Everchem’s exclusive Closers Only Club is reserved for only the highest caliber brass-baller salesmen in the chemical industry. Watch the hype video and be introduced to the top of the league: —read more

Has The Housing Market Bottomed? The Surprising Result From A Little-Known Market Indicator

by Tyler Durden

Monday, Jan 30, 2023 – 03:20 PM

It may come as a bit of a shock to those who have been following the creeping freeze in housing transactions as the bid-ask spread grows to monstrous proportions, leading to a record crash in pending home sales…

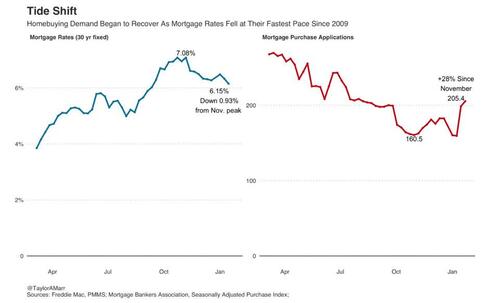

… but even though mortgage rates ticked higher back to 6% in January, there is growing speculation that the housing market has bottomed. Why? Because as Goldman’s Rich Provorotsky notes, “bet you didn’t know there were housing price futures…they bottomed in Q4 and have been rallying.” Indeed, the Housing Composite Index traded on the CME is up decidedly in the past month after hitting a 16 month low in November.

Why this surprising bounce? A big reason for the unexpected rebound may be a recent report from real estate company Redfin which last Wednesday reported that “the housing market has begun to recover from a trough in the second week of November with buyers returning at a faster pace than sellers. The number of Redfin customers asking for first tours has improved by 17 percentage points from the November low, and the number of clients contacting.”

Furthermore, according to the report, Redfin agents to begin the home-buying process has improved by 13 points: “I’ve seen more homes go under contract this month than in the entire fourth quarter,” Angela Langone, a San Jose, California, agent, said in the report.

Among notable market moves, Redfin points to mortgage applications which are up 28% from early November as the average 30-year-fixed mortgage rate has dropped to 6.15% from its peak of 7.08% in November, the biggest decline since 2009. Pending home sales rose 3% in December from November.

Preliminary data on the share of Redfin agents’ offers facing bidding wars points to small upticks in the Seattle and Tampa markets this month (however, since this is an uneven trend, expect it to take some time before bidding wars nationally show an upward trend).

“Bidding wars are back in Seattle,” said local Redfin real estate agent Shoshana Godwin. “One of our Issaquah listings got 12 offers and is under contract for $155,000 over the $1.4 million list price. The buyer waived every contingency, handed over $300,000 of earnest money and is letting the seller stay for free for two months after closing. Another home in Seattle’s popular Ballard neighborhood was recently delisted after sitting on the market for over three months. The seller relisted it last week and it went pending in under a day.”

Eric Auciello, Redfin’s team manager in Tampa, has seen three modest single-family homes priced around $300,000 wind up in bidding wars in central Florida this month, with 16, 17 and 23 competing offers, respectively.

