Current Affairs

August 5, 2022

BASF Warning

BASF may have to cut production due to low Rhine water levels- statement

Fri, August 5, 2022 at 6:53 AM·1 min read

BERLIN, Aug 5 (Reuters) – German chemicals giant BASF said it could not rule out needing to make cuts to production in the coming weeks due to low water levels on the Rhine river, one of the key logistics arteries for Europe’s largest economy.

“Currently, production is not affected by the low water,” the company said in an e-mailed statement on Friday. “But we cannot fully rule out reductions in output from certain plants in the coming weeks.”

Europe’s heatwave has had knock-on effects on levels in key transport waterways. The Rhine is one of the key channels linking Germany’s industrial heartlands with the North Sea ports from which their products are exported to world markets. (Reporting by Thomas Escritt; editing by Matthias Williams)

https://finance.yahoo.com/news/basf-may-cut-production-due-105314092.html

August 4, 2022

Diesel Primer

Sorry! Diesel prices are likely to climb again soon

Behind the scenes of why fuel is so expensive in 2022

Rachel PremackThursday, August 4, 2022 11 minutes read

Listen to this article 0:00 / 15:47 BeyondWords

For today’s MODES, I called up FreightWaves Editor-at-Large John Kingston to find out what the heck is happening with diesel prices recently. I learned a lot, but the most important takeaway was the World Oil Market Waterbed Theory.

This conversation was lightly edited and condensed for clarity.

FREIGHTWAVES: Just to start off pretty broad, the macro conditions are pretty much the same from what we saw earlier this year to what’s happening now. Obviously, we haven’t built any new refineries in the past few months. There’s still a war in Ukraine. Why is it that future prices are going down, and maybe not as quickly, but retail gasoline and diesel prices are also going down?

KINGSTON: “It’s a good question because it’s not really clear. I think part of the reason is that the news reports continue to trickle out about Russia doing relatively well in finding new buyers for its crude oil. Whereas, the International Energy Agency had predicted a couple of months ago that the loss of Russian supplies was going to be about 3 million barrels a day, which is roughly about 3% of the world market — which is a lot when you lose that much supply.

“I’m going to date myself with this reference, but it’s the best I can do. The world oil market is like a waterbed. If you push down one corner of the waterbed, the water moves throughout the entire mattress. If Russia is actually finding buyers for its oil that maybe had gone to Europe previously, but the oil is instead going to India or China, it’s the same as it getting out to its normal places. The world oil market is better supplied than it looked like it was going to be starting back around March or April. I think that’s very clearly a factor.”

Why diesel prices likely will rise again

KINGSTON: “When you look at what refineries are doing right now, they are running just full blast. One of the reasons, of course, is that the margins have been so strong. They are putting a lot of products onto the market, but let’s look forward a little bit, and I’m going to refer to the earnings call for Phillips 66.

“The executive vice president for marketing and commercial is a guy named Brian Mandell. He was talking about diesel and he said, ‘Yeah, it’s down, but let’s look at a couple of things. Global inventories are still extremely tight. It’s summer, which is not the heavy diesel season.’ But as he said, ‘We’re getting near harvest season, and harvest season is important for diesel consumption for obvious reasons, and then right after that is winter.’

“He’s cautious about the idea that we’ve got some great drop in diesel markets as a result of various factors.

“Now, the question becomes, as we move ahead, does the price of crude rise overall? Does diesel drag up crude? There are times in oil market history where that most certainly happened. Or does diesel just strengthen against crude?”

“Looking at a very basic spread of the first month of the Brent crude price versus the price of ultra-low sulfur diesel on the market, it got up as high as $1.64 per gallon on May 2. [Tuesday], it was down about 58 cents. It’s been trending consistently. Over the last two weeks, it’s been about in the 40-to-50 cents range. A year ago, the spread was 40 cents. OK, it’s starting back toward normalcy, but it’s still elevated and it’s coming off some amazingly high numbers.”

Europe’s natural gas crisis could mean a higher diesel prices in the U.S.

KINGSTON: “Going forward, as we go toward the winter, we really have to watch whether you’ll see crude go up on its own. Will diesel drag up crude with it? Or will diesel just move higher than crude?

“The world of diesel needs to look very closely at what happens with the whole Russian natural gas situation. When you don’t have enough natural gas, you inevitably turn to diesel or some kind of distillate as a substitute, whether it is for an industrial process [or] whether it’s to generate electricity, diesel can be a substitute for natural gas.

