The Urethane Blog

Everchem Updates

VOLUME XXI

September 14, 2023

Everchem’s exclusive Closers Only Club is reserved for only the highest caliber brass-baller salesmen in the chemical industry. Watch the hype video and be introduced to the top of the league: — read more

May 2, 2021

$70,000 For A Part-Time Driver

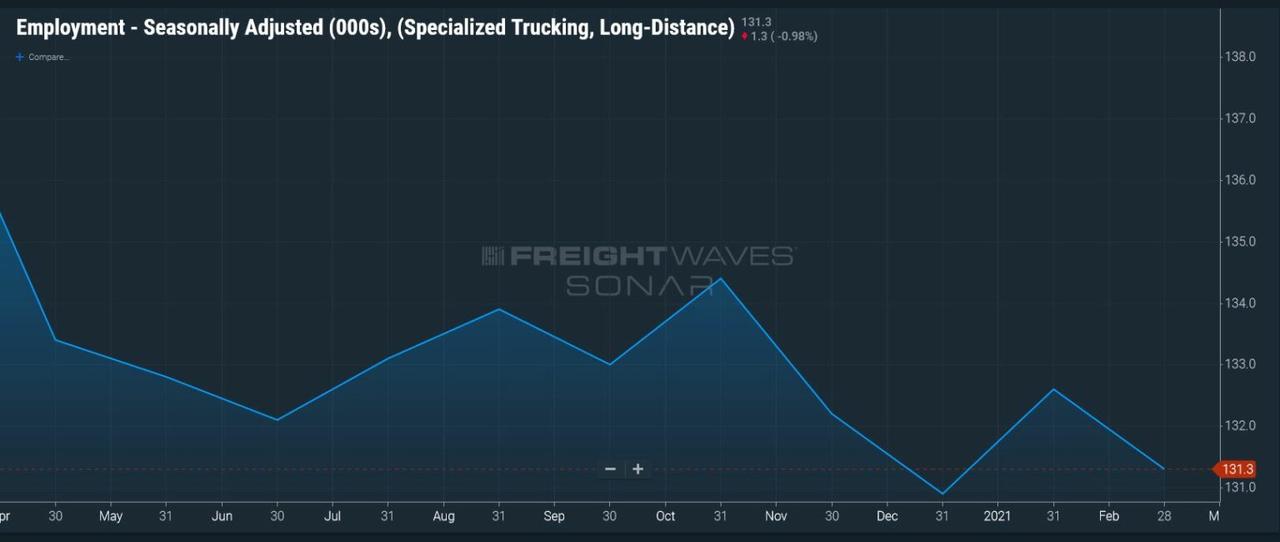

by Tyler DurdenSunday, May 02, 2021 – 05:00 PM

By John Kingston of Freightwaves,

David Parker is the CEO of Covenant Logisticsand he was blunt with analysts who follow the company on its earnings call Tuesday.

“How do we get enough drivers?” he said in response to a question from Stephens analyst Jack Atkins. “I don’t know.”

Parker then gave an overview of the situation facing Covenant, and by extension other companies, in trying to recruit drivers. One problem: With rates so high, companies are encountering the fact that a driver doesn’t need to work a full schedule to pull in a decent salary.

“We’re finding out that just to get a driver, let’s say the numbers are $85,000 (per year),” Parker said, according to a transcript of the earnings call supplied by SeekingAlpha. “But a lot of these drivers are happy at $70,000. Now they’re not coming to work for me, unless it’s in the ($80,000s), because they’re happy making $70,000.”

What’s happening, he said, is that drivers are looking at the fact that they can make $70,000 “and stay home a little more.”

The result is a tightening of capacity. Parker said utilization in the first quarter at Covenant was three or four percentage points less than it would have as a result of that development. “It’s an interesting dynamic that none of us have calculated,” he said.

To put the numbers in perspective, Todd Amen, the president of ATBS, which prepares taxes for mostly independent owner-operators, said in a recent interview with the FreightWaves Drilling Deep podcast that the average tax return his company prepared for drivers’ 2020 pay was $67,500. He also said his company prepared numerous 2020 returns with pay in excess of $100,000.

