Company News

February 19, 2024

A Familiar Name in Urethanes Now New CEO of Olin

Olin taps LyondellBasell executive Lane as new President/CEO, succeeding Sutton

Feb. 19, 2024 8:14 PM ETOlin Corporation (OLN) StockLYBBy: Carl Surran, SA News Editor

Olin (NYSE:OLN) said Monday it named LyondellBaseel (LYB) executive Kenneth Lane as its new President and CEO effective March 18, when Scott Sutton will step down from those positions; no explanation was given for Sutton’s departure.

Lane was Executive VP of Global Olefins and Polyolefins at LyondellBasell (LYB), which he joined in 2019 after serving BASF for 13 years and holding executive positions across a wide range of businesses including Polyurethanes, Monomers and Catalysts; previously, he had spent time at BP Chemicals and Amoco Chemical.

Kim Foley will assume Lane’s previous role at LyondellBasell (LYB) after serving as Senior VP of Global Engineering, Turnarounds and Health, Safety and Environment.

February 8, 2024

Tempur Sealy Highlights from Investors Call

Tempur Sealy International, Inc. (TPX) Q4 2023 Earnings Call Transcript

Feb. 08, 2024 1:02 PM ETTempur Sealy International, Inc. (TPX) Stock

143.91K Followers

Q4: 2024-02-08 Earnings Summary

EPS of $0.53 misses by $0.01 | Revenue of $1.17B (-1.42% Y/Y) misses by $5.01M

Tempur Sealy International, Inc. (NYSE:TPX) Q4 2023 Earnings Conference Call February 8, 2024 8:00 AM ET

Company Participants

Aubrey Moore – Investor Relations

Scott Thompson – Chairman, President & Chief Executive Officer

Bhaskar Rao – Executive Vice President & Chief Financial Officer

Scott Thompson

Thank you, Aubrey. Good morning, everyone, and thank you for joining us on our 2023 fourth quarter and full year earnings call. I’ll begin with some highlights from the quarter and full year, and then turn the call over to Bhaskar to review our financial performance in more detail and discuss our 2024 guidance. After that, I’ll provide an update of our proposed acquisition of Mattress Firm, before opening up the call for Q&A.

In the fourth quarter of 2023, net sales were approximately $1.2 billion, and adjusted EPS was $0.53. Our results were in line with our expectation for the quarter, with sales and adjusted EPS approximately consistent with prior years.

Turning to a few highlights for 2023. First, I’d like to highlight our resilience of our business model, our robust cash flow and industry-leading balance sheet. Our solid financial position has given us flexibility to capitalize on the industry’s opportunities. We’re delivering strong operating cash flow, investing in the business and outperforming the broader bedding market in North America and internationally.

In the last three years, we’ve generated over $1.0 billion in cash flow after investing $1.3 billion in advertising and over $600 million in CapEx. We believe the strategic investments in our brands, capabilities and capacity enabled us and our retailers to succeed in a dynamic environment. Versus the prior year, adjusted EBITDA to net debt leverage declined from 3.1 to 2.87. We expect to continue to reduce our leverage in the coming quarters as we prepare for the closing of the proposed Mattress for transaction.

The US bedding industry, which is our largest market, was challenged in 2023. Based on preliminary figures, we believe the category units were down double-digits versus the prior year, and the US produced mattress units were below the 20-year trough for the industry. However, we have recently seen stabilization of the category demand. The international markets we operate in have generally demonstrated similar trends on a consolidated basis.

Over the prior two decades, the bedding industry has consistently grown through both ASP and unit expansion over time. We anticipate that the category will return to his historical trends of consistent growth. With our strong financial position, resilient operating model and the recent investments we’ve made in the business, Tempur Sealy is uniquely positioned to reap the benefits of an improving market.

The second item I’d like to highlight is our successful rollout of our new iconic premium products and continued expansion of extensive manufacturing capabilities. These actions in 2023, solidified our position as a leading vertically integrated global bedding company. Internationally, we successfully launched and all new lineup of timber mattresses, pillows and bed bases in over 90 markets, introducing new innovation and expanding our total addressable market globally. The consumer-centric innovation and expanded price points in the new collections for driving positive traction and broad range of customers, including our legacy ultra-premium consumers that mattress prices at 3,000 and above as well as consumer shopping for mattresses starting at 2000. The reaction to the new products has been positive. On the cost side, we have streamlined the construction of the new product to maximize manufacturing efficiencies, enhance our ability to efficiently customize products to meet customers’ needs in diverse markets and channels.