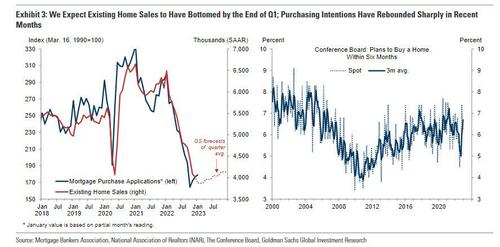

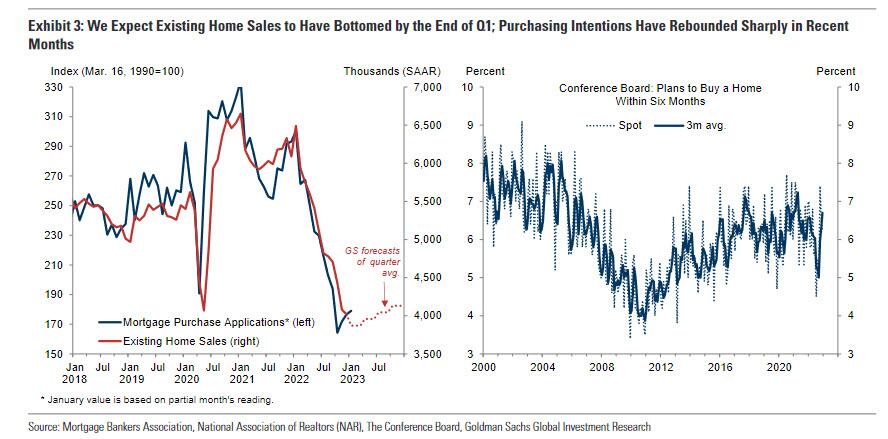

But while one can accuse Redfin of bias – after all the company recently laid off some 13% of its employees due to the housing market collapse so it is certainly interested in sparking some animal spirits in the sector – it is not alone in predicting a housing recovery. One week ago, Goldman’s Jan Hatzius published the bank’s Housing Outlook for 2023 in which he predicted that “home sales appear set to turn higher.” That’s because “mortgage purchase applications have averaged 9% above their October trough so far in January and survey-based measures of purchasing intentions have rebounded sharply” and while Goldman expects that existing home sales could decline slightly further “but will likely bottom in Q1 (GS forecast: Q1 average of 3.85mn saar vs. 4.02mn in December) before rebounding modestly by year-end (GS forecast: Q4 average of 4.1mn).”

Here are some more observations from the Goldman note (full report available to pro subs):

We forecast that housing starts will take longer to stabilize, declining to a trough pace of 1¼mn in 2023Q4 (vs. 1.4mn in 2022Q4) before recovering next year. We expect completions to total 1½mn this year, the most since 2007, which will help to clear the backlog of homes under construction and contribute to a modest increase in the homeowner vacancy rate (GS forecast of 1.2% in 2023Q4 vs. 0.9% now and 1.4% in 2019Q4).

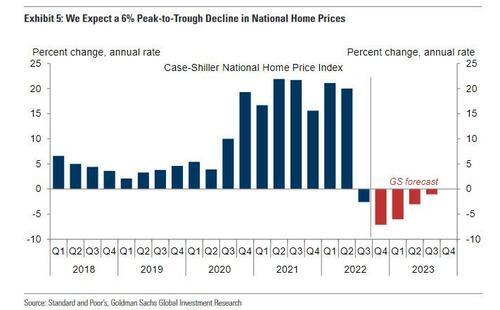

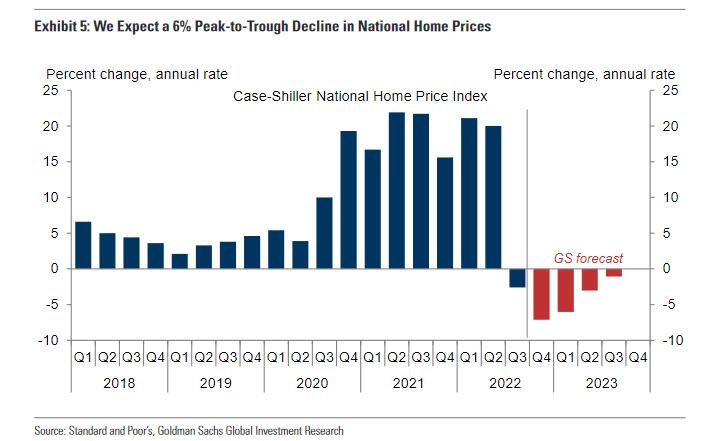

We expect a peak-to-trough decline in national home prices of roughly 6% and for prices to stop declining around mid-year.

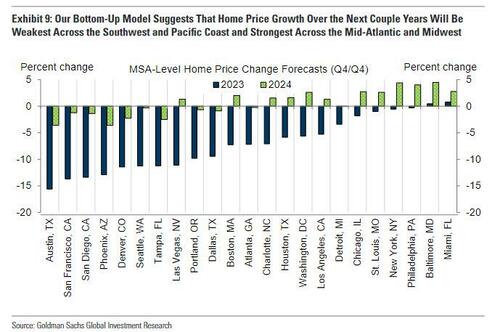

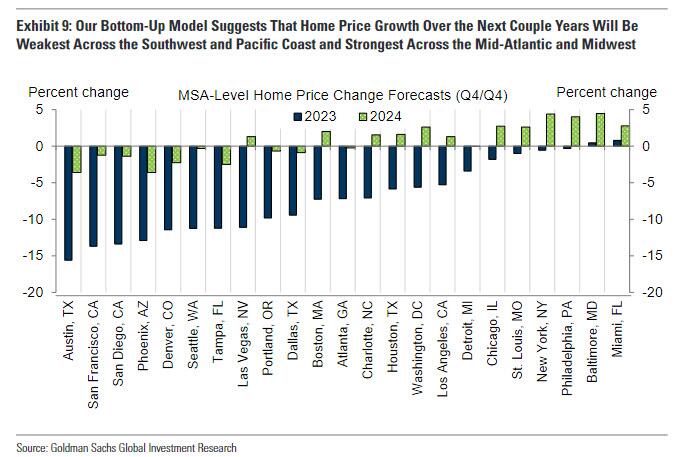

On a regional basis, we project larger declines across the Pacific Coast and Southwest regions—which have seen the largest increases in inventory on average—and more modest declines across the Mid-Atlantic and Midwest—which have maintained greater affordability over the past couple years.