Parker was firm that this was not a situation likely to change soon. “There’s nothing out there that tells me that drivers are going to readily be available over the medium [term in] one to two years,” he said. “And that’s where I’m at.”

Paul Bunn, the company’s COO and senior executive vice president, echoed what other executives have said recently: Additional stimulus benefits are making the situation tighter. He said that while offering some hope that as the benefits roll off, “that might help a bit.”

But what the government giveth the government can sometimes taketh away. Bunn expressed another familiar sentiment in the industry today, that an infrastructure bill adding to demand for workers would create more difficulty to put drivers behind the wheel. Construction, Bunn said, is “a monster competitor of our industry” and if the bill is approved, “that’s going to be a big pull.”

Labor is going to be a “capacity constraint” through the economy, Bunn said, while conceding that trucking is not unique in that. And because of that labor squeeze, capacity in many fields is going to be limited. “The OEMs, the manufacturers are limited capacity,” Bunn said. “They’re not ramping up in a major, major way because of labor, because of commodity pricing, because of the costs.”

All that means is that capacity growth is going to be “reasonable,” Bunn said. “It’s not going to be crazy, people growing fleets [by] significant amounts.”

“It’s all you can do just to hold serve,” he added.

While the driver situation is tough, it didn’t notably hurt the first-quarter performance of Covenant. To open the call, Joey Hogan, Covenant’s co-president, highlighted some of the company’s first-quarter numbers: a 6% growth in operating revenue on a strategic reduction in the number of company tractors and the best first-quarter net income figure in its history.

Beyond the market for drivers, Parker said the freight market is “hot” and likely to stay that way.

“We are at 7%, 8% GDP growth, that goes to 5%, well, probably, or it could stay 7% or 8%,” he said. “But it’s still going to be numbers that you and I have never sensed or felt from a freight standpoint. And so I don’t see that letting up, I see that a solid couple of years of being in that kind of environment.”

Given that, Parker and other Covenant managers used the occasion of the earnings call to drive home with more detail a point the company made in its earnings statement a day earlier: It intends to get higher rates out of some of its Dedicated customers. While the company’s Expedited division saw its operating ratio improve to 91% from 102.3% a year earlier, the Dedicated division saw its OR remain above 100%.

The Dedicated division, Bunn said, has two types of customers. One is a group with high returns, “and we want more of those,” he said. “We’re going to go to the customers [where] we have that and say, ‘Can we have more of your business?’”

The other are customers that Bunn referred to as “commoditized.” Those customers are going to need to “value” the Dedicated service provides “or we’re going to give those trucks to somebody who’s in the first bucket.”

Trucks won’t just get “yanked” out, Bunn said. But “we’re not going to run Dedicated with a 98, 99 or 100 OR,” he added.

But even though Covenant, like other carriers, has leverage in negotiations given the tight market for capacity, it does need to be handled with a certain degree of aplomb, Hogan said. Hogan was talking about the company’s Expedited division when he said that in price negotiations, a company needs to be “respectful” as prices get up to “that line where they say, ‘Well, I’m going to grow my own [transportation].’”

Another possibility: rail. “When does the price push them to the rail?” he asked.

However, the Expedited division is “in a good spot for at least a couple of years,” Hogan said. That’s aided by the fact that inventories are “stupid low” across the supply chain, he added.

May 2, 2021

$70,000 For A Part-Time Driver

by Tyler DurdenSunday, May 02, 2021 – 05:00 PM

By John Kingston of Freightwaves,

David Parker is the CEO of Covenant Logisticsand he was blunt with analysts who follow the company on its earnings call Tuesday.

“How do we get enough drivers?” he said in response to a question from Stephens analyst Jack Atkins. “I don’t know.”

Parker then gave an overview of the situation facing Covenant, and by extension other companies, in trying to recruit drivers. One problem: With rates so high, companies are encountering the fact that a driver doesn’t need to work a full schedule to pull in a decent salary.

