The Urethane Blog

Everchem Updates

VOLUME XXI

September 14, 2023

Everchem’s exclusive Closers Only Club is reserved for only the highest caliber brass-baller salesmen in the chemical industry. Watch the hype video and be introduced to the top of the league: — read more

August 2, 2022

Tenex Capital Management Exits SES Foam

| New York, NY – August 2, 2022 – Tenex Capital Management (“Tenex”) is pleased to announce the sale of SES Foam, a leading manufacturer of spray foam insulation, to Holcim, a global leader in sustainable building solutions. The sale marks the realization of Tenex’s SES Foam insulation portfolio, which also included an investment in US GreenFiber in 2013 and continued with its investment in SES Foam in 2016. Since Tenex’s initial investment in SES Foam, the business has expanded rapidly, with revenue increasing approximately six-fold, entirely through organic growth. SES Foam CEO Charles Valentine commented, “Tenex was an invaluable partner for SES, providing us the resources we needed to help execute on our ambitious growth plans. The Tenex team aided SES in scaling our team, supporting critical new product launches, and vertically integrating our blending operations, which enabled SES to thrive throughout the pandemic and capture market share over the years by delivering superior products and best-in-class service to the marketplace.” Tenex Managing Director Gabe Wood said, “We are thrilled for Charles, Adam Faber and the entire SES team for their remarkable achievements over the last six years, and we’re honored to have played a small part in this latest chapter of their incredible story. This is an exciting new phase for the company, and we are confident that SES will continue to ascend to new heights as part of Holcim.” The transaction closed on July 29, 2022. Houlihan Lokey served as lead financial advisor to SES Foam, and Lazard served as co-advisor. |

| About SES Foam: Founded in 2009 and based in Spring, TX, SES has a history of innovation with solutions like SucraSeal®, the first sucrose-based spray foam insulation to be certified by the US Department of Agriculture for its high bio-based content. SES offers superior products that improve buildings’ energy efficiency and thermal comfort, while lowering their carbon footprint. The company stands out for its value-added services to contractors, including onsite technical instruction, business consulting, branding and lead generation support. For additional information, please visit www.sesfoam.com. |

| About Tenex Capital Management: Tenex Capital Management is a private equity firm that invests in middle market companies. Tenex uses an in-house team of hybrid investment professionals skilled in operational leadership, investing, and capital markets structuring to maximize long-term value creation. Tenex’s deep operating experience allows the firm to collaborate with management teams to capitalize on business and market opportunities. Tenex has successfully invested in a diverse range of industries, including industrials, business and tech-enabled services, healthcare, building products, and auto aftermarket, among others. For additional information, please visit www.tenexcm.com. |

August 2, 2022

Contract truckload rates will likely soften in the coming months

Spot rates indicate a strong dip for contracts is imminent

Zach Strickland, FW Market Expert & Market Analyst Follow on Twitter Saturday, July 30, 2022 3 minutes read Listen to this article 0:00 / 4:56 BeyondWords

Van rates on the truckload contract market will likely soften in the coming months. But, the decline won’t be as marked as what the industry saw on the spot market side.