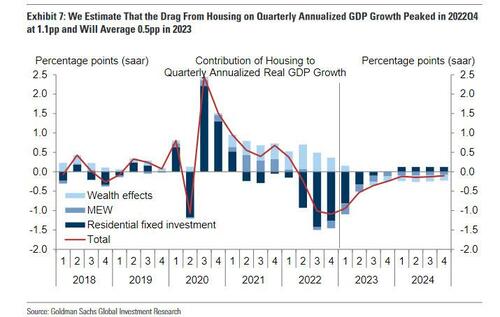

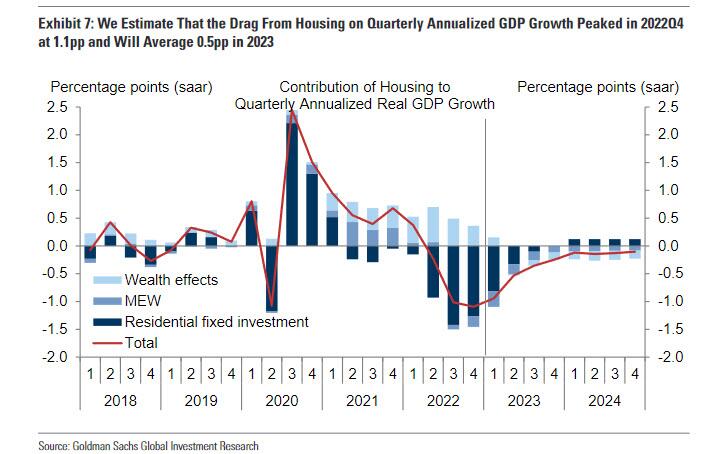

Higher rates and lower home prices will increase the drag on GDP growth from negative wealth effects and declining mortgage equity withdrawal, but we believe that the aggregate drag on GDP growth from the housing sector peaked in 2022Q4 at 1.1pp and will moderate to just 0.25pp by 2023Q4.

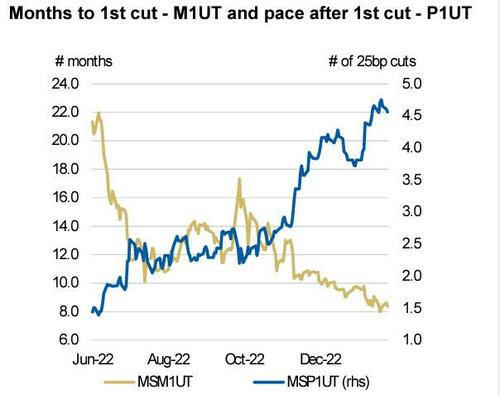

If the housing price futures market – and Goldman – is right in pricing in a housing trough than the consequences could confound markets: on one hand, a stabilization in housing will likely make any coming recession less severe; on the other, since housing is the primary channel by which the Fed can slowdown the economy, any failure to cripple this key US asset, could mean that Powell will be stuck in a “higher for longer” mode for, well, longer than the market expects. As a reminder, as the following Morgan Stanley chart shows, consensus is that the Fed is about 8 months away from its first rate cut, which will be promptly followed by ~4.5 25bps rate cuts.

DORAVILLE, Ga. – Serta Simmons Bedding’s Chapter 11 bankruptcy filing Monday provides a look at the company’s financial status showing the company owes more than $62 million to its top 10 unsecured creditors.

The petition, filed in the U.S. Bankruptcy Court for the Southern District of Texas, lists assets and liabilities of $1 billion to $10 billion. The filing that includes SSB and 13 of its affiliates estimates its number of creditors to be somewhere between 25,000 and 50,000.

The filing lists the company’s 30 largest unsecured claims. The hardest hit were suppliers of springs, foam and nonwovens, and logistics companies.

