The Urethane Blog

Everchem Updates

VOLUME XXI

September 14, 2023

Everchem’s exclusive Closers Only Club is reserved for only the highest caliber brass-baller salesmen in the chemical industry. Watch the hype video and be introduced to the top of the league: — read more

August 26, 2019

Impact of the US-China trade war on the MDI market

The polymeric methyl diphenyl diisocyanate (pMDI) market has been impacted by the latestdevelopments in the United States-China trade war. pMDI, a key polyurethane feedstock, was initially included in the list of $200 billion of Chinese imports that were tariffed by the United States Trade Representative in response to China’s trade practices. US pMDI imports from China were subject to a 10% import tariff beginning September 24, 2018. This rate was subsequently increased to 25% on May 10.

The main polyurethane feedstocks – including pMDI, monomeric methyl diphenyl diisocyanate (mMDI), toluene diisocyanate (TDI), and polyether polyols (produced via the intermediate propylene oxide) – are reacted in different combinations to produce polyurethanes. The most common product is flexible and rigid polyurethane foam.

Polyurethanes are used in a myriad of applications. The buildings we live in, the mattresses we sleep on, and the shoes we wear can all contain polyurethanes. Even surfboards are made from rigid polyurethane foam. Polyurethanes are everywhere.

The global pMDI market has been volatile lately. In 2017, supply shortages triggered by plant outages and insufficient capacity investment led to a pMDI price surge. Prices collapsed in the second half of 2018, as supply significantly improved and demand waned amid product substitution and the cooling global economy. In late-Q1 2019, the pMDI market picked up with reinvigorated demand thanks to the peak spring construction season.

However, the escalation in the US-China trade war and implementation of the 25% trade tariff will impact global pMDI demand growth and in the United States. Slower global economic growth is now forecasted. One upshot is a weaker outlook in construction activity, including in the United States, moderating growth in building insulation demand; the largest pMDI end use in the United States is in rigid polyurethane and polyisocyanurate foam based insulation. In general, IHS Markit forecasts softer pMDI demand growth compared to the healthy growth exhibited in recent years. Weakness in other sectors such as the automotive industry – an industry facing its own challenges – is also projected to stifle US pMDI demand growth.

The United States, the second largest pMDI-consuming country, has seen its pMDI trade position shift in recent years. Historically, the US was a net exporter of pMDI. Today the country still exports a substantial volume of pMDI, including more than 200,000 metric tons (mt) in 2018.

The US pMDI market has recently exhibited high demand growth rates. Yet there has not been a major greenfield MDI capacity investment in the United States for many years. As the US import requirement grew and the pMDI market structurally tightened, the US became a net importer of pMDI in 2018.

Subsequently, the US market has become dependent on imports to meet demand. Approximately 71% of the 300,000 mt of pMDI imported into the US was sourced from China. Based on IHS Markit’s US pMDI monthly index and the monthly import volume, this equates to just under $500 million worth of imports.

The introduction of the 25% tariff will ensure that volatility continues in the pMDI market, especially in the US. US pMDI prices are forecast to rise not just because the tariff increase, but also because Chinese supply is expected to moderate as exporters reduce US shipments.

The United States trade position will rebalance. pMDI imports will decrease in 2019. Exports are also projected to drop as more domestically produced material remains in the US market to meet the deficit arising from reduced Chinese supply. Agreed contractual volumes will continue to flow from China to the United States. In such circumstances, pMDI consumers will face rising prices where contracts allow. The impact a trade rebalance will have on the market is one factor amongst others contributing to upward price momentum anticipated in the second half of 2019. It is unlikely direct long-term supply shortages will be experienced due to the consequences of the tariff introduction. Instead major end users in the construction, appliance and wood composite industries will not have to moderate end use production, rather face higher polyurethane material costs.

Other polyurethane feedstocks are also impacted by the US-China trade war. The US implemented the 25% tariff on TDI and propylene oxide. On May 13, China applied retaliatory tariffs of 25% on pMDI, mMDI, and TDI as well as a 10% tariff on propylene oxide.

IHS Markit launched its new Global Polyurethane Feedstocks Market Advisory Service in March. This service helps clients navigate pricing, supply, and demand volatility in the polyurethane feedstocks markets. It also provides deep insight into the latest market developments, such as the impact of the US-China trade war on the polyurethane feedstocks markets.

https://ihsmarkit.com/research-analysis/impact-of-the-uschina-trade-war-on-the-mdi-market.html

August 26, 2019

Impact of the US-China trade war on the MDI market

The polymeric methyl diphenyl diisocyanate (pMDI) market has been impacted by the latestdevelopments in the United States-China trade war. pMDI, a key polyurethane feedstock, was initially included in the list of $200 billion of Chinese imports that were tariffed by the United States Trade Representative in response to China’s trade practices. US pMDI imports from China were subject to a 10% import tariff beginning September 24, 2018. This rate was subsequently increased to 25% on May 10.

