The Urethane Blog

Everchem Updates

VOLUME XXI

September 14, 2023

Everchem’s exclusive Closers Only Club is reserved for only the highest caliber brass-baller salesmen in the chemical industry. Watch the hype video and be introduced to the top of the league: — read more

May 20, 2021

Why Stratospheric Container Rates Could Rocket Even Higher

by Tyler DurdenThursday, May 20, 2021 – 11:35 AM

By Greg Miller of Freight Waves,

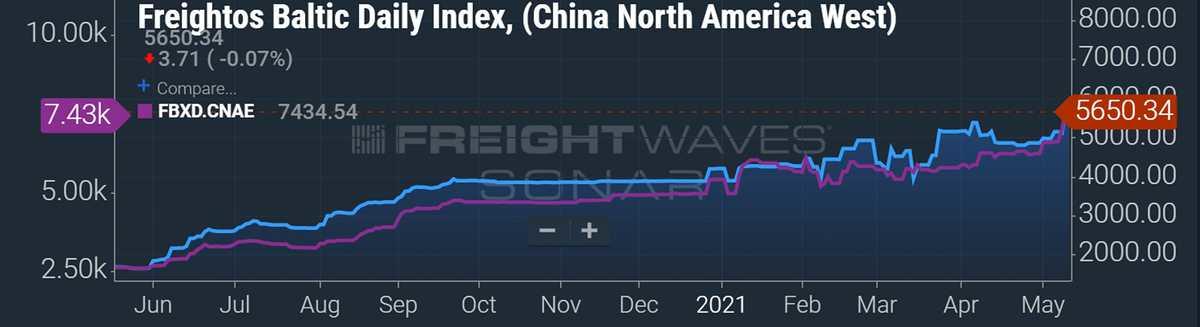

Spot ocean container rates are up triple digits year on year, ergo they must be near their peak. They’re so high they don’t have much more room to run. So goes a common belief in the container market, despite the fact that this premise has already been proven wrong, and that container rates could theoretically have a lot more room to run if the upper limit is defined the same way it is in non-containerized shipping.

One leading freight-forwarder executive told American Shipper in August 2020 after the initial spike, “I do not think there is room for growth beyond $4,000 [per forty-foot equivalent unit or FEU].” Nine months later, many all-in trans-Pacific rates including premium charges are more than double that — and rising sustainably. Importers commonly pay $8,000-$10,000 per FEU or more, including extra charges, sometimes a lot more.Spot rates do not include $3,000-$5,000 per FEU premiums now reportedly being paid by some shippers. FBXD.CNAE = China-East Coast

{kind=link}

But why stop there?

Retail inventories-to-sales ratios are still at historic lows, stimulus checks are still supporting spending, and the traditional peak season is right around the corner. Meanwhile, U.S. households accumulated an enormous amount of excess savings during the pandemic (equivalent to 12% of GDP, according to Moody’s) that may now be unleashed.

What if the high-end case for U.S. import demand plays out over the rest of this year and exceeds vessel and equipment supply even more so than it does today?

A common response from shippers in online forums is that regulators will intervene if rates go too high. That’s not going to happen, at least in the U.S. During a presentation last week, Federal Maritime Commission (FMC) Chairman Daniel Maffei made clear that if high freight prices are being caused by market forces, there’s nothing the FMC can currently do about it.

How bulk shipping rates are capped

The current rate spike is unprecedented in the history of container shipping. The sector is in completely unchart(er)ed territory (one reason why rate predictions over the past nine months have been repeatedly wrong). However, there is an extensive history of precedents in non-containerized shipping — in crude tanker, gas carrier and dry bulk markets — that shed light on how high the maximum spot rate can go.

The freight rate of a spot cargo in bulk commodity shipping is elastic all the way up to the point where it erases the profit margin of the shipper. Rates for very large crude carriers (VLCCs, tankers that carry 2 million barrels of oil) topped $200,000 per day in October 2019 and March-April 2020. A liquefied natural gas carrier was booked at $350,000 per day in January.

An example of the upper limit being hit was recounted by Trygve Munthe, co-CEO of crude-tanker owner DHT. Referring to the rate peak in the second week of October 2019, he said, “When you get to that kind of freight level, you make it very hard for the refiners to make money. In that crazy week, we happened to be in Korea meeting with a lot of refiners, and they told us that at those freight levels, it just didn’t make sense for them. They said they would just pull back on their [refining] throughputs.”