EPS of $0.46 misses by $0.11 | Revenue of $11.86B (-17.44% Y/Y) misses by $186.55M

Dow Inc. (NYSE:DOW) Q4 2022 Results Conference Call January 26, 2023 8:00 AM ET

Company Participants

Pankaj Gupta – Investor Relations, Vice President

Jim Fitterling – Chairman and Chief Executive Officer

Howard Ungerleider – President and Chief Financial Officer

Conference Call Participants

Vincent Andrews – Morgan Stanley

David Begleiter – Deutsche Bank

Hassan Ahmed – Alembic Global Advisors

P.J. Juvekar – Citi

Jeff Zekauskas – JPMorgan

John McNulty – BMO

Michal Sison – Wells Fargo

Kevin McCarthy – Vertical Research Partners

Matthew Skowronski – Credit Suisse

Christopher Parkinson – Mizuho Securities

Frank Mitch – Fermium Research

Jim Fitterling

Thank you, Pankaj. Beginning on Slide 3. In the fourth quarter, Team Dow continued to take proactive actions to navigate slower GDP growth, challenging energy markets and customer destocking. We proactively lowered our operating rates to effectively manage working capital, implemented operational mitigation plans and cost saving measures and prioritized higher-value products where demand remained resilient, including in functional polymers and performance silicones as well as in mobility, renewable energy and pharma end markets.

These actions, combined with our continued focus on cash enabled us to deliver cash flow from operations of $2.1 billion in the quarter. Cash flow conversion was 166%, and we returned $620 million to shareholders. Dow’s cash generation reflects our continued focus on operational and financial discipline, which was important as we navigated an extremely dynamic year in 2022, as you see on Slide 4.

In the first half of the year, we capitalized on strong demand across our diverse global portfolio while leveraging our derivative and feedstock flexibility and low-cost positions to mitigate higher raw material and energy costs. In the second half of the year, economic conditions deteriorated driven by record inflation, rising interest rates, ongoing pandemic lockdowns in China and continued geopolitical tensions.

In the face of these evolving market dynamics, Dow was resilient, generating cash flow from operations of $7.5 billion for the full year. While executing our disciplined and balanced approach to capital allocation. We delivered returns on invested capital of 15%, above our 13% across the economic cycle target, as we prioritized higher return, lower risk and faster payback investments.

We achieved credit rating and outlook upgrades as a result of our strengthened balance sheet, and we have no substantive debt maturities due until 2027. And we returned a total of $4.3 billion to shareholders, including $2.3 billion in share repurchases and $2 billion in dividends.

Moving to the Industrial Intermediates & Infrastructure segment. Net sales were $3.7 billion, down 20% from the year ago period. Volumes declined primarily due to lower demand in Europe for industrial, consumer durables and building and construction applications. Sequentially, net sales were down 10% as seasonal demand increases for deicing fluid were more than offset by declines in building and construction, consumer durables and industrial applications.

Operating EBIT for the segment was $164 million compared to $595 million in the year-ago period, driven by lower demand and increasing energy costs, particularly in Europe. Sequentially, operating EBIT margins expanded by 40 basis points as lower energy costs versus the prior quarter were partly offset by lower volumes.

Howard Ungerleider

Thank you, Jim, and good morning, everyone. We expect the market dynamics we experienced in late 2022 to continue into early ’23. While the pace of inflation has moderated, overall cost levels remain elevated, which has continued to trigger tighter monetary policy in most parts of the world and is weighing on both business investment and consumer sentiment.

The majority of economic forecasts are calling for slower GDP growth globally relative to 2022, although dynamics differ by region, with most regions except Europe still forecasting positive year-on-year growth. In the U.S., we see signs of moderating demand and the continuation of year-end destocking trends early in the quarter.

Building and construction end markets have been particularly impacted by inflation and rising interest rates with housing starts declining by more than 20% year-over-year in December.

Manufacturing PMI contracted for the third consecutive month of 48, while light vehicle sales in the U.S. were down for the full year by 8 percentage points. Easing inflation is leading to improving consumer confidence, albeit from depressed levels in late 2022, while consumer spending remains resilient. In Europe, we expect demand to remain constrained despite recent improvements in regional energy prices.

While the move to five-year highs in gas storage is a positive sign, changing weather forecasts are leading to volatility in the futures markets. High inflation and geopolitical tensions continue to weigh on consumer spending and industrial production. December manufacturing PMI has been contracting since July, and construction PMI reached its lowest level since May.

In China, while we’re very encouraged by recent ships in COVID policy to ease restrictions and open up orders, we expect these actions to take some time to improve economic activity. This is an area we’re closely monitoring as it has the potential to provide a source of significant demand recovery following the Lunar New Year.

And in Latin America, overall economic growth is expected to slow, driven by political tensions, high inflation and restrictive monetary policy. Given this dynamic backdrop, we will continue to take a region by region, business-by-business approach to managing our operations and adapting our businesses to the evolving market realities.

