Epoxy

August 4, 2022

Chinese Epoxy Update

Epoxy in August Cautiously Optimistic

ECHEMI 2022-08-01

In July, the liquid epoxy resin went down all the way. The highest average price in the month was 22,000 yuan/ton, and the lowest average price was 17,800 yuan/ton, a drop of 19.09%; from January to July, the highest average price during the period was 29,300 yuan/ton, and the lowest average price was 29,300 yuan/ton. The price was 17,800 yuan/ton, a drop of 39.25%.

As of the weekend (7.29), the market price of liquid epoxy resin continued to fluctuate within a week, with limited news changes. This was mainly due to limited price fluctuations at the cost side of resins, few offers from resin manufacturers to discuss one by one, and a small amount of downstream just needed replenishment. Most of the merchants focus on stable prices, and the trading atmosphere in the market is sluggish, and it is difficult to increase the volume of real orders.

Market outlook forecast: It is expected that the epoxy resin market price will remain weak and fluctuated in the short term, and pay close attention to the trend of upstream dual raw materials and changes in downstream wind power and electronics demand.

Wind power is the ballast stone of the epoxy market, and wind power is expensive. This year, the state’s requirement for wind power installed capacity is to exceed 55GW. However, in the first half of the year, the actual installation volume was only 14.5GW, which was more than half of the time, and the installation progress did not exceed half of the time. Therefore, after August, it will gradually enter the peak installation period, and the demand for resin for blades should increase.

The 40.5GW wind power blades to be installed in the second half of the year will theoretically consume 172,200 tons of liquid epoxy, which will be allocated to 5 months, and 34,400 tons per month. However, judging from the current situation, wind power companies have not yet accelerated their actions, and the curing agent/diluent supporting the blades has no signs of recovery. Therefore, the pulling effect of wind power in August may be limited, and it is hoped that the wind power will be installed in September and October set off a climax.

Electronic appliances are estimated to be out of play. Last year, due to the global epidemic, online classes and home office overdrafts consumed a huge amount of electronic products such as tablet computers, TVs, etc., which greatly stimulated the demand for epoxy resins for electronic products. Although consumer electronics are updated quickly, they also have a certain life cycle. The market capacity that was saturated last year cannot be replicated this year. Due to the decline of the market, the demand for electronic resins has also declined this year. We can only see if the traditional gold, nine silver and ten consumption seasons can bring some hope.

On July 28, a meeting of the Political Bureau of the Central Committee was held, which is second only to the Central Economic Work Conference. In the middle of the year, it connects the previous and the next, analyzes and studies the current economic situation, and deploys the economic work in the second half of the year.

At present, the internal and external environment is more complex and severe. The epidemic and economic recovery have reached a critical point. The economy and capital market have also reached a new crossroads.

Regarding the economic growth target, the meeting pointed out that “the economy must be stabilized”, “maintain the economic operation within a reasonable range, and strive to achieve the best results”, “the major economic provinces must bravely take the lead, and the qualified provinces must strive to achieve the expected economic and social development goals. “.

This is a relatively new statement. The current international and domestic environment is complex, and the global economy is facing high uncertainty. The International Monetary Fund has just lowered its growth forecast for major global economies again.

In the second quarter of the country, major cities were affected by the epidemic. In the first half of the year, GDP achieved 2.5%. It will be very difficult to achieve the annual target of 5.5% at the beginning of the year.

The draft did not mention the specific numerical target of 5.5, which means that the annual growth target of around 5.5% is not a rigid requirement, but the meeting called for ensuring that the economy operates within a reasonable range.

With flood irrigation, the requirement of 5.5 can be fulfilled under a substantial stimulus, but on July 19, the Prime Minister just said that macroeconomic policies should be drip irrigation accurately, and that super-large-scale stimulus measures, excess currency issuance, and future advances will not be introduced in order to achieve excessive growth goals.

It is also a good thing not to mention the rigid requirements of numbers, which means that the upper levels are more objective and realistic, no longer simply pursuing numbers, and appropriately lowering expectations, which is conducive to the adjustment of my country’s economic structure and the healthy and stable development of the medium and long-term economy.

After reading the draft, it is not advisable to be overly optimistic about the economy, stock market and property market in the second half of the year. Under the condition of ensuring price stability in the second half of the year and the completion of the employment target, in the end, the economic growth rate will be slower, as long as it is acceptable within a reasonable range.

Therefore, under the premise that the national economic growth rate is slowing down, our hopes for epoxy resin in August should not be too optimistic.