Stifel analyst Ben Nolan explained the max-rate calculation for Capesizes (dry bulk ships with a capacity of around 180,000 deadweight tons) in a research note titled “How High Can You Go?” published last week.

“Turns out, at current commodity prices … the dry bulk market is nowhere close to its theoretical ceiling,” he wrote. “If demand exceeds supply, the primary upward constraint of ship freight cost is the point at which it absorbs the profit of the producer or shipper.”

He noted that the landed price of thermal coal in China last week was about $125 per ton and the producer breakeven was $60 per ton, meaning the transport costs could be as much as $65 per ton. Capesize rates were then around $13 per ton (the equivalent of $40,000 per day), meaning “freight rates would need to rise seven times or to around $300,000 per day before the economics are completely destroyed by freight costs.”

Applying bulk shipping rate cap to containers

In an interview on Friday, American Shipper asked Jefferies shipping analyst Randy Giveans how this max-spot-rate concept applies to container shipping.

The big difference with bulk commodity shipping is transparency on the cargo price and margins. “With tankers, you know the commodity you’re moving. You know the exact price of Brent. With floating storage economics, you can say the prompt month price is x, the price six or 12 months later is y, here’s the carry trade, so here’s what you can charge for a VLCC to operate in floating storage.

“It’s similar with dry bulk, although you’re not doing floating storage. You can still say: The delivered cost of iron ore in China is $150-$200 per ton, it costs maybe $30 or $40 per ton [to produce] in Brazil and $50 in Australia and Capesize [transport] rates are maybe $30 per ton from Brazil and $10-$12 from Australia, so there are still huge margins and rates from Brazil for iron-ore [shipping] could go up three times.”

Container shipping is much more opaque. “This is a lot harder [to calculate] for containerized goods because you don’t know exactly what’s in those boxes,” he said. “Is it large stuffed animals or is it iPhones and iPads with much higher value and lower weight?”

The key is how the total containerized transport cost, including ocean and land, relates to the margin of the goods. “Let’s say a pair of shoes costs $10 to produce and sells for $100-$200. You can fit a lot of shoes in a container. If the transport cost is $5-$10 per pair and then it rises to $20, who cares? There’s still a huge margin there,” he said.

On the other hand, there have been reported cases of certain imported goods already getting priced out by rising ocean spot rates. “There are goods with lower margins and we’ve heard of some retailers saying it’s too expensive for me to take the cargo,” acknowledged Giveans. “But I think there are a lot fewer items like that than there are items with margins [that can still handle even higher transport costs].”

The spot-rate equation also changes as importers pass along transport costs to consumers. “The cost of everything is going up. You’re seeing inflation of the cost of goods. Even the price of low-margin materials is going higher and part of that is the increased shipping cost is being passed along to the customers,” said Giveans.

To apply the bulk commodity shipping equation to container shipping: If you subtract all the volume covered by fixed-price contracts, the spot rate on the remaining trans-Pacific volume could theoretically increase to the extent that there is enough demand to fill that remaining volume with goods from shippers who will accept even higher rates, whether because their margin is high enough to absorb it or because of their ability to pass along costs to consumers. If some low-margin imports are priced out, higher-margin goods could supplant them and keep rates rising.

Differences between bulk and container shipping

In tanker and bulker shipping, the cycles over the decades have been characterized by long periods of below-breakeven rates or small profits, accentuated by repeated brief periods of extremely high rates.

Shippers offer spot bulk cargoes to the vessels in the vicinity and generally take the lowest freight bid. During rate spikes, if the lowest bid is extremely high, shippers pay it if they can still make a margin on the trade and refuse it if they can’t. They don’t begrudge the vessel interest for offering a high spot rate; they blame the temporary supply-demand imbalance.

In container shipping, the past decades have been overwhelmingly dominated by heavy losses for carriers, several of which would no longer exist if not for government rescues. Containerized cargo shippers do not have the same institutional memory of extreme rate spikes as bulk cargo shippers.

Containerized cargo shippers also have more contract versus spot business with carriers than in the crude and dry bulk trades, and thus, there is more risk of relationship damage with carriers during periods of extreme spot-rate highs. Unlike shippers in bulk commodity trades, container shippers are blaming carriers for taking advantage of the supply-demand imbalance, even though shippers benefited from the imbalance in the opposite direction for decades.