The main polyurethane feedstocks – including pMDI, monomeric methyl diphenyl diisocyanate (mMDI), toluene diisocyanate (TDI), and polyether polyols (produced via the intermediate propylene oxide) – are reacted in different combinations to produce polyurethanes. The most common product is flexible and rigid polyurethane foam.

Polyurethanes are used in a myriad of applications. The buildings we live in, the mattresses we sleep on, and the shoes we wear can all contain polyurethanes. Even surfboards are made from rigid polyurethane foam. Polyurethanes are everywhere.

The global pMDI market has been volatile lately. In 2017, supply shortages triggered by plant outages and insufficient capacity investment led to a pMDI price surge. Prices collapsed in the second half of 2018, as supply significantly improved and demand waned amid product substitution and the cooling global economy. In late-Q1 2019, the pMDI market picked up with reinvigorated demand thanks to the peak spring construction season.

However, the escalation in the US-China trade war and implementation of the 25% trade tariff will impact global pMDI demand growth and in the United States. Slower global economic growth is now forecasted. One upshot is a weaker outlook in construction activity, including in the United States, moderating growth in building insulation demand; the largest pMDI end use in the United States is in rigid polyurethane and polyisocyanurate foam based insulation. In general, IHS Markit forecasts softer pMDI demand growth compared to the healthy growth exhibited in recent years. Weakness in other sectors such as the automotive industry – an industry facing its own challenges – is also projected to stifle US pMDI demand growth.

The United States, the second largest pMDI-consuming country, has seen its pMDI trade position shift in recent years. Historically, the US was a net exporter of pMDI. Today the country still exports a substantial volume of pMDI, including more than 200,000 metric tons (mt) in 2018.

The US pMDI market has recently exhibited high demand growth rates. Yet there has not been a major greenfield MDI capacity investment in the United States for many years. As the US import requirement grew and the pMDI market structurally tightened, the US became a net importer of pMDI in 2018.

Subsequently, the US market has become dependent on imports to meet demand. Approximately 71% of the 300,000 mt of pMDI imported into the US was sourced from China. Based on IHS Markit’s US pMDI monthly index and the monthly import volume, this equates to just under $500 million worth of imports.

The introduction of the 25% tariff will ensure that volatility continues in the pMDI market, especially in the US. US pMDI prices are forecast to rise not just because the tariff increase, but also because Chinese supply is expected to moderate as exporters reduce US shipments.

The United States trade position will rebalance. pMDI imports will decrease in 2019. Exports are also projected to drop as more domestically produced material remains in the US market to meet the deficit arising from reduced Chinese supply. Agreed contractual volumes will continue to flow from China to the United States. In such circumstances, pMDI consumers will face rising prices where contracts allow. The impact a trade rebalance will have on the market is one factor amongst others contributing to upward price momentum anticipated in the second half of 2019. It is unlikely direct long-term supply shortages will be experienced due to the consequences of the tariff introduction. Instead major end users in the construction, appliance and wood composite industries will not have to moderate end use production, rather face higher polyurethane material costs.

Other polyurethane feedstocks are also impacted by the US-China trade war. The US implemented the 25% tariff on TDI and propylene oxide. On May 13, China applied retaliatory tariffs of 25% on pMDI, mMDI, and TDI as well as a 10% tariff on propylene oxide.

IHS Markit launched its new Global Polyurethane Feedstocks Market Advisory Service in March. This service helps clients navigate pricing, supply, and demand volatility in the polyurethane feedstocks markets. It also provides deep insight into the latest market developments, such as the impact of the US-China trade war on the polyurethane feedstocks markets.

https://ihsmarkit.com/research-analysis/impact-of-the-uschina-trade-war-on-the-mdi-market.html