August 4, 2022

Epoxy Comments from Westlake Q2 Discussion

WESTLAKE CORP Management’s Discussion and Analysis of Financial Condition and Results of Operations (form 10-Q)

08/03/2022 | 02:37pm EDT

Overview

We are a vertically integrated global manufacturer and marketer of performance

and essential materials and housing and infrastructure products. We operate in

two principal operating segments, Performance and Essential Materials and

Housing and Infrastructure Products. The Performance and Essential Materials

segment includes Westlake North American Vinyls, Westlake North American

Chlor-alkali & Derivatives, Westlake European & Asian Chlorovinyls, Westlake

Olefins, Westlake Polyethylene and Westlake Epoxy. The Housing and

Infrastructure Products segment includes Westlake Royal Building Products,

Westlake Pipe & Fittings, Westlake Global Compounds and Westlake Dimex. Prior to

our segment reorganization in the fourth quarter of 2021, we operated in two

principal operating segments, Vinyls and Olefins. The change has been

retrospectively reflected in the periods presented in this Form 10-Q. We are

highly integrated along our materials chain with significant downstream

integration from ethylene and chlor-alkali (chlorine and caustic soda) into

vinyls, polyethylene, epoxy and styrene monomer. We also have substantial

downstream integration from polyvinyl chloride ("PVC") into our building

products, PVC pipes and fittings and PVC compounds in our Housing and

Infrastructure Products segment.

Performance and Essentials Materials

Ethane-based ethylene producers have experienced a cost advantage over

naphtha-based ethylene producers during periods of higher crude oil prices. This

cost advantage has resulted in a strong export market for polyethylene and other

ethylene derivatives and has benefited operating margins and cash flows for our

Performance and Essential Materials segment during such periods. In the past

year, we have seen significant volatility in natural gas, ethane and ethylene

prices, primarily due to changes in demand, the timing for certain new ethylene

capacity additions, the availability of natural gas liquids, and the ongoing

conflict between Russia and Ukraine.

Our performance and essential materials such as ethylene, PVC, polyethylene,

epoxy and chlor-alkali are some of the most widely used materials in the world

and are upgraded into a variety of higher value-added products used in many

end-markets. Our performance and essential materials are used by customers in

food and specialty packaging; industrial and consumer packaging; medical health

applications; PVC pipe applications; consumer durables; mobility and

transportation; renewable wind energy; and housing and construction products.

Chlor-alkali and petrochemicals are typically manufactured in large volume by a

number of different producers using widely available technologies. The

chlor-alkali and petrochemical industries exhibit cyclical commodity

characteristics, and margins are influenced by changes in the balance between

supply and demand and the resulting operating rates, the level of general

economic activity and the price of raw materials. Due to the significant size of

new plants, capacity additions are built in large increments and typically

require several years of demand growth to be absorbed. The cycle is generally

characterized by periods of tight supply, leading to high operating rates and

margins, followed by a decline in operating rates and margins primarily as a

result of excess new capacity additions.

Westlake is the second-largest chlor-alkali producer and the second-largest PVC

producer in the world, which makes Westlake a global leading chlorovinyls

producer. Demand for our products in the first half of 2020 was negatively

impacted by the onset of the COVID-19 pandemic. Global demand for most of our

products started strengthening in the second half of 2020 and has remained

strong through the second quarter of 2022. We expect global demand for most of

our products to remain favorable throughout 2022.

25

——————————————————————————–

Table of Contents

On February 1, 2022, we completed the acquisition of Westlake Epoxy for a purchase consideration of $1,207 million. The assets acquired and liabilities assumed and the results of operations of the Westlake Epoxy business are included in the Performance and Essential Materials segment. This acquisition represents a significant strategic expansion of Westlake's Performance and Essential Materials businesses into additional high-growth, innovative and sustainability-oriented applications - such as wind turbine blades and light-weight automotive structural components. Because epoxies are produced from chlorine and caustic soda, the transaction also provides vertical integration with Westlake's global chlor-alkali businesses. With the acquisition of the Westlake Epoxy business Westlake is now one of the leading producers of epoxy specialty resins, modifiers and curing agents in Europe and the United States with a global reach to our end markets. Epoxy resins are the fundamental component of many types of materials and are often used in the automotive, construction, wind energy, aerospace and electronics industries due to their superior adhesion, strength and durability. Our position in basic epoxy resins, along with our technology and service expertise, has enabled us to offer formulated specialty products in certain markets. In composites, our specialty epoxy products are used either as replacements for traditional materials such as metal, wood and ceramics, or in applications where traditional materials do not meet demanding engineering specifications. We are also one of the leading producers of resins that are used in fiber reinforced composites. Composites are a fast growing class of materials that are used in a wide variety of applications ranging from aircraft components and wind turbine blades to sports equipment, and increasingly in automotive and transportation. We supply epoxy resin systems to composite fabricators in the wind energy, automotive and pipe markets. Epoxy specialty resins are also used for a variety of high-end coating applications that require the superior adhesion, corrosion resistance and durability of epoxy, such as protective coatings for industrial flooring, pipe, marine and construction applications and automotive coatings. Epoxy-based surface coatings are among the most widely-used industrial coatings due to their long service life and broad application functionality combined with overall economic efficiency. We also leverage our resin and additives position to supply custom resins to specialty coatings formulators. The raw materials that we primarily use to manufacture our epoxy products are chlorine and caustic soda, among others and are available from more than one source including internal sourcing and the open market. Prices for our main feedstocks are generally driven by the underlying petrochemical benchmark prices and energy costs, which are subject to price fluctuations. Depending on the performance of the global economy, the timing of resolution of the conflict between Russia and Ukraine, disruption in the global supply chain, labor shortages and costs, potential resurgence of the COVID-19 pandemic, the trend of crude oil prices, new capacity additions in North America, Asia and the Middle East in 2022 and beyond, the sustainability of the current, strong demand for most of our products, inflationary pressures and concerns over slower future economic growth, including the possibility of recession or financial market instability, our financial condition, results of operations or cash flows could be negatively or positively impacted. We purchase significant amounts of ethane feedstock, natural gas, ethylene and salt from external suppliers for use in production of performance and essential materials. We also purchase significant amounts of electricity to supply the energy required in our production processes. While we have agreements providing for the supply of ethane feedstock, natural gas, ethylene, salt and electricity, the contractual prices for these raw materials and energy vary with market conditions and may be highly volatile. Factors that have caused volatility in our raw material prices in the past, and which may do so in the future include:

•the availability of feedstock from shale gas and oil drilling;

•supply and demand for crude oil and natural gas;

•shortages of raw materials due to increasing demand;

•ethane and liquefied natural gas exports;

•capacity constraints due to higher construction costs for investments, construction delays, strike action or involuntary shutdowns;

•the general level of business and economic activity; and

•the direct or indirect effect of governmental regulation.

Significant volatility in raw material costs tends to put pressure on product

margins as sales price increases could lag behind raw material cost increases.

Conversely, when raw material costs decrease, customers may seek immediate

relief in the form of lower sales prices. We currently use derivative

instruments to reduce price volatility risk on feedstock commodities and lower

overall costs. Normally, there is a pricing relationship between a commodity

that we process and the feedstock from which it is derived. When this pricing

relationship deviates from historical norms, we have from time to time entered

into derivative instruments and physical positions in an attempt to take

advantage of this relationship.

Acquisition of Hexion Epoxy Business

On November 24, 2021, the Company, through a wholly-owned subsidiary, entered

into a Stock Purchase Agreement (the "Hexion Epoxy Purchase Agreement") by and

among Hexion Inc. ("Hexion"), a New Jersey corporation, and solely for the

limited purposes set forth therein, the Company. Pursuant to the terms of the

Hexion Epoxy Purchase Agreement, the Company agreed to acquire all of the equity

interests in Hexion's global epoxy business ("Westlake Epoxy"). On February 1,

2022, the Company completed the acquisition of, and acquired all of the equity

interests in, the Westlake Epoxy business for a purchase consideration of $1,207

million. The assets acquired and liabilities assumed and the results of

operations of the Westlake Epoxy business are included in the Performance and

Essential Materials segment.

Performance and Essential Materials Segment

Net Sales. Net sales for the Performance and Essential Materials segment

increased by $958 million, or 45%, to $3,104 million in the second quarter of

2022 from $2,146 million in the second quarter of 2021. Average sales prices for

the Performance and Essential Materials segment increased by 27% in the second

quarter of 2022 as compared to the second quarter of 2021. The higher

Performance Materials sales prices were due to higher PVC resin sales prices.

The higher Essential Materials sales prices were primarily driven by the higher

prices for caustic soda, chlorine, styrene and derivative products. Sales

volumes for the Performance and Essential Materials segment increased by 18% in

the second quarter of 2022 as compared to the second quarter of 2021, primarily

resulting from the acquisition of Westlake Epoxy in the first quarter of 2022.

Income from Operations. Income from operations for the Performance and Essential

Materials segment increased by $294 million to $965 million in the second

quarter of 2022 from $671 million in the second quarter of 2021. This increase

in income from operations was due to higher sales prices for PVC resin, caustic

soda and styrene and higher margins for polyethylene, mainly resulting from

strong demand for our products. Income from operations was also higher due to

the acquisition of Westlake Epoxy in the first quarter of 2022. The increase in

income from operations versus the prior-year period was partially offset by

higher global fuel and power costs, higher feedstock costs and lower sales

volumes for PVC resin.

https://www.marketscreener.com/quote/stock/WESTLAKE-CORPORATION-14877/news/WESTLAKE-CORP-Management-s-Discussion-and-Analysis-of-Financial-Condition-and-Results-of-Operations-41186706/