In the US, the new TEMPUR-breeze and Stearns & Foster product portfolio completed their rollout in 2023 and realized notable year-over-year growth. The TEMPUR-breeze portfolio achieved double-digit sales growth and a 5% increase in mattress and foundation ASP, while Stearns & Foster portfolio also delivered strong sales growth over the same period. These premium brands significantly outperformed the market and drove higher ASP for the entire category at a time when retailers are dealing with reduced floor traffic.

In 2024, we expect to complete the full refresh of our US Tempur portfolio by introducing our next generation of Adapt products. The new Adapt products are focused on meeting one of the highest consumer needs in mattresses, reduced aches and pains. This line includes our most advanced Tempur Material, uniquely designed to deliver 20% more pressure relief than the standard Tempur Material.

The Adapt products paired with our own proven line of innovative smart adjustable bases will build on the success of prior generations and Tempur Sealy’s robust R&D track record.

We have over 60,000 new Adapt mattresses ready as we prepare for the rollout to begin in the first quarter and expect to reach substantial completion before the Memorial Day holiday.

In 2023, we also opened our newest and largest state-of-the-art plant in Crawfordsville, Indiana. This new facility located in the Midwest, complements our existing manufacturing footprint, enhances our ability to serve Northeast customers.

Our expanded US manufacturing footprint will allow us to capture the projected long-term demand for our products and to support our rapidly growing OEM business. The new facility has the capabilities to manufacture a wide variety of bedding products and components for branded and non-branded operations.

Our third highlight is the diversification of our business model and go-to-market approach. One of our long-term initiatives is to increase the visibility with the consumer wherever and however they choose to shop. We follow the customers’ lead and aim to provide quality products at every price point, both on and offline.

In support of our broader portfolio diversification strategy, we are pursuing growth initiatives through innovation and development of industry-leading products. growing our wholesale business through existing and new retail relationships and increasing our investments in Stearns & Foster brand.

We’ll also look to expand further into the OEM market and grow our direct-to-consumer business through the expansion of our e-commerce channels and company-owned stores.

All these initiatives are in line with our pursuit of long-term sustainable growth. For example, our direct-to-consumer channel has increased from $150 million in 2015 to over $1.2 billion in 2023, a compound annual growth rate of 30%. This was in part thanks to the expansion into hundreds of new company-owned stores around the world and the successful launch of our Stearns & Foster and Sealy e-commerce websites. Additionally, we began offering OEM and private label products in 2020. And today, we generate hundreds of millions of dollars in profitable private label and OEM sales with further opportunities for growth in 2024 and beyond.

Lastly, our growth in wholesale has been broad-based across existing and new distribution. In fact, in April, we’ll be expanding our products into additional big-box stores with one of the largest U.S. bedding retailers.

Fourth, I’d like to highlight significant expansion in our year-over-year consolidated gross margin. We delivered year-over-year improvement of 260 basis points in our consolidated gross margin to 44.2%, in the fourth quarter of 2023. This is a result of efforts from the team to drive profitability by leveraging our fixed cost structure over multiple growth initiatives.

As mentioned, our new product innovation investments in manufacturing processes and plant and diversification of our go-to-market strategy have all contributed to improved gross margin. As we continue to drive greater efficiency, we increase our ability to invest in advertising, product development and our people. We also benefit from a larger pool of free cash flow to drive EPS growth and reduce our net leverage. While we expect the retail environment to remain dynamic, we have a track record of delivering results during challenging cycles.

In fact, we generated $4.9 billion in sales and $2.2 billion in gross profit for the full year 2023, both of which were just shy of our highest ever annual sales and gross profit figures. In 2024, we plan to stay focused on our long-term initiatives stay agile to capture opportunities and deliver higher sales and profits.

Our last highlight is on our commitment to protect and improve our communities and the environment, as we detailed in our recently published 2024 corporate social values report. The report is available on our IR website. We are proud of our achievements over the last year, including our zero waste to landfill status at our Canadian and Mexican manufacturing facilities and maintaining our zero waste landfill status at our U.S. and European manufacturing operations. This year, we contributed over $800,000 in shared contributions through our Tempur Sealy Foundation and donated more than 12,100 mattresses worth approximately $16.9 million, bringing our cumulative 10-year donation total to over $100 million.