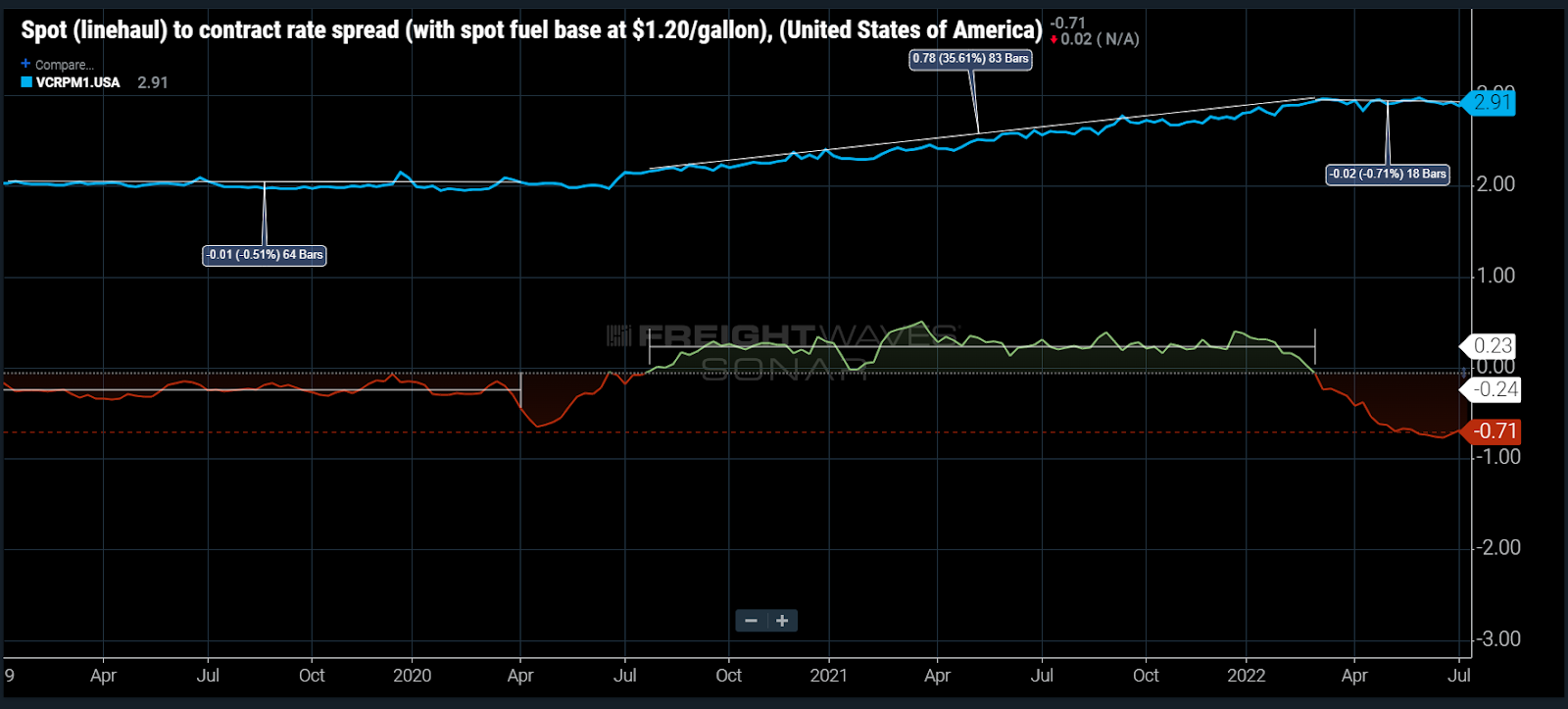

The spread between spot and contract rates has averaged around record low levels (~-74 cents a mile) since early May. That will put downward pressure on contract rates for bids negotiated in the second half of the year. There is little precedent for such a dramatic difference, but there’s also little evidence historically that contract rates will fall as fast as they increase.

The contract truckload market behaves very differently from the spot market. Volatility is the main difference. That’s driven primarily by the way pricing is negotiated.

The RATES12 index used in this week’s chart is the difference between spot rates less a level of estimated cost of fuel and contract rates. This is done for a more apples-to-apples comparison of the two rates, as contract rates include a portion of fuel cost and pass a lot of it along in the form of a fuel surcharge. This mechanism is largely absent from spot rates.