August 4, 2022

Epoxy Comments from Westlake Q2 Discussion

WESTLAKE CORP Management’s Discussion and Analysis of Financial Condition and Results of Operations (form 10-Q)

08/03/2022 | 02:37pm EDT

Overview

We are a vertically integrated global manufacturer and marketer of performance

and essential materials and housing and infrastructure products. We operate in

two principal operating segments, Performance and Essential Materials and

Housing and Infrastructure Products. The Performance and Essential Materials

segment includes Westlake North American Vinyls, Westlake North American

Chlor-alkali & Derivatives, Westlake European & Asian Chlorovinyls, Westlake

Olefins, Westlake Polyethylene and Westlake Epoxy. The Housing and

Infrastructure Products segment includes Westlake Royal Building Products,

Westlake Pipe & Fittings, Westlake Global Compounds and Westlake Dimex. Prior to

our segment reorganization in the fourth quarter of 2021, we operated in two

principal operating segments, Vinyls and Olefins. The change has been

retrospectively reflected in the periods presented in this Form 10-Q. We are

highly integrated along our materials chain with significant downstream

integration from ethylene and chlor-alkali (chlorine and caustic soda) into

vinyls, polyethylene, epoxy and styrene monomer. We also have substantial

downstream integration from polyvinyl chloride ("PVC") into our building

products, PVC pipes and fittings and PVC compounds in our Housing and

Infrastructure Products segment.

Performance and Essentials Materials

Ethane-based ethylene producers have experienced a cost advantage over

naphtha-based ethylene producers during periods of higher crude oil prices. This

cost advantage has resulted in a strong export market for polyethylene and other

ethylene derivatives and has benefited operating margins and cash flows for our

Performance and Essential Materials segment during such periods. In the past

year, we have seen significant volatility in natural gas, ethane and ethylene

prices, primarily due to changes in demand, the timing for certain new ethylene

capacity additions, the availability of natural gas liquids, and the ongoing

conflict between Russia and Ukraine.

Our performance and essential materials such as ethylene, PVC, polyethylene,

epoxy and chlor-alkali are some of the most widely used materials in the world

and are upgraded into a variety of higher value-added products used in many

end-markets. Our performance and essential materials are used by customers in

food and specialty packaging; industrial and consumer packaging; medical health

applications; PVC pipe applications; consumer durables; mobility and

transportation; renewable wind energy; and housing and construction products.

Chlor-alkali and petrochemicals are typically manufactured in large volume by a

number of different producers using widely available technologies. The

chlor-alkali and petrochemical industries exhibit cyclical commodity

characteristics, and margins are influenced by changes in the balance between

supply and demand and the resulting operating rates, the level of general

economic activity and the price of raw materials. Due to the significant size of

new plants, capacity additions are built in large increments and typically

require several years of demand growth to be absorbed. The cycle is generally

characterized by periods of tight supply, leading to high operating rates and

margins, followed by a decline in operating rates and margins primarily as a

result of excess new capacity additions.

Westlake is the second-largest chlor-alkali producer and the second-largest PVC

producer in the world, which makes Westlake a global leading chlorovinyls

producer. Demand for our products in the first half of 2020 was negatively

impacted by the onset of the COVID-19 pandemic. Global demand for most of our

products started strengthening in the second half of 2020 and has remained

strong through the second quarter of 2022. We expect global demand for most of

our products to remain favorable throughout 2022.