“If the Russians really put the squeeze on Europe with natural gas, you’ll probably see buyers turn to distillate, whether it’s a pure diesel or some other distillate product, in its place. That’s very concerning. Obviously, there’s always a risk of a gas-for-oil substitution or oil-for-gas substitution, but it’s really high now, really strong.”

FREIGHTWAVES: What would that substitution do to the price of diesel, for example?

KINGSTON: “If you’ve got demand for energy out there that’s right now satisfied by natural gas, and instead that’s not available and they turn to diesel, that’s a new source of demand for diesel.”

FREIGHTWAVES: Diesel obviously has come down in price quite a bit in the past few weeks, but you don’t seem quite so certain that we’re out of the woods quite yet.

KINGSTON: “No. Really the reason I say that is primarily because of inventories. They’re so low.”

Here’s how to determine diesel prices on the futures market, if that’s something you were hoping to do

KINGSTON: “There’s no one price of diesel on the futures market. There’s a price now for September. There’s a price for October. There’s a price for September 2023. It goes out several years, and that spread is not a prediction of where the price is going to be. It is a complex mix, a complex brew of inventories and interest rates. A market that is in perfect balance, the kind of thing they teach you in econ 101, that a market will rise over time.

“The September commodity is X. In that perfectly balanced market, October will be X plus something. That something is a function really of the cost of storage and the cost of money, the time value of money.

“When markets get very, very tight, like they are now, the market shifts into a structure known as ‘backwardation.’ In backwardation, it’s X for the first month, X minus something for the next month, X minus something even more for the next month after that. The reason is because with supply short, you absolutely want the front-month barrel. You want the most immediate supply right now.

“The diesel market is in eye-popping backwardation right now. It’s not quite as crazy as it was. The highest number I’ve got here was $1.19 for the 12-month backwardation, meaning the front month versus 12 months out. I’ve got one number that got out to $2.14. I mean, it’s just nuts. Right now, it’s about 50 cents. A year ago on Aug. 3, the 12-month curve was 7 cents.”

FREIGHTWAVES: These are some crazy numbers, for sure.

KINGSTON: “It wasn’t backwardation. The market’s been a little tight for a while, but if you go back to as recently as April of last year, the market was in the structure known as ‘contango.’ That’s what I talked about before, where the price goes up every month, and that’s usually a sign of a fairly well-supplied market. This really steep backwardation in the market, yes, it continues to have me concerned because the market doesn’t.”

How to turn crude into diesel (a new hobby?)

FREIGHTWAVES: How does the diesel refining world compare to the tightness we’ve been seeing on the gasoline refining side? And as a secondary question to that, is there a certain type of crude that refineries prefer when it comes to refining diesel versus refining gasoline?

KINGSTON: “Every grade of crude performs differently in a refinery. For a real refinery, their model will show that crude type X will yield, in their particular refinery, a small percentage of LPGs (liquefied petroleum gases), like butane and propane, a small percentage of naphtha and a small percentage of intermediate products that we don’t really recognize. They know exactly what type of crudes will do particularly well to make diesel or to make gasoline.

“If the market’s right, they’ll look to make heavy fuel oil. They’ve tended not to try to do that in recent years, but they will try to maximize their output. They can’t do it precisely. It’s not like you can plug in numbers and say, ‘OK, I’d like to get 35.1% diesel out of this crude oil.

“The fact of the matter is, it’s tough for any crude to yield more than 40% diesel. That’s your maximum.

“As the world looks to consume more diesel, relative to gasoline, if that is in fact the way we’re going, that’s a problem. You cannot stand in front of a refinery and demand that it produce nothing but diesel because we don’t want gasoline right now. You’re always going to get some.

“This imprecision is why we import and export products because some refineries have more diesel than their system needs. Some refineries have more gasoline. Some markets need more diesel than their local refiners produce, so it’s easier to import it rather than to bring it into the U.S. [or] rather than to bring it from somewhere else in the U.S. Refineries are amazingly complex products, but they are not perfect. They’re only so precise.You do get these imbalances, and the imbalances can only really be met by importing or exporting.”