“We’re finding out that just to get a driver, let’s say the numbers are $85,000 (per year),” Parker said, according to a transcript of the earnings call supplied by SeekingAlpha. “But a lot of these drivers are happy at $70,000. Now they’re not coming to work for me, unless it’s in the ($80,000s), because they’re happy making $70,000.”

What’s happening, he said, is that drivers are looking at the fact that they can make $70,000 “and stay home a little more.”

The result is a tightening of capacity. Parker said utilization in the first quarter at Covenant was three or four percentage points less than it would have as a result of that development. “It’s an interesting dynamic that none of us have calculated,” he said.

To put the numbers in perspective, Todd Amen, the president of ATBS, which prepares taxes for mostly independent owner-operators, said in a recent interview with the FreightWaves Drilling Deep podcast that the average tax return his company prepared for drivers’ 2020 pay was $67,500. He also said his company prepared numerous 2020 returns with pay in excess of $100,000.

Parker was firm that this was not a situation likely to change soon. “There’s nothing out there that tells me that drivers are going to readily be available over the medium [term in] one to two years,” he said. “And that’s where I’m at.”

Paul Bunn, the company’s COO and senior executive vice president, echoed what other executives have said recently: Additional stimulus benefits are making the situation tighter. He said that while offering some hope that as the benefits roll off, “that might help a bit.”

But what the government giveth the government can sometimes taketh away. Bunn expressed another familiar sentiment in the industry today, that an infrastructure bill adding to demand for workers would create more difficulty to put drivers behind the wheel. Construction, Bunn said, is “a monster competitor of our industry” and if the bill is approved, “that’s going to be a big pull.”

Labor is going to be a “capacity constraint” through the economy, Bunn said, while conceding that trucking is not unique in that. And because of that labor squeeze, capacity in many fields is going to be limited. “The OEMs, the manufacturers are limited capacity,” Bunn said. “They’re not ramping up in a major, major way because of labor, because of commodity pricing, because of the costs.”

All that means is that capacity growth is going to be “reasonable,” Bunn said. “It’s not going to be crazy, people growing fleets [by] significant amounts.”

“It’s all you can do just to hold serve,” he added.

While the driver situation is tough, it didn’t notably hurt the first-quarter performance of Covenant. To open the call, Joey Hogan, Covenant’s co-president, highlighted some of the company’s first-quarter numbers: a 6% growth in operating revenue on a strategic reduction in the number of company tractors and the best first-quarter net income figure in its history.

Beyond the market for drivers, Parker said the freight market is “hot” and likely to stay that way.

“We are at 7%, 8% GDP growth, that goes to 5%, well, probably, or it could stay 7% or 8%,” he said. “But it’s still going to be numbers that you and I have never sensed or felt from a freight standpoint. And so I don’t see that letting up, I see that a solid couple of years of being in that kind of environment.”

Given that, Parker and other Covenant managers used the occasion of the earnings call to drive home with more detail a point the company made in its earnings statement a day earlier: It intends to get higher rates out of some of its Dedicated customers. While the company’s Expedited division saw its operating ratio improve to 91% from 102.3% a year earlier, the Dedicated division saw its OR remain above 100%.

The Dedicated division, Bunn said, has two types of customers. One is a group with high returns, “and we want more of those,” he said. “We’re going to go to the customers [where] we have that and say, ‘Can we have more of your business?’”

The other are customers that Bunn referred to as “commoditized.” Those customers are going to need to “value” the Dedicated service provides “or we’re going to give those trucks to somebody who’s in the first bucket.”

Trucks won’t just get “yanked” out, Bunn said. But “we’re not going to run Dedicated with a 98, 99 or 100 OR,” he added.

But even though Covenant, like other carriers, has leverage in negotiations given the tight market for capacity, it does need to be handled with a certain degree of aplomb, Hogan said. Hogan was talking about the company’s Expedited division when he said that in price negotiations, a company needs to be “respectful” as prices get up to “that line where they say, ‘Well, I’m going to grow my own [transportation].’”