25

——————————————————————————–

Table of Contents

On February 1, 2022, we completed the acquisition of Westlake Epoxy for a purchase consideration of $1,207 million. The assets acquired and liabilities assumed and the results of operations of the Westlake Epoxy business are included in the Performance and Essential Materials segment. This acquisition represents a significant strategic expansion of Westlake's Performance and Essential Materials businesses into additional high-growth, innovative and sustainability-oriented applications - such as wind turbine blades and light-weight automotive structural components. Because epoxies are produced from chlorine and caustic soda, the transaction also provides vertical integration with Westlake's global chlor-alkali businesses. With the acquisition of the Westlake Epoxy business Westlake is now one of the leading producers of epoxy specialty resins, modifiers and curing agents in Europe and the United States with a global reach to our end markets. Epoxy resins are the fundamental component of many types of materials and are often used in the automotive, construction, wind energy, aerospace and electronics industries due to their superior adhesion, strength and durability. Our position in basic epoxy resins, along with our technology and service expertise, has enabled us to offer formulated specialty products in certain markets. In composites, our specialty epoxy products are used either as replacements for traditional materials such as metal, wood and ceramics, or in applications where traditional materials do not meet demanding engineering specifications. We are also one of the leading producers of resins that are used in fiber reinforced composites. Composites are a fast growing class of materials that are used in a wide variety of applications ranging from aircraft components and wind turbine blades to sports equipment, and increasingly in automotive and transportation. We supply epoxy resin systems to composite fabricators in the wind energy, automotive and pipe markets. Epoxy specialty resins are also used for a variety of high-end coating applications that require the superior adhesion, corrosion resistance and durability of epoxy, such as protective coatings for industrial flooring, pipe, marine and construction applications and automotive coatings. Epoxy-based surface coatings are among the most widely-used industrial coatings due to their long service life and broad application functionality combined with overall economic efficiency. We also leverage our resin and additives position to supply custom resins to specialty coatings formulators. The raw materials that we primarily use to manufacture our epoxy products are chlorine and caustic soda, among others and are available from more than one source including internal sourcing and the open market. Prices for our main feedstocks are generally driven by the underlying petrochemical benchmark prices and energy costs, which are subject to price fluctuations. Depending on the performance of the global economy, the timing of resolution of the conflict between Russia and Ukraine, disruption in the global supply chain, labor shortages and costs, potential resurgence of the COVID-19 pandemic, the trend of crude oil prices, new capacity additions in North America, Asia and the Middle East in 2022 and beyond, the sustainability of the current, strong demand for most of our products, inflationary pressures and concerns over slower future economic growth, including the possibility of recession or financial market instability, our financial condition, results of operations or cash flows could be negatively or positively impacted. We purchase significant amounts of ethane feedstock, natural gas, ethylene and salt from external suppliers for use in production of performance and essential materials. We also purchase significant amounts of electricity to supply the energy required in our production processes. While we have agreements providing for the supply of ethane feedstock, natural gas, ethylene, salt and electricity, the contractual prices for these raw materials and energy vary with market conditions and may be highly volatile. Factors that have caused volatility in our raw material prices in the past, and which may do so in the future include:

•the availability of feedstock from shale gas and oil drilling;

•supply and demand for crude oil and natural gas;

•shortages of raw materials due to increasing demand;

•ethane and liquefied natural gas exports;

•capacity constraints due to higher construction costs for investments, construction delays, strike action or involuntary shutdowns;

•the general level of business and economic activity; and

•the direct or indirect effect of governmental regulation.

Significant volatility in raw material costs tends to put pressure on product

margins as sales price increases could lag behind raw material cost increases.

Conversely, when raw material costs decrease, customers may seek immediate

relief in the form of lower sales prices. We currently use derivative

instruments to reduce price volatility risk on feedstock commodities and lower

overall costs. Normally, there is a pricing relationship between a commodity

that we process and the feedstock from which it is derived. When this pricing

relationship deviates from historical norms, we have from time to time entered

into derivative instruments and physical positions in an attempt to take

advantage of this relationship.

Acquisition of Hexion Epoxy Business

On November 24, 2021, the Company, through a wholly-owned subsidiary, entered

into a Stock Purchase Agreement (the "Hexion Epoxy Purchase Agreement") by and

among Hexion Inc. ("Hexion"), a New Jersey corporation, and solely for the

limited purposes set forth therein, the Company. Pursuant to the terms of the

Hexion Epoxy Purchase Agreement, the Company agreed to acquire all of the equity

interests in Hexion's global epoxy business ("Westlake Epoxy"). On February 1,

2022, the Company completed the acquisition of, and acquired all of the equity

interests in, the Westlake Epoxy business for a purchase consideration of $1,207

million. The assets acquired and liabilities assumed and the results of

operations of the Westlake Epoxy business are included in the Performance and

Essential Materials segment.

Performance and Essential Materials Segment

Net Sales. Net sales for the Performance and Essential Materials segment

increased by $958 million, or 45%, to $3,104 million in the second quarter of

2022 from $2,146 million in the second quarter of 2021. Average sales prices for

the Performance and Essential Materials segment increased by 27% in the second

quarter of 2022 as compared to the second quarter of 2021. The higher

Performance Materials sales prices were due to higher PVC resin sales prices.

The higher Essential Materials sales prices were primarily driven by the higher

prices for caustic soda, chlorine, styrene and derivative products. Sales

volumes for the Performance and Essential Materials segment increased by 18% in

the second quarter of 2022 as compared to the second quarter of 2021, primarily

resulting from the acquisition of Westlake Epoxy in the first quarter of 2022.