And the Industrial Intermediates & Infrastructure segment, demand remains stable for energy markets, and we’re monitoring demand for deicing fluids with a warmer than average winter. However, inflationary pressures in contracting PMIs continue to impact industrial demand, and we expect lower seasonal volumes in building construction end markets. We also anticipate an approximately $25 million headwind due to a third-party outage, which is causing a supply disruption on the U.S. Gulf Coast from winter storm Elliott.

And in the Performance Materials & Coatings segment, we expect demand recovery for performance silicones following year-end customer destocking as well as improved supply availability and lower costs. However, we also anticipate lower siloxane pricing in the quarter as we continue to see pressure from increased industry supply.

Jim Fitterling

In Industrial Intermediates & Infrastructure, our latest alkoxylates capacity investment in the United States was completed in the third quarter of 2022, and our next in Europe will be completed in the first quarter of this year. These projects will further serve high-value markets in home care and pharma and are just a start.

Our next wave of alkoxylates capacity investments remain on track. In fact, Dow has already successfully begun locking in supply contracts with several consumer and pharmaceutical customers to support the next wave of growth.

And in Performance Materials & Coatings, we completed 16 downstream silicone debottleneck projects in 2022 to meet demand for high performance, building and construction, personal care and mobility applications.

Additionally, we accelerated the delivery of our digitalization initiatives and now expect the full $300 million run rate EBITDA to fully materialize by the end of 2023, well ahead of our prior target of 2025. As a result, we anticipate our digital sales to comprise 50% of total revenue by 2025.

Looking forward, we expect to continue growth investments in our global operations, including key capital investments in higher-margin polyurethane systems and additional alkoxylate capacity, incremental projects to expand downstream, high-value ethylene derivative capacity and continued coatings and silicon debottlenecking projects. We will also continue progressing our operating investments to improve production capabilities and reliability as we shift our product mix toward higher growth and higher-value markets.

Vincent Andrews

Good morning everyone. Wondering if you could just unpack the outlook for Performance Materials & Coatings a little bit. And it sounds like there’s just a lot of moving parts right now with weak China in the fourth quarter but now reopening, some issues with new supply coming into the market. So obviously, uncertainty about how far and how fast China will reopen. But could you give us sort of the range of outcomes for how this segment might recover as we move through the year, representing that it could be a wide range?

Jim Fitterling

Sure. Good morning, Vince. Thanks for the question. First, I think it’s important to look back at the fourth quarter on PM&C and understand the fourth quarter. Coatings and Performance Monomers kind of got back to the normal fourth quarter seasonality that we would see, which a year ago was very different because we were still recovering from all the supply disruptions from winter storm URI and everything else that was associated with that. So I think you’ll see that they’ll come back to a more normal season in 2023.

And you also saw the impact of destocking. Destocking in the fourth quarter represented, and this is across the businesses, about 50% to 60% of the slowdown that we saw in the fourth quarter. So I think the destocking is going to work itself through in the first quarter. And then I think you’ll see us get back to normal seasonality there.

I do think positively on China for coatings and performance monomers. I do think we’re seeing China opening up. We’re not seeing issues with people coming to work. So I think we’re optimistic that the government will probably try to stimulate the construction economy there, and we’ll start to see that take off through the year.

On silicones and siloxanes, you had two impacts. One was the market impact of things slowing, which was the lower siloxane prices that hit hardest in China, obviously, at the end of the year. The other one was self-inflicted. We happen to have all three of the silicones pillar plants, the siloxanes pillar plant down at some point in the fourth quarter. And that lower operating rate really hurt us. They’re, all 3 back up and running. So I think that issue is behind us.

So I would expect you’ll start to see siloxanes demand pick back up. We saw destocking in all the downstream areas in silicones, personal care, home consumer goods, and we also saw it, obviously, in building and construction. I think that will start to rebound as the year progresses.

David Begleiter

Thank you. Good morning. Jim and Howard, given the recent decline in European natural gas prices, how are you thinking about the competitiveness of the European operations going forward?

Jim Fitterling

Good morning David. Very good question. Obviously, the European situation has been tough on all the European producers over this past year. In fact, if you think about the year-over-year performance for Dow for the full year, 60% of the decline in EBIT was related to Europe and that energy situation.

So this is very targeted. Incrementally, we saw a step change in the fourth quarter, obviously driven by the warmer winter and the inventory levels being back up. And they’ve done an admirable job, especially in Germany, of switching away from Russian natural gas over to other sources.

So that has helped. But we still have to take a look at long-term energy policies and work with the governments, both EU and the member states on energy policies because we’re a long way away from long-term competitiveness in Europe. I would say the decisions we announced today around restructuring, right now, we’ve looked at locations that are going to be challenged in any scenario long term, and we’ll take actions on those.