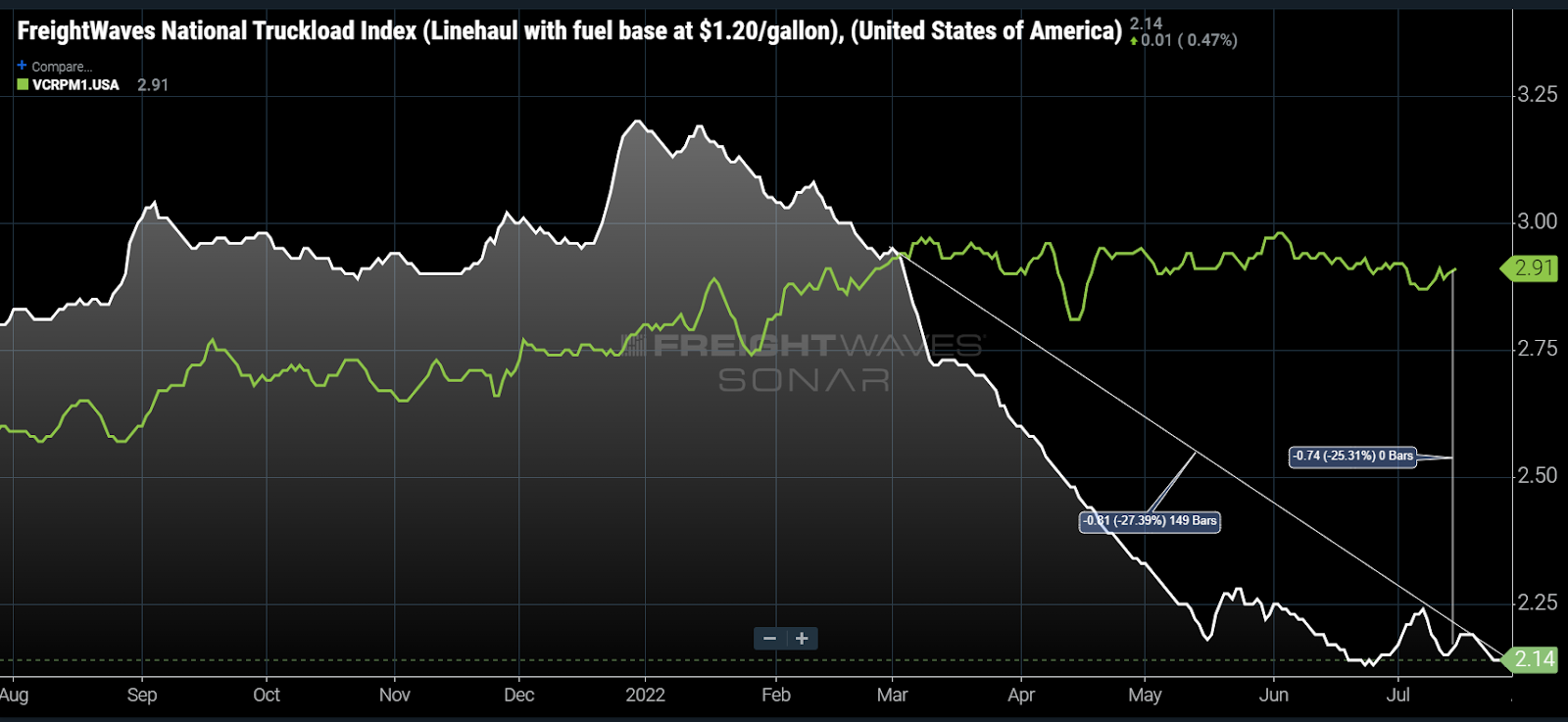

Contract truckload rates have barely budged since March, but red flags are already appearing

The contract or published rate market is simply an agreement between shipper and carrier that is in place for an extended period of time. The commitment is somewhat tenuous as neither volume nor service is guaranteed in most instances.

The only binding portion is, if the shipper tenders a load(s) to the carrier and the carrier is willing and able to transport the customer’s freight, it will do it for a predetermined price until the expiration of the agreement. Spot rates are negotiated on the spot and are normally only applicable for a few days with minimal volume.

Contract rate agreements typically have a life span of around 12 months but can be longer or shorter. Many shippers transitioned to a shorter procurement cycle during the pandemic thanks to their inability to secure capacity reliably, essentially bidding against one another and driving up rates faster than ever. Contract rates increased ~49% from June 2020 to March 2022.