Income from Operations. Income from operations for the Performance and Essential

Materials segment increased by $294 million to $965 million in the second

quarter of 2022 from $671 million in the second quarter of 2021. This increase

in income from operations was due to higher sales prices for PVC resin, caustic

soda and styrene and higher margins for polyethylene, mainly resulting from

strong demand for our products. Income from operations was also higher due to

the acquisition of Westlake Epoxy in the first quarter of 2022. The increase in

income from operations versus the prior-year period was partially offset by

higher global fuel and power costs, higher feedstock costs and lower sales

volumes for PVC resin.

https://www.marketscreener.com/quote/stock/WESTLAKE-CORPORATION-14877/news/WESTLAKE-CORP-Management-s-Discussion-and-Analysis-of-Financial-Condition-and-Results-of-Operations-41186706/

August 2, 2022

Contract Truck Rates Expected to Fall

Contract truckload rates will likely soften in the coming months

Spot rates indicate a strong dip for contracts is imminent

Zach Strickland, FW Market Expert & Market Analyst Follow on Twitter Saturday, July 30, 2022 3 minutes read Listen to this article 0:00 / 4:56 BeyondWords

Van rates on the truckload contract market will likely soften in the coming months. But, the decline won’t be as marked as what the industry saw on the spot market side.

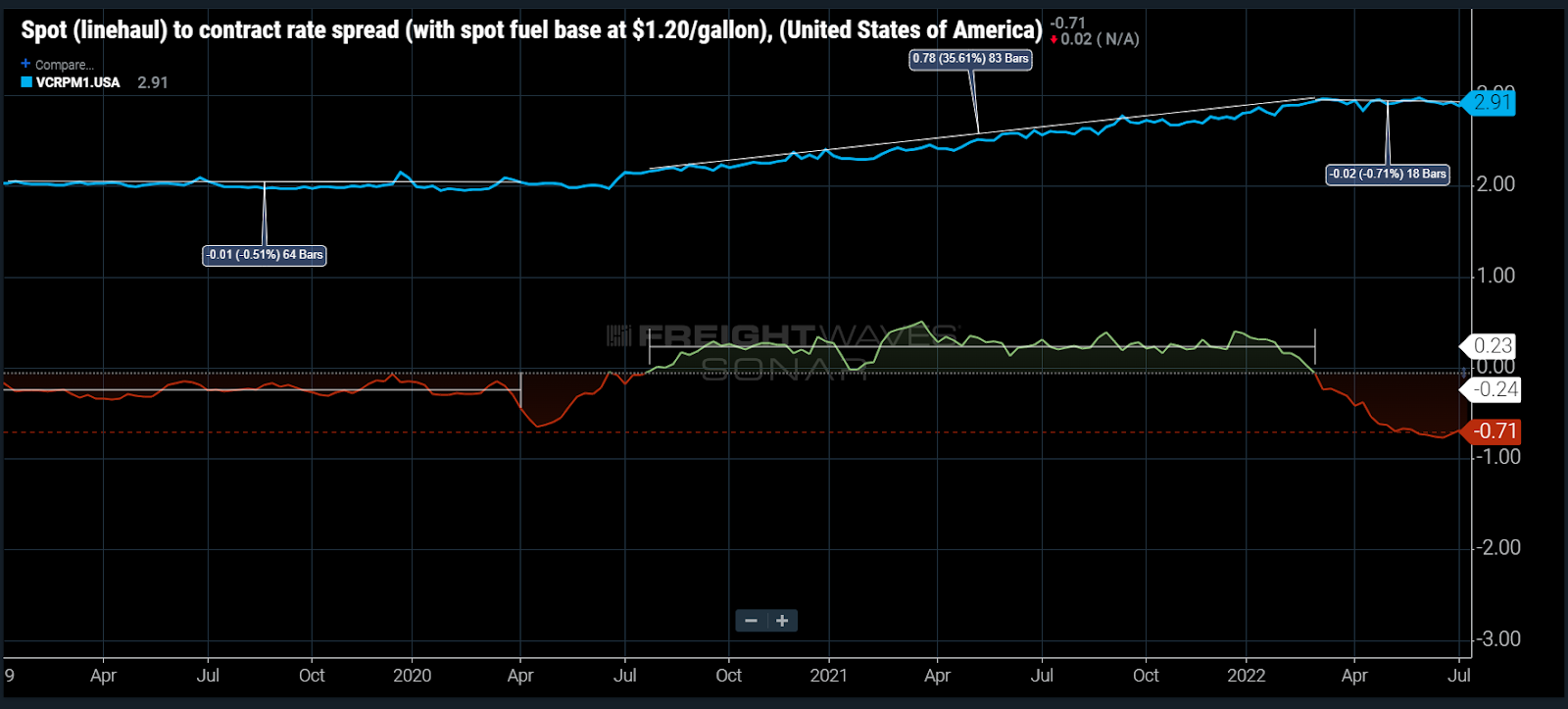

The spread between spot and contract rates has averaged around record low levels (~-74 cents a mile) since early May. That will put downward pressure on contract rates for bids negotiated in the second half of the year. There is little precedent for such a dramatic difference, but there’s also little evidence historically that contract rates will fall as fast as they increase.

The contract truckload market behaves very differently from the spot market. Volatility is the main difference. That’s driven primarily by the way pricing is negotiated.