That relationship factor might, perhaps, keep liners from being as aggressive on pricing as they might otherwise be. “I could understand how a liner maybe doesn’t want to really put the screws on its customers,” Giveans said.

Can US regulators intervene?

Another difference between bulk commodity shipping and container shipping is that container shipping, unlike bulk shipping, is regulated, at least to some extent.

However, in the U.S., the FMC cannot intervene on high pricing unless it is deemed “unreasonable” from a market perspective or as the direct result of lack of competition via alliances. Maffei of the FMC addressed the current market crunch during a Port of Los Angeles presentation on Thursday.

“The fact is that we have an incredibly vibrant global freight system, and right now that system is at and beyond capacity,” he said.

“We have a pretty limited set of tools. … We can investigate the alliances and if necessary, challenge them in court if we feel they are creating unreasonably high costs because of the alliances. We have looked at that pretty extensively and will continue to do so. But so far, there’s just no evidence that the alliances themselves are engaging in any behavior that would allow us to take them to court.

“High price in and of itself is not a violation of the Shipping Act,” he continued. “We don’t set rates and we can’t dictate the levels of service. What we can do is continue to monitor carriers to make sure alliances, by their very existence, don’t mean that there will be an unreasonably diminished level of service or unreasonably increased cost.

“But the key is that when you’re at or beyond the capacity of the system, it’s very difficult to prove that if only this [carrier consolidation] didn’t exist, prices would be lower. Because the fact is that it’s simply supply and demand. If demand is high and supply remains fairly limited, then that [high prices] is what happens.

“One thing I am doing is talking to my former colleagues in Congress. Some have asked: Could we change the Shipping Act? And of course, they can change the Shipping Act. But in terms of our current act, a high price in and of itself is not a violation.”

American Shipper asked Peter Freidmann, a lobbyist at the Agriculture Transportation Coalition, which represents exporters of containerized goods, whether he had heard of any current proposals to reform the Shipping Act to in any way limit ocean freight pricing.

Freidmann responded: “I am not aware of any effort or proposal to control or establish freight rates, now, or at any time since the Shipping Acts were written. In the past, competition between carriers served to keep freight rates affordable, even if sometimes they were very high. But then, there were 20-plus carriers. Now, there are 10 major east-west carriers, and they are consolidated into three alliances. So, practically speaking, shippers are finding that there are really only three carriers left.”

Will Chinese regulators throttle liners?

If U.S. regulators cannot throttle trans-Pacific freight pricing, what about Chinese regulators?

Chinese officials called a meeting with ocean liners on Sept. 11, 2020. During a client call in early October, Jefferies analyst Andrew Lee recounted, “What we heard from the [people in the] meeting themselves was that it wasn’t [regulators saying], ‘You’ve got to cut the rates.’ It was, ‘Carriers are making a lot of money on the trans-Pacific at the moment. Let’s not push it much higher.’”

Trans-Pacific spot-rate indexes plateaued in the months after that meeting, lending some credence to the theory that liners were somehow bowing to Chinese pressure. However, the actual all-in rates including premiums did not plateau and today’s trans-Pacific spot-rate index levels are far higher than they were at the time of last September’s China meeting.

According to Giveans, “I think there certainly was [some fear of regulators] in the fall and winter, where some governments were pushing back and saying, ‘Don’t get too crazy’ because they felt their goods would have to be discounted because the shipping costs were so high.

“But I think because prices [to consumers] have continued to go up and because there’s still so much demand, that has been alleviated. This is a free market.”

https://www.zerohedge.com/economics/why-stratospheric-container-rates-could-rocket-even-higher

May 20, 2021

Why Stratospheric Container Rates Could Rocket Even Higher

by Tyler DurdenThursday, May 20, 2021 – 11:35 AM

By Greg Miller of Freight Waves,

Spot ocean container rates are up triple digits year on year, ergo they must be near their peak. They’re so high they don’t have much more room to run. So goes a common belief in the container market, despite the fact that this premise has already been proven wrong, and that container rates could theoretically have a lot more room to run if the upper limit is defined the same way it is in non-containerized shipping.