Truck stops have seen unprecedented profits from high diesel prices — but it’s not as sinister as it may appear

FREIGHTWAVES: I want to talk a little bit more about what you mentioned before I turned on the recorder about this idea that truck stops are making so much money right now, so much profit off of diesel and the fact that retail diesel prices have been so much higher than wholesale. Why is it that the decline in diesel prices haven’t been keeping up with wholesale prices? A skeptical reader is going to see that and think, “OK, these truck stops are just trying to profit off of us.” What’s going on behind the scenes?

KINGSTON: “The way the market works is that there’s futures trading. It builds up in four steps. I’m going to oversimplify here.

“There’s future trading, A, and then B, there is physical trading in individual markets (such as the Gulf Coast, the Atlantic Coast and New York Harbor). It might be traded as, in the Gulf Coast, ULSD minus 3 cents one day, then minus three and a half cents the next day, whatever.

“Then, those spot market prices are used as the basis for setting wholesale prices. Wholesale prices serve as the basis for what the retailers pay.

“Then, there’s the retail prices, which are set by the individual station owner, not the oil companies. When the market shoots up rapidly, as it has done, obviously, over the past several months, the wholesale prices shoot up with it. Wholesale will track futures prices pretty closely. Not necessarily one for one but pretty close to one to one.

“When those prices shoot up, it’s difficult for the retailers to keep up. They’re a little nervous about going up all the way, because what if the guy across the street, maybe he’s not going to go up all the way and then I’m going to lose business. It’s real street combat.

“Similarly, when the prices are up there and the wholesale numbers start coming down rapidly, as they’ve done now for really a month, they’re going to hold on to those prices as long as they can. Now, as soon as the guy across the street says, ‘I think I can grab some market share. I got a new, cheaper load from my supplier, and I think I can grab some market share from that jerk across the street by lowering my prices and then I’ll get more people who are going to come into my convenience store and buy beef jerky and all this other stuff,’ then the guy across the street has to go too. He has to move too.

“It’s always going to be slower because it’s probably just a natural economic resistance to lowering your price.

One international shipping regulation is quietlypushing up diesel prices

KINGSTON: “In 2019, in the oil market and at FreightWaves, we were writing quite a bit about IMO 2020. IMO 2020 is the worldwide regulation that went into effect that required all ships to burn fuel with no more than 0.5% sulfur. This was significantly restrictive.

“One of the ways that the marine fuel market was going to get there was to produce a new product called very-low-sulfur fuel oil, VLSFO. That’s a product that really didn’t exist before. “The way that they were going to make it is that they were going to use a lot of something called vacuum gas oil. Vacuum gas oil is an intermediate product that comes off the crude tower, which is the first thing you do in a refinery. You throw crude into the crude tower, you get all these intermediate products and then you further process them into final products.

“The problem is that vacuum gas oil tends to go into making diesel. The fear was always that you were going to divert VGO into making marine VLSFO. This is a whole new source of demand. You were going to tighten up the diesel market in the process.

“There were some signs in the fall of 2019 that maybe the diesel market was starting to tighten up. There was a view out there that maybe this was the early signs of IMO 2020. IMO 2020 goes into effect on Jan. 1, 2020. By March 1, the world’s in a full-blown pandemic. Demand craters, and the test of the theories of the diesel market tightening because of IMO 2020 never really got tested because demand had collapsed.

“Now, of course, demand has come roaring back, and there are some views out there that one of the reasons you’re seeing such strength in the diesel market is because of IMO 2020. It just didn’t announce itself on a single day the way it’s supposed to do the first time.”

FREIGHTWAVES: That’s a potential under-the-radar driver of the tightness in diesel right now, it seems.

KINGSTON: “I mean, let’s just say that it wasn’t under the radar in 2019. Everybody talked about it.”

Diesel inventory remains low, and scheduled refinery “turnarounds” won’t help boost stores

FREIGHTWAVES: What will it take to restock diesel inventories?

KINGSTON: “It’s hard to say because refineries have been running on full blast now for a while. Just in the U.S. over the last four weeks, the utilization has been between 94.5% and 95%, which is a really healthy number. It’s dropped a little bit since then.