The RATES12 index used in this week’s chart is the difference between spot rates less a level of estimated cost of fuel and contract rates. This is done for a more apples-to-apples comparison of the two rates, as contract rates include a portion of fuel cost and pass a lot of it along in the form of a fuel surcharge. This mechanism is largely absent from spot rates.

Contract truckload rates have barely budged since March, but red flags are already appearing

The contract or published rate market is simply an agreement between shipper and carrier that is in place for an extended period of time. The commitment is somewhat tenuous as neither volume nor service is guaranteed in most instances.

The only binding portion is, if the shipper tenders a load(s) to the carrier and the carrier is willing and able to transport the customer’s freight, it will do it for a predetermined price until the expiration of the agreement. Spot rates are negotiated on the spot and are normally only applicable for a few days with minimal volume.

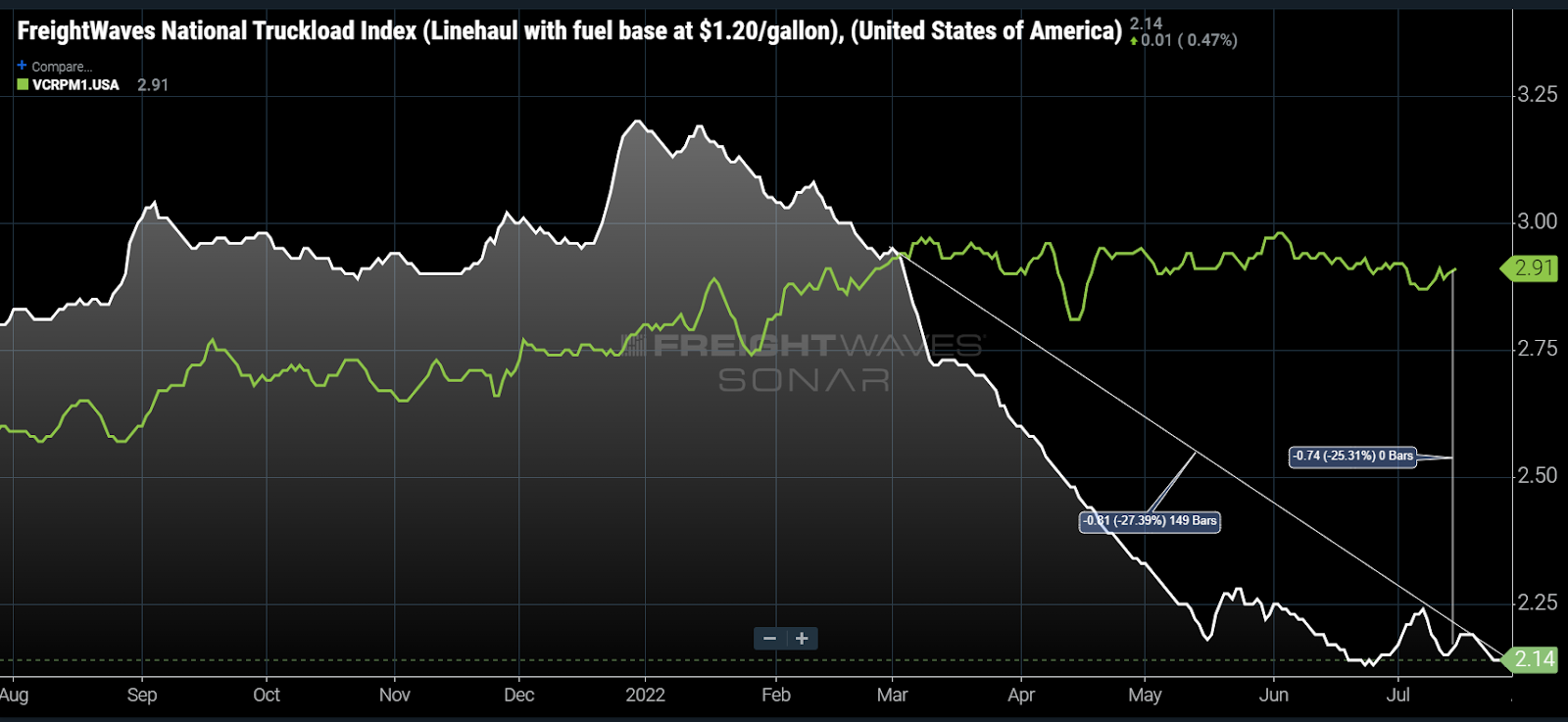

Contract rate agreements typically have a life span of around 12 months but can be longer or shorter. Many shippers transitioned to a shorter procurement cycle during the pandemic thanks to their inability to secure capacity reliably, essentially bidding against one another and driving up rates faster than ever. Contract rates increased ~49% from June 2020 to March 2022.