One leading freight-forwarder executive told American Shipper in August 2020 after the initial spike, “I do not think there is room for growth beyond $4,000 [per forty-foot equivalent unit or FEU].” Nine months later, many all-in trans-Pacific rates including premium charges are more than double that — and rising sustainably. Importers commonly pay $8,000-$10,000 per FEU or more, including extra charges, sometimes a lot more.Spot rates do not include $3,000-$5,000 per FEU premiums now reportedly being paid by some shippers. FBXD.CNAE = China-East Coast

But why stop there?

Retail inventories-to-sales ratios are still at historic lows, stimulus checks are still supporting spending, and the traditional peak season is right around the corner. Meanwhile, U.S. households accumulated an enormous amount of excess savings during the pandemic (equivalent to 12% of GDP, according to Moody’s) that may now be unleashed.

What if the high-end case for U.S. import demand plays out over the rest of this year and exceeds vessel and equipment supply even more so than it does today?

A common response from shippers in online forums is that regulators will intervene if rates go too high. That’s not going to happen, at least in the U.S. During a presentation last week, Federal Maritime Commission (FMC) Chairman Daniel Maffei made clear that if high freight prices are being caused by market forces, there’s nothing the FMC can currently do about it.

How bulk shipping rates are capped

The current rate spike is unprecedented in the history of container shipping. The sector is in completely unchart(er)ed territory (one reason why rate predictions over the past nine months have been repeatedly wrong). However, there is an extensive history of precedents in non-containerized shipping — in crude tanker, gas carrier and dry bulk markets — that shed light on how high the maximum spot rate can go.

The freight rate of a spot cargo in bulk commodity shipping is elastic all the way up to the point where it erases the profit margin of the shipper. Rates for very large crude carriers (VLCCs, tankers that carry 2 million barrels of oil) topped $200,000 per day in October 2019 and March-April 2020. A liquefied natural gas carrier was booked at $350,000 per day in January.

An example of the upper limit being hit was recounted by Trygve Munthe, co-CEO of crude-tanker owner DHT. Referring to the rate peak in the second week of October 2019, he said, “When you get to that kind of freight level, you make it very hard for the refiners to make money. In that crazy week, we happened to be in Korea meeting with a lot of refiners, and they told us that at those freight levels, it just didn’t make sense for them. They said they would just pull back on their [refining] throughputs.”

Stifel analyst Ben Nolan explained the max-rate calculation for Capesizes (dry bulk ships with a capacity of around 180,000 deadweight tons) in a research note titled “How High Can You Go?” published last week.

“Turns out, at current commodity prices … the dry bulk market is nowhere close to its theoretical ceiling,” he wrote. “If demand exceeds supply, the primary upward constraint of ship freight cost is the point at which it absorbs the profit of the producer or shipper.”

He noted that the landed price of thermal coal in China last week was about $125 per ton and the producer breakeven was $60 per ton, meaning the transport costs could be as much as $65 per ton. Capesize rates were then around $13 per ton (the equivalent of $40,000 per day), meaning “freight rates would need to rise seven times or to around $300,000 per day before the economics are completely destroyed by freight costs.”

Applying bulk shipping rate cap to containers

In an interview on Friday, American Shipper asked Jefferies shipping analyst Randy Giveans how this max-spot-rate concept applies to container shipping.

The big difference with bulk commodity shipping is transparency on the cargo price and margins. “With tankers, you know the commodity you’re moving. You know the exact price of Brent. With floating storage economics, you can say the prompt month price is x, the price six or 12 months later is y, here’s the carry trade, so here’s what you can charge for a VLCC to operate in floating storage.

“It’s similar with dry bulk, although you’re not doing floating storage. You can still say: The delivered cost of iron ore in China is $150-$200 per ton, it costs maybe $30 or $40 per ton [to produce] in Brazil and $50 in Australia and Capesize [transport] rates are maybe $30 per ton from Brazil and $10-$12 from Australia, so there are still huge margins and rates from Brazil for iron-ore [shipping] could go up three times.”

Container shipping is much more opaque. “This is a lot harder [to calculate] for containerized goods because you don’t know exactly what’s in those boxes,” he said. “Is it large stuffed animals or is it iPhones and iPads with much higher value and lower weight?”