Since March, there has been minimal movement in contract rates, but they are showing early signs of deterioration, falling about 2% since early June. Spot rates, assuming a base level of fuel cost around $1.20 per gallon, have dropped 27% over the same period. This has created a 74-cent-per-mile difference between the spot (NTIL12) and contract rate (VCRPM1) indices.

In 2019 the spread between spot and contract averaged -24 cents per mile. Contract rates barely moved before falling about 2%-4% in January 2020, which shows that contract rates are less volatile.

The spread today is three times larger than it was in 2019. Shippers may have a stronger appetite for cost reduction after two years of rapid inflation.

A rate decrease will occur if demand-side conditions do not improve

Movements for contract truckload rates will ultimately be decided by the carriers and their need for equipment utilization. And so far, most publicly traded trucking companies have only mentioned minor deterioration at most while reporting strong Q2 results.

Accepted contract load volumes support this for now, showing only a marginal decline in July versus June. Compared to last July, volumes are down 3%-5%.

As for the supply side of the equation, most of the capacity growth over the past two years has been on the small fleet/owner-operator side, which heavily relies on spot market freight. The larger fleet heavy contract market has better structure to maintain elevated rate levels.

That said, the rate differential is too large to sustain for long. Some level of rate decrease will occur if demand-side conditions remain at or below current levels. Judging from history, it would appear a conservatively estimated 3%-5% decrease is all but imminent in the coming months.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new datasets each week and enhancing the client experience.

August 2, 2022

Contract truckload rates will likely soften in the coming months

Spot rates indicate a strong dip for contracts is imminent

Zach Strickland, FW Market Expert & Market Analyst Follow on Twitter Saturday, July 30, 2022 3 minutes read Listen to this article 0:00 / 4:56 BeyondWords

Van rates on the truckload contract market will likely soften in the coming months. But, the decline won’t be as marked as what the industry saw on the spot market side.

The spread between spot and contract rates has averaged around record low levels (~-74 cents a mile) since early May. That will put downward pressure on contract rates for bids negotiated in the second half of the year. There is little precedent for such a dramatic difference, but there’s also little evidence historically that contract rates will fall as fast as they increase.

The contract truckload market behaves very differently from the spot market. Volatility is the main difference. That’s driven primarily by the way pricing is negotiated.

The RATES12 index used in this week’s chart is the difference between spot rates less a level of estimated cost of fuel and contract rates. This is done for a more apples-to-apples comparison of the two rates, as contract rates include a portion of fuel cost and pass a lot of it along in the form of a fuel surcharge. This mechanism is largely absent from spot rates.

Contract truckload rates have barely budged since March, but red flags are already appearing

The contract or published rate market is simply an agreement between shipper and carrier that is in place for an extended period of time. The commitment is somewhat tenuous as neither volume nor service is guaranteed in most instances.

The only binding portion is, if the shipper tenders a load(s) to the carrier and the carrier is willing and able to transport the customer’s freight, it will do it for a predetermined price until the expiration of the agreement. Spot rates are negotiated on the spot and are normally only applicable for a few days with minimal volume.

Contract rate agreements typically have a life span of around 12 months but can be longer or shorter. Many shippers transitioned to a shorter procurement cycle during the pandemic thanks to their inability to secure capacity reliably, essentially bidding against one another and driving up rates faster than ever. Contract rates increased ~49% from June 2020 to March 2022.

Since March, there has been minimal movement in contract rates, but they are showing early signs of deterioration, falling about 2% since early June. Spot rates, assuming a base level of fuel cost around $1.20 per gallon, have dropped 27% over the same period. This has created a 74-cent-per-mile difference between the spot (NTIL12) and contract rate (VCRPM1) indices.

In 2019 the spread between spot and contract averaged -24 cents per mile. Contract rates barely moved before falling about 2%-4% in January 2020, which shows that contract rates are less volatile.

The spread today is three times larger than it was in 2019. Shippers may have a stronger appetite for cost reduction after two years of rapid inflation.

A rate decrease will occur if demand-side conditions do not improve

Movements for contract truckload rates will ultimately be decided by the carriers and their need for equipment utilization. And so far, most publicly traded trucking companies have only mentioned minor deterioration at most while reporting strong Q2 results.