August 22, 2019

Polytek Development Corp. Announces Acquisition of

Stone Coat Countertops

August 22, 2019

Polytek Development Corp. Announces Acquisition of

Stone Coat Countertops

August 15, 2019

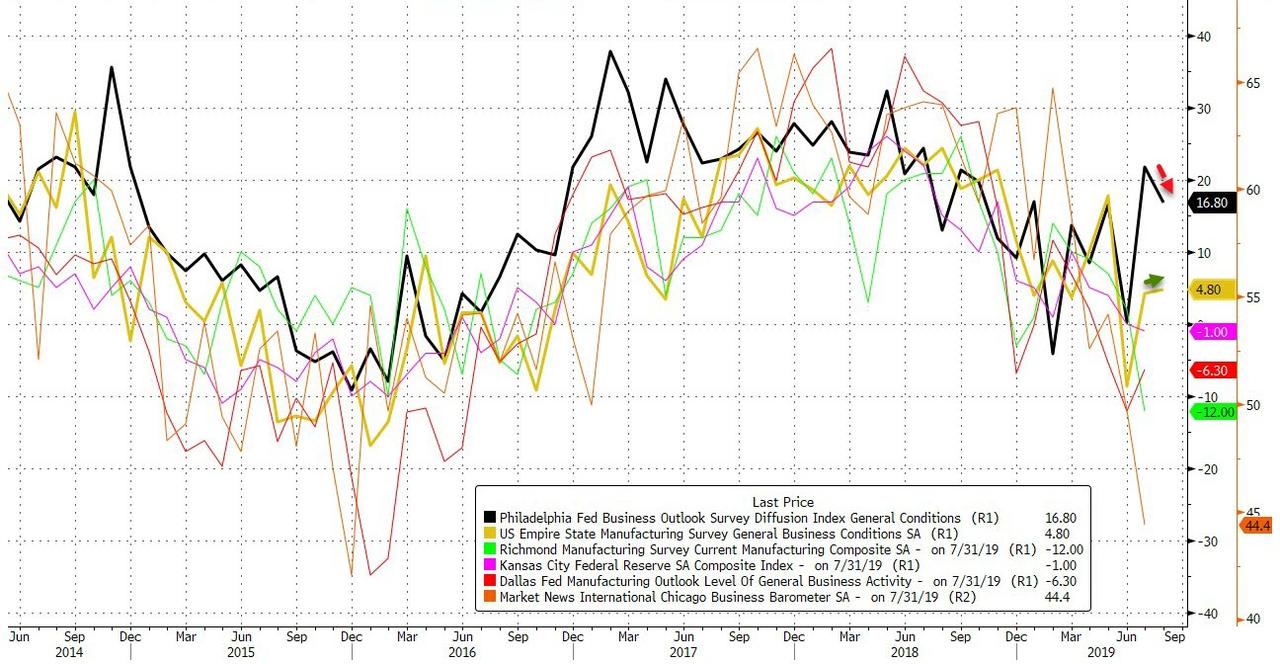

Philly, Empire Fed Beat Expectations, Confirming Economic Rebound

Following an unexpectedly strong retail sales report which saw a solid, 0.9% increase in sales ex autos and gas, almost double the 0.5% expected, we got further confirmation the US economy may be rebounding thanks to both the Philly and New York Fed, both of which printed well above expectations.

- Empire Manufacturing (NY) Fed August: 4.8. up from 4.3, and well above the 2.0% expected.

- Philadelphia Fed Business Outlook August: 16.8, down from 21.8 but also well above the 9.5% expected.

Commenting on the latest Philadelphia Fed, the survey organizers said that manufacturing activity in the region continued to grow, with “general activity, shipments, and employment indicators decreased from their readings last month, but the indicator for new orders increased.” The survey’s future activity indexes remained positive, suggesting continued optimism about growth for the next six months.

- The diffusion index for current general activity fell 5 points this month to 16.8, after increasing 22 points in July. Movements in the indexes for current shipments and new orders were mixed: The current new orders index increased 7 points, while the shipments index decreased 6 points. Both the unfilled orders and delivery times indexes remained positive this month, suggesting higher unfilled orders and slower delivery times.

- The firms continued to report increases in the prices paid for inputs. The percentage of firms reporting increases in input prices (25 percent) remained higher than the percentage reporting decreases (12 percent). The prices paid diffusion index decreased 3 points and remains well below readings over the past two and a half years. The current prices received index, reflecting the manufacturers’ own prices, increased 4 points to a reading of 13.0 but is also still well below readings of the past few years.

Meanwhile, the Empire Fed was even more optimistic, noting that “new orders increased after declining for the prior two months, and shipments continued to expand. Unfilled orders fell, delivery times were steady, and inventories increased.” On the other hand, the employment and average workweek indexes were both slightly below zero, pointing to sluggishness in labor market conditions. Input prices increased at a slightly slower pace than last month, and selling price increases were little changed. Some more details:

- Manufacturing firms in New York State reported that business activity grew modestly in August. The general business conditions index was little changed at 4.8, pointing to two months of modest growth after a brief decline in activity in June. Twenty-seven percent of respondents reported that conditions had improved over the month, while 22 percent reported that conditions had worsened. The new orders index climbed above zero, and at 6.7, indicated that orders increased. The shipments index moved slightly higher to 9.3, pointing to an increase in shipments. Unfilled orders declined for a third consecutive month. Delivery times were steady, and inventories rose for the first time since April.

- The index for number of employees held below zero for a third consecutive month, coming in at -1.6, and the average workweek index was -1.3, pointing to ongoing sluggishness in employment levels and hours worked. The prices paid index edged down two points to 23.2, suggesting a slightly slower pace of input price increases than last month. The prices received index was little changed at 4.5, with selling price increases maintaining a modest pace.

Where the news was less good was in the outlook, with indexes assessing the six-month outlook suggesting that firms were somewhat less optimistic about future conditions than they were last month. The index for future business conditions fell five points to 25.7, and the index for future new orders also moved lower.

The bottom line: the barrage of economic data today – from the beat in productivity and retail sales, to the stronger than expected Philly and Empire Fed indexes – suggest that the Fed may have a tough time pushing for a 50bps rate cut, or even a 25bps, absent a dramatic deterioration in financial conditions and/or further escalation in trade war.

Which probably explains why US futures are unable to decide what to do with today’s strong economic data, and if anything have drifted lower.

https://www.zerohedge.com/news/2019-08-15/philly-empire-fed-beat-expectations-confirming-economic-rebound