But on large sites, like our large cracker sites, we’re still able to run cash flow positive, and we’re working hard on that energy situation. We’ll continue to analyze that through this year and see what kind of work we can do with the governments there to make them more competitive long term.

John McNulty

Thanks for taking my question. So it seemed like the destocking was kind of at really accelerated levels in the fourth quarter. Can you give us a little bit of color as to which of the segments do you feel like you’re largely through that? And if anything, you may be — maybe we’re even at a balance side or even a restock phase? And I guess tied to that, — can you speak to the operating rates you saw in the fourth quarter and how you expect that to change as we look to 1Q?

Jim Fitterling

Sure. Good morning John. Good Question. I would say it accelerated in December. We made announcement in October that we were going to reduce some operating rates in ethylene, polyethylene because of some logistics constraints and other things that happen. We saw better logistics in December. December was our best export month of the year for marine pack cargo, so that’s positive. But at the same time, manufacturing activity in the last half of December really slowed. And so you could see that in the order pattern. And that stayed relatively slow the first half of January.

I do think we’re seeing manufacturing activity come back right now. We’re seeing that in the order book. I would not say that we’re at a restocking state yet. But I do think as the quarter progresses, we will get there because second and third quarter are typically our highest volume quarters. And there is not a lot of excess inventory anywhere in the change right now. So I do think it’s coming, but it isn’t here as we sit here right now today.

Michael Sison

Hey, good morning guys. What was the impact from the lower operating rates in the fourth quarter on EBITDA, meaning if you were at normal operating rates, what would that be? And then is that impact similar for the first quarter? And when do you think you can see your operating rates sort of improve back to normal rates in ’23?

Jim Fitterling

Yes. Just to give you an idea, I would say, probably you saw because of destocking, you probably saw a 10% lower operating rate due to destocking. Rough numbers, Howard, where do you think, [indiscernible] million.

Howard Ungerleider

Yes, I would say 10 percentage points. And that’s — I mean, when you think about every percentage point. Yes, look, I would say it this way, Mike. When you look at the sequential decline in probably two-thirds of that EBITDA drop was because of the destocking. And then the other balance was really the seasonal — just a seasonal sequential decline because we’re in more of a Northern Hemisphere business. And obviously, our coatings business typically is a seasonal low point in the fourth quarter.

Steve Byren

Yes, thank you. That 2,000-headcount reduction, how much of that is these assets in Europe that you’re planning to shutter? Or can you highlight what operations, is this commercial or back-office headcount? And then just one other quick one. Your partnership with Mura, when that’s at scale, you’re using the pyrolysis oil as cracker feedstock, how would you expect the profitability of that versus naphtha or ethane-based feedstock?

Jim Fitterling

Sure. Good morning Steve, good questions. 2,000 headcount reduction is not all specific to Europe, although Europe is a big part of the earnings decline that’s driving us to take these actions.

The site and asset decisions we’ve made so far are really smaller locations, smaller scale locations where we know they will be challenged through the year. We haven’t released a list of those we’re working through that with the European Works Councils, et cetera, but we will be doing that as we get toward the end of this quarter.

But — the $1 billion is really made up of two buckets: $500 million is structural cost reductions. That’s the headcount reductions, that’s productivity and end-to-end process improvement. So we’re really building off that digital work we’ve done, and that would work on improving processes and customer service and then the asset decisions. And then $500 million will just be reduced spending, turnaround spend, which Howard had mentioned, $300 million, leveraging our volume on lower purchased raw materials, logistics and utilities because we do see some supply/demand imbalances and the ability to do that and just tightening the belt to this environment.

So I would say I don’t — it’s not a haircut 5% of the workforce. It will be targeted, and we target around asset decisions. It will be targeted around businesses that need to tighten. It will be targeted around — it’s not just Dow headcount. We will have contractor reductions as well at the sites. And so we’ll look at it that way.

Matthew Skowronski

Good morning. This is Matt Skowronski on for John. Two commodities that Dow participates in, siloxanes and MDI, have had competitor capacity come online recently. You called out weaker pricing in siloxanes in your guide for the first quarter. But can you just talk about how long you expect it to take for pricing these commodities to recover?

Jim Fitterling

Yes, good morning. And thank you for the question. I think we’ll see a little bit of demand improvement. But siloxanes prices have fallen to their lowest levels in some time at the end of the year, and so we start the year at those levels. I don’t think we’re expecting any immediate improvement. The downstream demand still continues to be good. Building and construction will be the thing that I think will start to tip it to the positive. So if we see a good rebound in building and construction in China, that should start to pull things to the positive and lift things up.