Accepted contract load volumes support this for now, showing only a marginal decline in July versus June. Compared to last July, volumes are down 3%-5%.

As for the supply side of the equation, most of the capacity growth over the past two years has been on the small fleet/owner-operator side, which heavily relies on spot market freight. The larger fleet heavy contract market has better structure to maintain elevated rate levels.

That said, the rate differential is too large to sustain for long. Some level of rate decrease will occur if demand-side conditions remain at or below current levels. Judging from history, it would appear a conservatively estimated 3%-5% decrease is all but imminent in the coming months.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new datasets each week and enhancing the client experience.

August 2, 2022

Leggett & Platt Cuts FY22 Guidance Citing Macroeconomic Uncertainties

Shivani KumaresanTue, August 2, 2022 at 8:36 AM·1 min readIn this article:

LEG+0.73%Watchlist

- Leggett & Platt Inc (NYSE: LEG) reported second-quarter FY22 sales growth of 5% year-on-year to $1.33 billion, in line with the consensus. Organic sales rose 5%.

- Trade sales from Bedding products rose 1% Y/Y to $612.5 million, Specialized Products increased 8% to $260.1 million, and Furniture, Flooring & Textile Products rose 10% to $461.6 million.

- Gross profit for the quarter was $268.4 million, with a profit margin of 20.1%.

- The company held $269.9 million in cash and equivalents as of June 30, 2022. Net cash from operating activities in the quarter jumped 119.5% Y/Y to $90 million.

- EBITDA fell 2% Y/Y to $187.5 million, and the adjusted EBITDA margin contracted 100 basis points Y/Y to 14.1%.

- EPS of $0.70 matched the consensus of $0.70.

- “We are lowering our full-year guidance to reflect macroeconomic uncertainties including impacts of inflation, tightening monetary policy, and softening consumer demand continuing through the back half of the year,” said President and CEO Mitch Dolloff.

- Outlook: Leggett lowered FY22 sales guidance to $5.2 billion – $5.4 billion from $5.3 billion – $5.6 billion, against the consensus of $5.3 billion.

- The company cut FY22 EPS outlook to $2.65 – $2.80 from $2.70 – $3.00, versus the consensus of $2.72.

https://finance.yahoo.com/news/leggett-platt-cuts-fy22-guidance-123631528.html

August 2, 2022

Leggett & Platt Cuts FY22 Guidance Citing Macroeconomic Uncertainties

Shivani KumaresanTue, August 2, 2022 at 8:36 AM·1 min readIn this article:

LEG+0.73%Watchlist

- Leggett & Platt Inc (NYSE: LEG) reported second-quarter FY22 sales growth of 5% year-on-year to $1.33 billion, in line with the consensus. Organic sales rose 5%.

- Trade sales from Bedding products rose 1% Y/Y to $612.5 million, Specialized Products increased 8% to $260.1 million, and Furniture, Flooring & Textile Products rose 10% to $461.6 million.

- Gross profit for the quarter was $268.4 million, with a profit margin of 20.1%.

- The company held $269.9 million in cash and equivalents as of June 30, 2022. Net cash from operating activities in the quarter jumped 119.5% Y/Y to $90 million.

- EBITDA fell 2% Y/Y to $187.5 million, and the adjusted EBITDA margin contracted 100 basis points Y/Y to 14.1%.

- EPS of $0.70 matched the consensus of $0.70.

- “We are lowering our full-year guidance to reflect macroeconomic uncertainties including impacts of inflation, tightening monetary policy, and softening consumer demand continuing through the back half of the year,” said President and CEO Mitch Dolloff.

- Outlook: Leggett lowered FY22 sales guidance to $5.2 billion – $5.4 billion from $5.3 billion – $5.6 billion, against the consensus of $5.3 billion.

- The company cut FY22 EPS outlook to $2.65 – $2.80 from $2.70 – $3.00, versus the consensus of $2.72.

https://finance.yahoo.com/news/leggett-platt-cuts-fy22-guidance-123631528.html