The key is how the total containerized transport cost, including ocean and land, relates to the margin of the goods. “Let’s say a pair of shoes costs $10 to produce and sells for $100-$200. You can fit a lot of shoes in a container. If the transport cost is $5-$10 per pair and then it rises to $20, who cares? There’s still a huge margin there,” he said.

On the other hand, there have been reported cases of certain imported goods already getting priced out by rising ocean spot rates. “There are goods with lower margins and we’ve heard of some retailers saying it’s too expensive for me to take the cargo,” acknowledged Giveans. “But I think there are a lot fewer items like that than there are items with margins [that can still handle even higher transport costs].”

The spot-rate equation also changes as importers pass along transport costs to consumers. “The cost of everything is going up. You’re seeing inflation of the cost of goods. Even the price of low-margin materials is going higher and part of that is the increased shipping cost is being passed along to the customers,” said Giveans.

To apply the bulk commodity shipping equation to container shipping: If you subtract all the volume covered by fixed-price contracts, the spot rate on the remaining trans-Pacific volume could theoretically increase to the extent that there is enough demand to fill that remaining volume with goods from shippers who will accept even higher rates, whether because their margin is high enough to absorb it or because of their ability to pass along costs to consumers. If some low-margin imports are priced out, higher-margin goods could supplant them and keep rates rising.

Differences between bulk and container shipping

In tanker and bulker shipping, the cycles over the decades have been characterized by long periods of below-breakeven rates or small profits, accentuated by repeated brief periods of extremely high rates.

Shippers offer spot bulk cargoes to the vessels in the vicinity and generally take the lowest freight bid. During rate spikes, if the lowest bid is extremely high, shippers pay it if they can still make a margin on the trade and refuse it if they can’t. They don’t begrudge the vessel interest for offering a high spot rate; they blame the temporary supply-demand imbalance.

In container shipping, the past decades have been overwhelmingly dominated by heavy losses for carriers, several of which would no longer exist if not for government rescues. Containerized cargo shippers do not have the same institutional memory of extreme rate spikes as bulk cargo shippers.

Containerized cargo shippers also have more contract versus spot business with carriers than in the crude and dry bulk trades, and thus, there is more risk of relationship damage with carriers during periods of extreme spot-rate highs. Unlike shippers in bulk commodity trades, container shippers are blaming carriers for taking advantage of the supply-demand imbalance, even though shippers benefited from the imbalance in the opposite direction for decades.

That relationship factor might, perhaps, keep liners from being as aggressive on pricing as they might otherwise be. “I could understand how a liner maybe doesn’t want to really put the screws on its customers,” Giveans said.

Can US regulators intervene?

Another difference between bulk commodity shipping and container shipping is that container shipping, unlike bulk shipping, is regulated, at least to some extent.

However, in the U.S., the FMC cannot intervene on high pricing unless it is deemed “unreasonable” from a market perspective or as the direct result of lack of competition via alliances. Maffei of the FMC addressed the current market crunch during a Port of Los Angeles presentation on Thursday.

“The fact is that we have an incredibly vibrant global freight system, and right now that system is at and beyond capacity,” he said.

“We have a pretty limited set of tools. … We can investigate the alliances and if necessary, challenge them in court if we feel they are creating unreasonably high costs because of the alliances. We have looked at that pretty extensively and will continue to do so. But so far, there’s just no evidence that the alliances themselves are engaging in any behavior that would allow us to take them to court.

“High price in and of itself is not a violation of the Shipping Act,” he continued. “We don’t set rates and we can’t dictate the levels of service. What we can do is continue to monitor carriers to make sure alliances, by their very existence, don’t mean that there will be an unreasonably diminished level of service or unreasonably increased cost.

“But the key is that when you’re at or beyond the capacity of the system, it’s very difficult to prove that if only this [carrier consolidation] didn’t exist, prices would be lower. Because the fact is that it’s simply supply and demand. If demand is high and supply remains fairly limited, then that [high prices] is what happens.

“One thing I am doing is talking to my former colleagues in Congress. Some have asked: Could we change the Shipping Act? And of course, they can change the Shipping Act. But in terms of our current act, a high price in and of itself is not a violation.”

American Shipper asked Peter Freidmann, a lobbyist at the Agriculture Transportation Coalition, which represents exporters of containerized goods, whether he had heard of any current proposals to reform the Shipping Act to in any way limit ocean freight pricing.