North America has been fairly resilient. And North America and Europe are typically slightly higher than the Chinese prices, and that continues to be the same case today. So I — that’s my outlook on siloxanes on.

On MDI, I would say the biggest difference between what’s reported in the markets on MDI in our view, is just what you believe about the RTO timing of some of the Chinese competitions, new plants that are coming online. I think our view is that, that’s going to be stretched out over a longer period of time.

Most of what’s reported would have all that 4 world-scale MDI facilities coming on in 2023. I don’t think that’s our view of how that’s going to happen. That would be more spread over the 2023 to 2025-time period. And so I think that will take some of that pressure off of MDI.

Downstream demand for MDI and for systems and the application that it goes into is really good so I don’t feel worried about that. That’s purely what your assumptions are about — that our new demand coming — or new supply coming online and the time frame

EPS of $1.49 beats by $0.08 | Revenue of $1.98B (-18.66% Y/Y) misses by $131.89M

Olin Corporation (NYSE:OLN) Q4 2022 Results Conference Call January 27, 2023 9:00 AM ET

Company Participants

Steve Keenan – Director, IR

Brett Flaugher – President, Winchester

Damian Gumpel – President, Epoxy

Patrick Schumacher – President, Chlor Alkali

Scott Sutton – CEO

Todd Slater – CFO

Scott Sutton

Yes. Thanks, Steve, and good morning to everyone. In 2022, Olin generated $12 per share of levered free cash flow, repurchased more than 25 million shares and reduced our net debt by $200 million.

It was a massive team effort after generating $9 per share of levered free cash flow in 2021. As we head into 2023, our markets are not healthy, yet our focus on levered free cash flow remains the same and we expect to generate approximately $7 per share of levered free cash flow in this recession year.

From an EBITDA perspective, we worked in the $2.4 billion to the $2.5 billion range the last 2 years and we expect to generate at least 2/3 of that average in the trough that is 2023.

For Olin, the key features of early 2023 include continuing to idle our complete global epoxy resin business due to suspended demand in the largest consuming regions of China and Europe, rectifying a transient fat supply channel in commercial ammunition via lower Olin participation rate, kicking off the operation of the blue water…

I understand that we dropped. I won’t repeat the first part of my comments, but I’ll start where I think we dropped off. So for Olin, the key features of early 2023 include continuing to idle our complete global epoxy resin business due to suspended demand in the largest consuming regions of China and Europe, rectifying a transient fat supply channel in commercial ammunition via lower Olin participation rate, kicking off the operation of the Bluewater alliance with Mitsui to manage much more the world’s liquidity in chlor alkali and recognizing another solid pricing lift in our merchant chlorine business.

While some of these features of the first quarter of 2023 are already impactful in a slightly negative way, it is still possible that we may have to take more drastic action in a subsequent quarter to recoil further and preserve product values for the rebound toward the latter part of the year.

In 2023, expect us to hold our current net debt position, keep buying shares throughout the year, gain an investment-grade rating, complete our asset footprint adjustment decisions and prepare for a quality growth story in 2024.

We’ve also updated our 2022 ESG scorecard progress on Page 10 of the presentation. This is a growing theme for Olin, and we look forward to showing the results from our focus in this area. Now Damian, Patrick and Brett will each make a few brief comments on both the situation and our initiatives across all 3 businesses and then Todd will follow with additional commentary on our 2022 accomplishments and 2023 outlook.

Damian Gumpel

Thank you, Scott, and good morning. On Slide 4, Epoxy Q4 results are partly a reflection of seasonal demand, but principally our disciplined approach to water the most challenging landscape in 14 years which led us to deeply pull back resin production that would have otherwise harmed the landscape.

While anticipating improvement in the back half of ’23, we focus today on productivity, optimizing our asset base, enhancing our sustainability profile and positioning for value-based growth.

On this last point, we supercharged the business during Q4 of 2022. Putting our differentiated systems product portfolio under seasoned leadership in new product commercialization. I look forward to sharing on future calls the role Olin epoxy plays in addressing global energy, mobility and infrastructure challenges in a sustainable way and how that translates into shareholder value growth. I’ll now turn it over to Patrick Schumacher for chlor alkali.

Mike Sison

I guess my question was, where are your operating rates now? And do you think they will — based on your guidance, stay similar through the rest of the year, given the outlook for demand?

Scott Sutton

Well, look, I would say overall, I mean, we’re certainly running lower operating rates. I mean, the highlights of those lows really are that if you went all the way down into our epoxy resin, you’d find that we’re running below 50% capacity. And that situation is certainly going to continue because we’re just not going to sell too much volume into an undervalued marketplace.