Scott Thompson

Thank you, Bhaskar. Nice job. Before opening up the call for questions, let me provide a brief update on our pending acquisition of Mattress Firm. In the fourth quarter, we certified substantial completion with the FTC second request. We continue to work with the FTC to advance the transaction approval process. We anticipate these conversations will continue through the first quarter. As previously, disclosed we continue to expect the transaction to close in mid to late 2024. In connection with and contingent upon the acquisition, we are proactively pursuing a divestiture plan and engaging with Mattress Firm suppliers. In parallel, Tempur Sealy and Mattress Firm continue to make joint progress on integration planning.

Lastly, a brief comment on Mattress Firm’s financial performance. Mattress Firm recently made their quarterly results available on their website, which were consistent with our expectations. We encourage you to review Mattress Firm’s website for more information on their financial performance for the most recent quarter. In summary, our progress towards the transaction close is on track and we look forward to joining with the Mattress Firm team.

Susan Maklari

Good morning, Scott. Maybe to start with why don’t we talk a little bit about demand? You mentioned that it seems like we have bottomed out in the fourth quarter and that this year we could see a sequential improvement as we move through. How are you thinking about that, I guess relative to the macro backdrop the potential for rates to come down? And what else do you think is stimulating the consumer a bit perhaps to start to see some improvement on the unit side?

Scott Thompson

Well, obviously we have easier comps, which is probably the first thing that’s got to be pointed out. Second thing obviously, we are at an all-time low when we’re talking about the US in volume. So we are really at rock bottom from a historical standpoint. And as you mentioned, there are some green shoots. Obviously, we’re in an environment where interest rates are trending down. We’re also — if you look at the bedding industry and we just got back from the Vegas bedding show there’s good innovation in the industry. We’ve got some new product coming out and others have some new product coming out that’s very interesting.

We’ve also seen some of our larger retailers, I’m going to say, refocus on advertising and we’ve got several of them increasing their advertising budgets going into 2024. So, yeah, in general it feels like I’ve used the term balancing around the bottom. We’re kind of bouncing around the bottom. If you go back and look at the fourth quarter and kind of look at it parse it by month, October was not good in the US and then it got better throughout the quarter.

And then you get to the January period. And obviously, it’s very difficult in this world to forecast. If we look at our own order book in January, it’s positive. If I look at our online sales in January it’s up double digits. So it looks like some green shoots, but you have to dampen that when you look at some of the details, the order book is positive, but it’s concentrated in some larger customers. It’s not as broad-based as we’d like to see. If you go talk to the retailers and listen to them, floor traffic is down double digits. And their January — when you talk to the retailers in general are talking about being down 10%. And then you think about January it’s only 30% of the quarter. So what I’m kind of saying, it’s all mixed and we are continuing to get some mixed signals, but clearly bouncing around the bottom seems to be the best description currently.

Keith Hughes

Thank you. A question on the new facility in Indiana. Once you get up to full capacity, how much of your pouring will that represent? And will you actually hit full capacity in the second quarter?

Scott Thompson

Really complicated question. Let me put some words around it. No, we will not hit full capacity in the second quarter. And it depends on when you talk about capacity, whether you’re running one shift, two shifts all that kind of stuff. The way you should probably think about it is look first quarter a little bit of a drag to get it going by the time you’re into the second and third quarter, Crawfordsville is contributing, okay?

But you should think about optimize — optimized it’s probably a couple of years out as far as being totally optimized depending on what the bedding market is and it gives us great flexibility. But we’ve — with Crawfordsville and the other plants we have and the ability to go to second shifts, you should think about Tempur has capacity for the foreseeable future, both in pouring OEM foam and regular foam.

Keith Hughes

Okay. One follow-up question to that.

Scott Thompson

Go ahead.

Keith Hughes

Do you think you’re going to — in terms of like spring production, do you think you’ll do some more backward integration on spring production in the future as well? Particularly, given the volume you’re starting to move in the industry?

Scott Thompson

Yes. I don’t know. That’s something we’ve always looked at. We’ve got a great partnership with Leggett for sure. They do a fabulous job for us. We’ve got some other manufacturers that are doing good job for us. And we make a good bit of our springs already. We make our own springs in the Asian market.