“We’re coming up to what’s known as turnaround season, where you have regularly scheduled maintenance. They have turnarounds in September and October to get ready for winter and then they do turnarounds. They don’t turnaround every refinery, but then there’ll be turnarounds, let’s say, in March and April getting ready for summer.

| Year | Refined fuel stocks in the US, end of July (thousand barrels) |

|---|---|

| 2017 | 149,414 |

| 2018 | 124,193 |

| 2019 | 135,922 |

| 2020 | 179,977 |

| 2021 | 138,744 |

| Five-year average | 145,650 |

| 2022 | 109,324 |

We have unusually low stocks of refined fuel. (Source: U.S. Energy Information Administration)

“We were at 95% on the week of June 24. We’re down to 92.2%. We’re getting toward the fall, where it’s inevitably going to slide.

“The refining margins are not as great as they were a few weeks ago. They’re still healthy, but they’re not as good. That creates a little less incentive to produce a lot of product. Inventories can turn around relatively quickly with a change in conditions, but you’d have to have a lot of new supply, margins that really incentivize price, and a drop in demand. Otherwise, it’s going to take a little while to get inventory back, and I still think that’s going to be the primary driving factor in price.”

Goodbye gasoline, long live diesel!

FREIGHTWAVES: I’ve got one more big-picture, long-term question. We’re seeing an increasing adoption of passenger cars. Obviously, finding an electric tractor-trailer is not quite as seamless as buying a Chevy Bolt or a Tesla. Do you think that in the next 10 to 20 years that diesel demand will be more resilient than gasoline demand — or is this an oversimplification?

KINGSTON: “I think you’re right. I think that most refiners are probably looking at the idea that their diesel demand will stay a little more stable. It’s probably less subject to disruption. I think that’s very legitimate. I think that’s in the long-term calculations of a lot of companies – no doubt about it.”

August 4, 2022

Diesel Primer

Sorry! Diesel prices are likely to climb again soon

Behind the scenes of why fuel is so expensive in 2022

Rachel PremackThursday, August 4, 2022 11 minutes read

Listen to this article 0:00 / 15:47 BeyondWords

For today’s MODES, I called up FreightWaves Editor-at-Large John Kingston to find out what the heck is happening with diesel prices recently. I learned a lot, but the most important takeaway was the World Oil Market Waterbed Theory.

This conversation was lightly edited and condensed for clarity.

FREIGHTWAVES: Just to start off pretty broad, the macro conditions are pretty much the same from what we saw earlier this year to what’s happening now. Obviously, we haven’t built any new refineries in the past few months. There’s still a war in Ukraine. Why is it that future prices are going down, and maybe not as quickly, but retail gasoline and diesel prices are also going down?

KINGSTON: “It’s a good question because it’s not really clear. I think part of the reason is that the news reports continue to trickle out about Russia doing relatively well in finding new buyers for its crude oil. Whereas, the International Energy Agency had predicted a couple of months ago that the loss of Russian supplies was going to be about 3 million barrels a day, which is roughly about 3% of the world market — which is a lot when you lose that much supply.

“I’m going to date myself with this reference, but it’s the best I can do. The world oil market is like a waterbed. If you push down one corner of the waterbed, the water moves throughout the entire mattress. If Russia is actually finding buyers for its oil that maybe had gone to Europe previously, but the oil is instead going to India or China, it’s the same as it getting out to its normal places. The world oil market is better supplied than it looked like it was going to be starting back around March or April. I think that’s very clearly a factor.”

Why diesel prices likely will rise again

KINGSTON: “When you look at what refineries are doing right now, they are running just full blast. One of the reasons, of course, is that the margins have been so strong. They are putting a lot of products onto the market, but let’s look forward a little bit, and I’m going to refer to the earnings call for Phillips 66.

“The executive vice president for marketing and commercial is a guy named Brian Mandell. He was talking about diesel and he said, ‘Yeah, it’s down, but let’s look at a couple of things. Global inventories are still extremely tight. It’s summer, which is not the heavy diesel season.’ But as he said, ‘We’re getting near harvest season, and harvest season is important for diesel consumption for obvious reasons, and then right after that is winter.’

“He’s cautious about the idea that we’ve got some great drop in diesel markets as a result of various factors.

“Now, the question becomes, as we move ahead, does the price of crude rise overall? Does diesel drag up crude? There are times in oil market history where that most certainly happened. Or does diesel just strengthen against crude?”

“Looking at a very basic spread of the first month of the Brent crude price versus the price of ultra-low sulfur diesel on the market, it got up as high as $1.64 per gallon on May 2. [Tuesday], it was down about 58 cents. It’s been trending consistently. Over the last two weeks, it’s been about in the 40-to-50 cents range. A year ago, the spread was 40 cents. OK, it’s starting back toward normalcy, but it’s still elevated and it’s coming off some amazingly high numbers.”