Arun Viswanathan

So first off, on that note of operating rates, it says you can run at 50% for 1 year. I think we’ve been at these low rates now for a little while. Are we — how long does that year last? I mean, how much time do we have left in that? And then I had a couple of questions on Blue Water and hydrogen as well.

Scott Sutton

Yes. Sure. Yes, I mean, that 50% rate was across effectively the whole company for a whole year. If we ran at the pricing levels established in the middle of last year, that would still deliver our recession case. So against that standard, there’s still quite a bit of room left, Arun.

Vincent Anderson

I just wanted to clarify your comments on Epoxy, just I had it clear. You said a global idling but naming just Europe and Asia markets is the reason. And I ask only because U.S. resin prices are still holding up fairly well. So is this really all epoxy resin assets are going down in the first quarter?

Scott Sutton

Well, I would say we’ve been running those at a lower level, but I’ll let Damian give a little more color on where we are right now.

Damian Gumpel

Sure. Thanks, Scott. Vince, on Epoxy, what we’ve said is that this is a globally challenged situation, the worst that we’ve seen in 14 years since the financial crisis. Most of epoxy consumption does take place in China and in Europe. And so that’s where we’ve seen the greatest impact on the landscape. Now as a result, we’ve been — for over a year now, we’ve been adjusting our production, our market participation in order to preserve value, that’s led us to continue to successfully challenge ourselves to operate at lower rates across our portfolio. We’re going to continue to do that as long as it takes and frankly, we can still go further. And it’s — for us, it’s a question of taking this opportunity to rightsize our global epoxy portfolio to focus on the assets that our customers value the most. And we’ve done a lot of that already, but we still have a lot more that we are going to do here under this challenging environment.

Jeffrey Zekauskas

And secondly, Scott, can you remind me when do the contracts with Dow expire? Is the beginning of ’25 or the end of ’25 and is that a big event for the company?

Scott Sutton

Yes. Jeff, we really weren’t going to comment on any specific customer or supplier arrangements.

Angel Castillo

Understood. No worries. And then second question, just going back to some of the discussions around the macro and some of the demand picture of what you’ve been seeing. You noted, I think, in the slide, vinyl troughing here in the first quarter and epoxy improving in the second half. I was curious, one, as we think about the 2023 outlook, how much of this — are you seeing anything in orders that gives you confidence in those rebounds? Is it more just destocking abating? Or anything that — how do you get kind of comfortable with those factors? And then as you think about just overall kind of recovery in some of that, how much of it is macro versus your ability to pull levers in parlay?

Scott Sutton

I mean we’ll start with epoxy. I mean it’s — of course, it’s very challenged right now as we’ve tried to lay out. But Damian, do you want to give a little guidance on back half.

Damian Gumpel

Sure. I mean when we look at some of the factors in the back half, we’re seeing some improved demand. I think you see the news. China, as I said, being the largest consuming region of epoxy, it’s looking like it’s emerging from its almost a year-long slumber. But we also see other areas that are starting to pull epoxies as well. If we highlighted our growth platforms and our macro trends around wind, infrastructure, electrification, mobility. Those are all that — we’re already starting to see some of that demand profile improved with our valued customers. So it’s a combination of what we see in the landscape, but more purposely, our participation in some of these platforms that are going to look to drive some improved demand recovery in the second half.

Eric Petrie

What’s embedded in your earnings outlook in terms of China and domestic consumption and at the end of last year, we saw a ramp-up of exports in epoxy as well as caustic soda. So any comments on those export levels into 2023 and impact on earnings?

Scott Sutton

Yes. No, what’s embedded is still that demand stays fairly muted, suspended for the better part of the first half of the year and then recovers. Specifically in epoxy by trade flows actually reversed out of China. But even when China recovers, still the amount of imports going into China is likely to be less than it was before because there have been some structural capacity adds there. And what this has taught us knowing that we really didn’t expect sort of the worst conditions in 15 years. But what it has taught us here is that we certainly have more trough minimization footprint work to do there. So we’re working on that.

Unidentified Analyst

This is [Matt Sharansky] on for John. Scott, while Epoxy has been down or operating at lower rates, have you made any structural changes such as operational or with your customer base? So when demand finally returns, Epoxy will look different than it has previously?

Scott Sutton

Yes. The answer is yes, but completely in process now. When I said we’re going to do more trough minimization footprint work, that’s something that we’re analyzing right now. So when demand does return yes, that business is going to look a little different. It’s going to be more focused on systems where we’ve had staying power even through these really sloppy recessionary conditions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}