earnings per share of $1.08 compared to adjusted diluted earnings per share of $0.32 in the prior year period.

- Third quarter 2021 adjusted EBITDA of $371 million compared to $188 million in the prior year period.

- Third quarter 2021 net cash provided by operating activities from continuing operations was $186 million. Free cash flow from continuing operations was $110 million for the third quarter 2021.

- Balance sheet is strong with a net leverage of 0.9x and total liquidity of approximately $2 billion.

- Repurchased approximately 4 million shares for approximately $102 million in the third quarter 2021.

- On October 28, 2021, Huntsman won an arbitration award against Albemarle for fraud and breach of contract in excess of $600 million of which the Company expects to net in excess of $400 million after attorney’s fees.

| Three months ended | Nine months ended | |||||||

| September 30, | September 30, | |||||||

| In millions, except per share amounts | 2021 | 2020 | 2021 | 2020 | ||||

| Revenues | $ 2,285 | $ 1,510 | $ 6,146 | $ 4,350 | ||||

| Net income | $ 225 | $ 57 | $ 497 | $ 706 | ||||

| Adjusted net income(1) | $ 239 | $ 70 | $ 577 | $ 105 | ||||

| Diluted income per share | $ 0.94 | $ 0.22 | $ 2.02 | $ 3.13 | ||||

| Adjusted diluted income per share(1) | $ 1.08 | $ 0.32 | $ 2.60 | $ 0.47 | ||||

| Adjusted EBITDA(1) | $ 371 | $ 188 | $ 994 | $ 407 | ||||

| Net cash provided by operating activities from continuing operations | $ 186 | $ 65 | $ 163 | $ 110 | ||||

| Free cash flow from continuing operations(2) | $ 110 | $ 11 | $ (87) | $ (60) | ||||

| Adjusted free cash flow from continuing operations(6) | $ 110 | $ 189 | $ (84) | $ 128 | ||||

| See end of press release for footnote explanations and reconciliations of non-GAAP measures. |

Huntsman Corporation (NYSE: HUN) today reported third quarter 2021 results with revenues of $2,285 million, net income of $225 million, adjusted net income of $239 million and adjusted EBITDA of $371 million.

Peter R. Huntsman, Chairman, CEO and President, commented:

“We are pleased with the strong earnings we delivered in the third quarter. Despite pockets of disruption in our supply chain and cost inflation, we see strong pent-up demand across most of our businesses with favorable pricing dynamics. In addition, we are benefiting from cost reduction programs and synergies from the acquisitions we completed over the past 18 months. As indicated in our second quarter earnings call, we resumed share repurchases and we used free cash flow generated in the quarter to repurchase approximately $102 million of our stock during the quarter at an average price of $25.64 per share.

Since 2017, we have divested approximately 40% of our portfolio, including much of our commodity product lines, while adding numerous differentiated and higher margin products to the portfolio through bolt–on acquisitions. Our investment grade balance sheet remains strong and, together with our cash generation, provides us with the opportunity to continue to return capital to shareholders and further our portfolio transformation with additional bolt–on acquisitions when they make strategic and financial sense. In addition, we are investing in high return organic projects that will increase our total returns and improve margins over the next 24 to 36 months.

I also want to recognize the efforts of our corporate leadership team as well as our Board of Directors in connection with our arbitration award announced yesterday afternoon. This was a multi-year effort that could not have been won without their support, integrity and cohesion.

We have a bright future, remain focused on improving the quality of our margins, and look forward to discussing the Company’s strategy at our Investor Day on November 9th in New York City.”