Another possibility: rail. “When does the price push them to the rail?” he asked.

However, the Expedited division is “in a good spot for at least a couple of years,” Hogan said. That’s aided by the fact that inventories are “stupid low” across the supply chain, he added.

May 1, 2021

Huntsman posts $83 million profit for first quarter 2021

Marcy de Luna, Houston ChronicleApril 30, 2021Updated: April 30, 2021 11:47 a.m. Comments

Huntsman Corp. said Friday reported a profit for the first three months of 2021.

The Woodlands chemical-maker said it earned a first-quarter profit of $83 million, compared to a $705 million profit during the same period in 2020. Revenues rose 16 percent to $1.84 billion in the period from $1.59 billion in the first quarter of 2020.

President and CEO Peter Huntsman said in the Friday release that the company thrived, despite challenges from February’s winter storm, due to each of its business segments exceeding the company’s expectations as economic recovery accelerated through the quarter.

For example, revenue for the company’s polyurethanes segment rose 20 percent to $1.1 billion for the period compared to $888 million for the first quarter of 2020.

The increase was largely due to high selling prices for the chemical methylene diphenyl diisocyanate, which is used primarily in the production of rigid polyurethane foams used for insulation for homes and refrigerators. MDI average selling prices increased mostly in China and Europe, according to the release.

“Furthermore, the seasonal expected use of cash in the first quarter was less than anticipated due to the better than expected operating results and lower net working capital levels,” Huntsman said in the release. “Our balance sheet leverage and liquidity remain strong and gives us ample flexibility to continue to develop and expand our core businesses through both internal investments and acquisitions in line with our strategy. Because of our strong balance sheet and confidence in the consistent generation of solid free cash flow, I am pleased we can increase our quarterly dividend by 15%. The year has started off well and if current trends hold, we expect 2021 to be a very good year for the company.”

May 1, 2021

Huntsman posts $83 million profit for first quarter 2021

Marcy de Luna, Houston ChronicleApril 30, 2021Updated: April 30, 2021 11:47 a.m. Comments

Huntsman Corp. said Friday reported a profit for the first three months of 2021.

The Woodlands chemical-maker said it earned a first-quarter profit of $83 million, compared to a $705 million profit during the same period in 2020. Revenues rose 16 percent to $1.84 billion in the period from $1.59 billion in the first quarter of 2020.

President and CEO Peter Huntsman said in the Friday release that the company thrived, despite challenges from February’s winter storm, due to each of its business segments exceeding the company’s expectations as economic recovery accelerated through the quarter.

For example, revenue for the company’s polyurethanes segment rose 20 percent to $1.1 billion for the period compared to $888 million for the first quarter of 2020.

The increase was largely due to high selling prices for the chemical methylene diphenyl diisocyanate, which is used primarily in the production of rigid polyurethane foams used for insulation for homes and refrigerators. MDI average selling prices increased mostly in China and Europe, according to the release.

“Furthermore, the seasonal expected use of cash in the first quarter was less than anticipated due to the better than expected operating results and lower net working capital levels,” Huntsman said in the release. “Our balance sheet leverage and liquidity remain strong and gives us ample flexibility to continue to develop and expand our core businesses through both internal investments and acquisitions in line with our strategy. Because of our strong balance sheet and confidence in the consistent generation of solid free cash flow, I am pleased we can increase our quarterly dividend by 15%. The year has started off well and if current trends hold, we expect 2021 to be a very good year for the company.”

April 30, 2021

Tosoh to Increase Prices for Millionate MDI Grades

Tosoh Specialty Chemicals USA, Inc. is increasing its prices for Millionate MDI Grades in North

America. Effective May 1, 2021 or as contract terms allow, TSCU will increase the prices of Millionate

MDI grades by $0.35/kg.

Millionate MDI is widely used in the production of rigid, semi-rigid, and integral skin foams, as well as

coatings, adhesives and elastomers.