Freidmann responded: “I am not aware of any effort or proposal to control or establish freight rates, now, or at any time since the Shipping Acts were written. In the past, competition between carriers served to keep freight rates affordable, even if sometimes they were very high. But then, there were 20-plus carriers. Now, there are 10 major east-west carriers, and they are consolidated into three alliances. So, practically speaking, shippers are finding that there are really only three carriers left.”

Will Chinese regulators throttle liners?

If U.S. regulators cannot throttle trans-Pacific freight pricing, what about Chinese regulators?

Chinese officials called a meeting with ocean liners on Sept. 11, 2020. During a client call in early October, Jefferies analyst Andrew Lee recounted, “What we heard from the [people in the] meeting themselves was that it wasn’t [regulators saying], ‘You’ve got to cut the rates.’ It was, ‘Carriers are making a lot of money on the trans-Pacific at the moment. Let’s not push it much higher.’”

Trans-Pacific spot-rate indexes plateaued in the months after that meeting, lending some credence to the theory that liners were somehow bowing to Chinese pressure. However, the actual all-in rates including premiums did not plateau and today’s trans-Pacific spot-rate index levels are far higher than they were at the time of last September’s China meeting.

According to Giveans, “I think there certainly was [some fear of regulators] in the fall and winter, where some governments were pushing back and saying, ‘Don’t get too crazy’ because they felt their goods would have to be discounted because the shipping costs were so high.

“But I think because prices [to consumers] have continued to go up and because there’s still so much demand, that has been alleviated. This is a free market.”

https://www.zerohedge.com/economics/why-stratospheric-container-rates-could-rocket-even-higher

May 20, 2021

ROTTERDAM, The Netherlands (May 2021) – IMCD N.V. (“IMCD” or “Company”), a leading distributor of speciality chemicals and ingredients, today announces the acquisition of Andes Chemical Corp. (“Andes Chemical”). This acquisition marks IMCD’s debut in Central America and Peru, expanding its presence in Latin America and throughout the Caribbean.

“Andes Chemical further strengthens IMCD’s presence in the Americas region and opens exciting opportunities for development in countries new to our business,” said Marcus Jordan, Americas President, IMCD. “Andes Chemical’s focus on speciality chemicals and strength in a number of IMCD’s core markets was an excellent fit and perfectly complements the presence we have in the region. We are delighted to welcome the Andes Chemical team to further enhance IMCD’s Americas footprint and offering.”

Andes Chemical has been a distribution partner to leading speciality chemical manufacturers since 1986, and in 2020, generated a revenue of USD 46 million. Headquartered in the Miami metropolitan area, it is active in Caribbean and Central American countries, Colombia and Peru. Andes Chemical serves the coatings, adhesives, sealants and elastomers (CASE), construction, cosmetics, personal care, plastics, pharmaceuticals and HI&I industries.

“IMCD has displayed impressive growth over the past 25 years, so joining the company to further progress its storyline together is an exciting opportunity for us and our partners,” said Fernando J. Espinosa, Jr., President, Andes Chemical. “We are ready to accelerate the growth potential with IMCD in the region and are confident that the enhanced commercial capabilities and global network of formulatory specialists will add great value to both our supplier partners and customers.”

The acquisition of Andes Chemical adds 43 employees to IMCD’s Americas team, plus a CASE innovation laboratory located in Miami which provides product and formulatory support.

About IMCD N.V.

IMCD is a market-leader in the sales, marketing, and distribution of speciality chemicals and ingredients. Its result-driven professionals provide market-focused solutions to suppliers and customers across EMEA, Americas and Asia-Pacific, offering a range of comprehensive product portfolios, including innovative formulations that embrace industry trends.

Listed at Euronext, Amsterdam (IMCD), IMCD realised revenues of EUR 2,775 million in 2020 with nearly 3,300 employees in over 50 countries on 6 continents. IMCD’s dedicated team of technical and commercial experts work in close partnership to tailor best-in-class solutions and provide value through expertise for around 50,000 customers and a diverse range of world class suppliers.

For further information, please visit www.imcdgroup.com.

About Andes Chemical Corp.