Since March, there has been minimal movement in contract rates, but they are showing early signs of deterioration, falling about 2% since early June. Spot rates, assuming a base level of fuel cost around $1.20 per gallon, have dropped 27% over the same period. This has created a 74-cent-per-mile difference between the spot (NTIL12) and contract rate (VCRPM1) indices.

In 2019 the spread between spot and contract averaged -24 cents per mile. Contract rates barely moved before falling about 2%-4% in January 2020, which shows that contract rates are less volatile.

The spread today is three times larger than it was in 2019. Shippers may have a stronger appetite for cost reduction after two years of rapid inflation.

A rate decrease will occur if demand-side conditions do not improve

Movements for contract truckload rates will ultimately be decided by the carriers and their need for equipment utilization. And so far, most publicly traded trucking companies have only mentioned minor deterioration at most while reporting strong Q2 results.

Accepted contract load volumes support this for now, showing only a marginal decline in July versus June. Compared to last July, volumes are down 3%-5%.

As for the supply side of the equation, most of the capacity growth over the past two years has been on the small fleet/owner-operator side, which heavily relies on spot market freight. The larger fleet heavy contract market has better structure to maintain elevated rate levels.

That said, the rate differential is too large to sustain for long. Some level of rate decrease will occur if demand-side conditions remain at or below current levels. Judging from history, it would appear a conservatively estimated 3%-5% decrease is all but imminent in the coming months.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new datasets each week and enhancing the client experience.

August 2, 2022

Contract Truck Rates Expected to Fall

Contract truckload rates will likely soften in the coming months

Spot rates indicate a strong dip for contracts is imminent

Zach Strickland, FW Market Expert & Market Analyst Follow on Twitter Saturday, July 30, 2022 3 minutes read Listen to this article 0:00 / 4:56 BeyondWords

Van rates on the truckload contract market will likely soften in the coming months. But, the decline won’t be as marked as what the industry saw on the spot market side.

The spread between spot and contract rates has averaged around record low levels (~-74 cents a mile) since early May. That will put downward pressure on contract rates for bids negotiated in the second half of the year. There is little precedent for such a dramatic difference, but there’s also little evidence historically that contract rates will fall as fast as they increase.

The contract truckload market behaves very differently from the spot market. Volatility is the main difference. That’s driven primarily by the way pricing is negotiated.

The RATES12 index used in this week’s chart is the difference between spot rates less a level of estimated cost of fuel and contract rates. This is done for a more apples-to-apples comparison of the two rates, as contract rates include a portion of fuel cost and pass a lot of it along in the form of a fuel surcharge. This mechanism is largely absent from spot rates.

Contract truckload rates have barely budged since March, but red flags are already appearing

The contract or published rate market is simply an agreement between shipper and carrier that is in place for an extended period of time. The commitment is somewhat tenuous as neither volume nor service is guaranteed in most instances.

The only binding portion is, if the shipper tenders a load(s) to the carrier and the carrier is willing and able to transport the customer’s freight, it will do it for a predetermined price until the expiration of the agreement. Spot rates are negotiated on the spot and are normally only applicable for a few days with minimal volume.

Contract rate agreements typically have a life span of around 12 months but can be longer or shorter. Many shippers transitioned to a shorter procurement cycle during the pandemic thanks to their inability to secure capacity reliably, essentially bidding against one another and driving up rates faster than ever. Contract rates increased ~49% from June 2020 to March 2022.

Since March, there has been minimal movement in contract rates, but they are showing early signs of deterioration, falling about 2% since early June. Spot rates, assuming a base level of fuel cost around $1.20 per gallon, have dropped 27% over the same period. This has created a 74-cent-per-mile difference between the spot (NTIL12) and contract rate (VCRPM1) indices.

In 2019 the spread between spot and contract averaged -24 cents per mile. Contract rates barely moved before falling about 2%-4% in January 2020, which shows that contract rates are less volatile.

The spread today is three times larger than it was in 2019. Shippers may have a stronger appetite for cost reduction after two years of rapid inflation.

A rate decrease will occur if demand-side conditions do not improve

Movements for contract truckload rates will ultimately be decided by the carriers and their need for equipment utilization. And so far, most publicly traded trucking companies have only mentioned minor deterioration at most while reporting strong Q2 results.

Accepted contract load volumes support this for now, showing only a marginal decline in July versus June. Compared to last July, volumes are down 3%-5%.

As for the supply side of the equation, most of the capacity growth over the past two years has been on the small fleet/owner-operator side, which heavily relies on spot market freight. The larger fleet heavy contract market has better structure to maintain elevated rate levels.

That said, the rate differential is too large to sustain for long. Some level of rate decrease will occur if demand-side conditions remain at or below current levels. Judging from history, it would appear a conservatively estimated 3%-5% decrease is all but imminent in the coming months.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new datasets each week and enhancing the client experience.