William Reuter

Hi. Just kind of follows on that last question. But you mentioned you expect ASP to be flat. Are you seeing a trade down currently? Are you currently seeing ASP flat? Or are you seeing greater strength at lower price points? I know you have Stearns & Foster rollout last year so that may be contributing to some greater success there. But any comments on mix?

Scott Thompson

Yeah. On mix, we’re generally seeing the higher priced units do better than the lower-priced units. That’s a trend that has been around for a year or so. I would say the gap has narrowed some, but we continue to see that mix. We haven’t seen any deterioration in the strength of the higher end. And I think in general, what I think Bhaskar’s talked about correct me if I’m wrong, on a like-for-like basis we aren’t expecting to see ASP increases as there’s quite a bit of pricing put in the market over the last few years due to commodity increases. And it feels like the commodity thing is behind us and price on a like-for-like basis is stabilized.

Read more here:

February 6, 2024

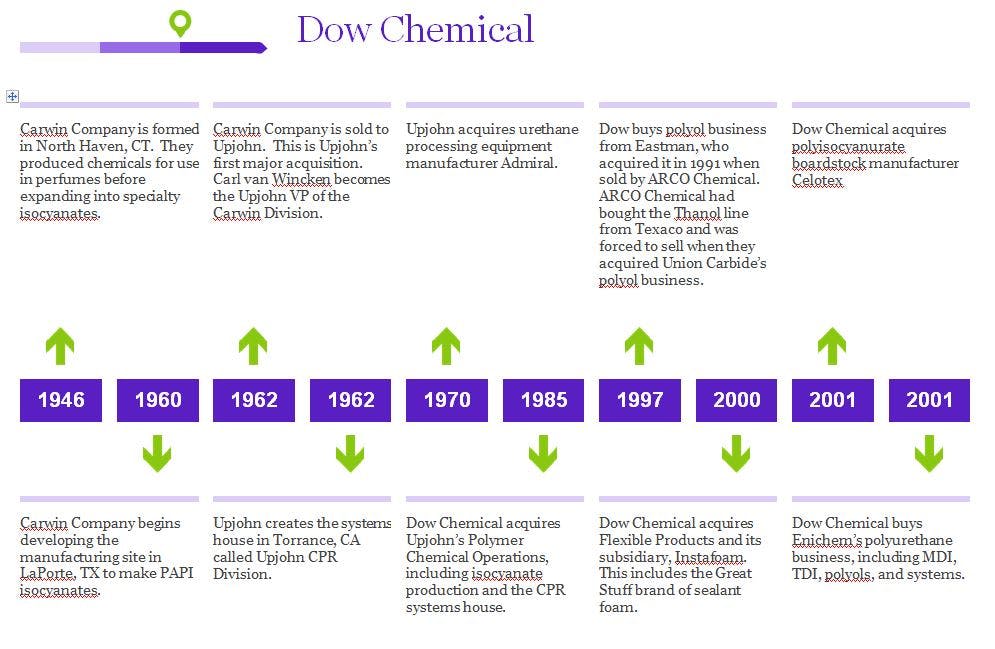

Dow Chemical Urethane History Part I

February 6, 2024

Another Mattress Facility in the U.S.

Kuka Sleep Celebrates Opening of Factory in Dallas

Kuka Sleep, a division of Hangzhou, China-based Kuka Home, has opened a mattress manufacturing facility in Dallas — a milestone for the company as it embarks on a new chapter of handcrafting custom sleep solutions in the United States, according to a news release.

Spanning 504,500 square feet, the new factory is located at 3584 Mountain Creek Parkway.

Read more here: https://bedtimesmagazine.com/2024/01/kuka-sleep-opens-factory-in-dallas-texas/

February 6, 2024

Wanhua 2023 Results

Wanhua Chemical Group Co., Ltd. Reports Earnings Results for the Full Year Ended December 31, 2023

February 02, 2024 at 04:51 pm IST

Wanhua Chemical Group Co., Ltd. reported earnings results for the full year ended December 31, 2023. For the full year, the company reported sales was CNY 17.54 million compared to CNY 16.56 million a year ago. Net income was CNY 1.68 million compared to CNY 1.62 million a year ago.

Basic earnings per share from continuing operations was CNY 5.36 compared to CNY 5.17 a year ago.