Andes Chemical Corp. is a distributor of specialty chemicals throughout Latin America that provides formulation solutions and logistics, making it a preferred partner for customers and suppliers. Its state-of-the-art distribution and warehouse facility in Miami offers a hands-on approach to an international supply chain with proficiencies in freight consolidation, documentation and export regulatory compliance. Andes Chemical also manages a Customer Innovation Center, where formulation expertise and cross regional knowledge provide cost effective solutions tailored to meet the needs of customers, while serving as a local resource to suppliers. Its Miami headquarters are complemented by offices and distribution centers in Dominican Republic, Costa Rica and Peru, serving as hubs for the Caribbean, Central American, and Andean regions.

For more information, please visit www.andeschem.com.

May 20, 2021

ROTTERDAM, The Netherlands (May 2021) – IMCD N.V. (“IMCD” or “Company”), a leading distributor of speciality chemicals and ingredients, today announces the acquisition of Andes Chemical Corp. (“Andes Chemical”). This acquisition marks IMCD’s debut in Central America and Peru, expanding its presence in Latin America and throughout the Caribbean.

“Andes Chemical further strengthens IMCD’s presence in the Americas region and opens exciting opportunities for development in countries new to our business,” said Marcus Jordan, Americas President, IMCD. “Andes Chemical’s focus on speciality chemicals and strength in a number of IMCD’s core markets was an excellent fit and perfectly complements the presence we have in the region. We are delighted to welcome the Andes Chemical team to further enhance IMCD’s Americas footprint and offering.”

Andes Chemical has been a distribution partner to leading speciality chemical manufacturers since 1986, and in 2020, generated a revenue of USD 46 million. Headquartered in the Miami metropolitan area, it is active in Caribbean and Central American countries, Colombia and Peru. Andes Chemical serves the coatings, adhesives, sealants and elastomers (CASE), construction, cosmetics, personal care, plastics, pharmaceuticals and HI&I industries.

“IMCD has displayed impressive growth over the past 25 years, so joining the company to further progress its storyline together is an exciting opportunity for us and our partners,” said Fernando J. Espinosa, Jr., President, Andes Chemical. “We are ready to accelerate the growth potential with IMCD in the region and are confident that the enhanced commercial capabilities and global network of formulatory specialists will add great value to both our supplier partners and customers.”

The acquisition of Andes Chemical adds 43 employees to IMCD’s Americas team, plus a CASE innovation laboratory located in Miami which provides product and formulatory support.

About IMCD N.V.

IMCD is a market-leader in the sales, marketing, and distribution of speciality chemicals and ingredients. Its result-driven professionals provide market-focused solutions to suppliers and customers across EMEA, Americas and Asia-Pacific, offering a range of comprehensive product portfolios, including innovative formulations that embrace industry trends.

Listed at Euronext, Amsterdam (IMCD), IMCD realised revenues of EUR 2,775 million in 2020 with nearly 3,300 employees in over 50 countries on 6 continents. IMCD’s dedicated team of technical and commercial experts work in close partnership to tailor best-in-class solutions and provide value through expertise for around 50,000 customers and a diverse range of world class suppliers.

For further information, please visit www.imcdgroup.com.

About Andes Chemical Corp.

Andes Chemical Corp. is a distributor of specialty chemicals throughout Latin America that provides formulation solutions and logistics, making it a preferred partner for customers and suppliers. Its state-of-the-art distribution and warehouse facility in Miami offers a hands-on approach to an international supply chain with proficiencies in freight consolidation, documentation and export regulatory compliance. Andes Chemical also manages a Customer Innovation Center, where formulation expertise and cross regional knowledge provide cost effective solutions tailored to meet the needs of customers, while serving as a local resource to suppliers. Its Miami headquarters are complemented by offices and distribution centers in Dominican Republic, Costa Rica and Peru, serving as hubs for the Caribbean, Central American, and Andean regions.

For more information, please visit www.andeschem.com.

May 19, 2021

May 18, 2021

Polyol PRICE INCREASE

Effective June 1, 2021, or as contracts allow, The Dow Chemical Company, on behalf of

itself and its applicable consolidated subsidiaries (“Dow”), will increase list and off-list

prices by the amounts listed below on all grades and package types of the following

Polyol products in North America:

VORANOL US $0.10 / lb

VORALUX US $0.10 / lb

SPECFLEX US $0.10 / lb

Thank you for your continued business with Dow. Please contact your Account

Manager if you have any questions related to this communication.