Segment Analysis for 3Q21 Compared to 3Q20

Polyurethanes

The increase in revenues in our Polyurethanes segment for the three months ended September 30, 2021, compared to the same period of 2020 was largely due to higher MDI average selling prices and slightly higher sales volumes. MDI average selling prices increased in all our regions. Sales volumes increased primarily due to stronger demand in relation to the ongoing recovery from the global economic slowdown, partially offset by the impact of Hurricane Ida at our Geismar, Louisiana facility that occurred in the third quarter of 2021. The increase in segment adjusted EBITDA was primarily due to higher MDI margins resulting from higher MDI pricing and slightly higher sales volumes as well as stronger earnings from our PO/MTBE joint venture in China, partially offset by higher raw material costs.

Performance Products

The increase in revenues in our Performance Products segment for the three months ended September 30, 2021, compared to the same period of 2020 was primarily due to higher average selling prices and higher sales volumes. Average selling prices increased primarily due to stronger demand in relation to the ongoing recovery from the global economic slowdown as well as in response to an increase in raw material costs. Sales volumes also increased primarily due to stronger demand. The increase in segment adjusted EBITDA was primarily due to increased revenue and margins, partially offset by increased fixed costs.

Advanced Materials

The increase in revenues in our Advanced Materials segment for the three months ended September 30, 2021, compared to the same period in 2020 was primarily due to higher sales volumes, higher average selling prices and the favorable net impact of the Gabriel Acquisition and the sale of the India-based DIY business. Excluding our recent acquisition and divestiture, sales volumes increased across all of our specialty markets, primarily in relation to the ongoing recovery from the global economic slowdown. Average selling prices increased largely in response to higher raw material costs. The increase in segment adjusted EBITDA was primarily due to higher sales volumes and the benefit from our recent acquisition.

Textile Effects

The increase in revenues in our Textile Effects segment for the three months ended September 30, 2021, compared to the same period of 2020 was due to higher sales volumes and higher average selling prices. Sales volumes increased primarily due to increased demand resulting from the ongoing recovery from the global economic slowdown, particularly in the North Asia and Americas regions. Average selling prices increased primarily in response to higher freight and logistics costs. The increase in segment adjusted EBITDA was primarily due to higher sales revenues, partially offset by higher fixed costs.

Corporate, LIFO and other

For the three months ended September 30, 2021, adjusted EBITDA from Corporate and other decreased by $11 million to a loss of $48 million from a loss of $37 million for the same period of 2020.

Liquidity and Capital Resources

During the three months ended September 30, 2021, our adjusted free cash flow from continuing operations was $110 million as compared to $189 million in the prior year period. As of September 30, 2021, we had approximately $2 billion of combined cash and unused borrowing capacity.

During the three months ended September 30, 2021, we spent $76 million on capital expenditures as compared to $54 million in the same period of 2020. For 2021, we expect to spend approximately $350 million on capital expenditures.

Income Taxes

In the third quarter 2021, our adjusted effective tax rate was 15%. For 2021, our adjusted effective tax rate is expected to be approximately 19% to 20%. We continue to expect our forward adjusted effective tax rate will be approximately 22% to 24%

Albemarle Litigation

On October 28, 2021, a panel of three former federal judges sitting as arbitrators found that Albemarle (and its predecessor Rockwood) had defrauded Huntsman in connection with the sale of its pigments business in 2014, breached the contract under which the business was sold, and awarded Huntsman in excess of $600 million for the fraud and breach, inclusive of punitive damages and statutory interest at 9% of which the Company expects to net in excess of $400 million after attorney’s fees. The award is subject to confirmation and limited appeal in the New York state court.

Earnings Conference Call Information

We will hold a conference call to discuss our third quarter 2021 financial results on Friday October 29, 2021 at 10:00 a.m. ET.

Webcast link: https://78449.themediaframe.com/dataconf/productusers/hun/mediaframe/46827/indexl.html

| Participant dial-in numbers: | |

| Domestic callers: | (877) 402-8037 |

| International callers: | (201) 378-4913 |

The conference call will be accompanied by presentation slides that will be accessible via the webcast link and Huntsman’s investor relations website, www.huntsman.com/investors. Upon conclusion of the call, the webcast replay will be accessible via Huntsman’s website.