Europe’s natural gas crisis could mean a higher diesel prices in the U.S.

KINGSTON: “Going forward, as we go toward the winter, we really have to watch whether you’ll see crude go up on its own. Will diesel drag up crude with it? Or will diesel just move higher than crude?

“The world of diesel needs to look very closely at what happens with the whole Russian natural gas situation. When you don’t have enough natural gas, you inevitably turn to diesel or some kind of distillate as a substitute, whether it is for an industrial process [or] whether it’s to generate electricity, diesel can be a substitute for natural gas.

“If the Russians really put the squeeze on Europe with natural gas, you’ll probably see buyers turn to distillate, whether it’s a pure diesel or some other distillate product, in its place. That’s very concerning. Obviously, there’s always a risk of a gas-for-oil substitution or oil-for-gas substitution, but it’s really high now, really strong.”

FREIGHTWAVES: What would that substitution do to the price of diesel, for example?

KINGSTON: “If you’ve got demand for energy out there that’s right now satisfied by natural gas, and instead that’s not available and they turn to diesel, that’s a new source of demand for diesel.”

FREIGHTWAVES: Diesel obviously has come down in price quite a bit in the past few weeks, but you don’t seem quite so certain that we’re out of the woods quite yet.

KINGSTON: “No. Really the reason I say that is primarily because of inventories. They’re so low.”

Here’s how to determine diesel prices on the futures market, if that’s something you were hoping to do

KINGSTON: “There’s no one price of diesel on the futures market. There’s a price now for September. There’s a price for October. There’s a price for September 2023. It goes out several years, and that spread is not a prediction of where the price is going to be. It is a complex mix, a complex brew of inventories and interest rates. A market that is in perfect balance, the kind of thing they teach you in econ 101, that a market will rise over time.

“The September commodity is X. In that perfectly balanced market, October will be X plus something. That something is a function really of the cost of storage and the cost of money, the time value of money.

“When markets get very, very tight, like they are now, the market shifts into a structure known as ‘backwardation.’ In backwardation, it’s X for the first month, X minus something for the next month, X minus something even more for the next month after that. The reason is because with supply short, you absolutely want the front-month barrel. You want the most immediate supply right now.

“The diesel market is in eye-popping backwardation right now. It’s not quite as crazy as it was. The highest number I’ve got here was $1.19 for the 12-month backwardation, meaning the front month versus 12 months out. I’ve got one number that got out to $2.14. I mean, it’s just nuts. Right now, it’s about 50 cents. A year ago on Aug. 3, the 12-month curve was 7 cents.”

FREIGHTWAVES: These are some crazy numbers, for sure.

KINGSTON: “It wasn’t backwardation. The market’s been a little tight for a while, but if you go back to as recently as April of last year, the market was in the structure known as ‘contango.’ That’s what I talked about before, where the price goes up every month, and that’s usually a sign of a fairly well-supplied market. This really steep backwardation in the market, yes, it continues to have me concerned because the market doesn’t.”

How to turn crude into diesel (a new hobby?)

FREIGHTWAVES: How does the diesel refining world compare to the tightness we’ve been seeing on the gasoline refining side? And as a secondary question to that, is there a certain type of crude that refineries prefer when it comes to refining diesel versus refining gasoline?

KINGSTON: “Every grade of crude performs differently in a refinery. For a real refinery, their model will show that crude type X will yield, in their particular refinery, a small percentage of LPGs (liquefied petroleum gases), like butane and propane, a small percentage of naphtha and a small percentage of intermediate products that we don’t really recognize. They know exactly what type of crudes will do particularly well to make diesel or to make gasoline.

“If the market’s right, they’ll look to make heavy fuel oil. They’ve tended not to try to do that in recent years, but they will try to maximize their output. They can’t do it precisely. It’s not like you can plug in numbers and say, ‘OK, I’d like to get 35.1% diesel out of this crude oil.

“The fact of the matter is, it’s tough for any crude to yield more than 40% diesel. That’s your maximum.

“As the world looks to consume more diesel, relative to gasoline, if that is in fact the way we’re going, that’s a problem. You cannot stand in front of a refinery and demand that it produce nothing but diesel because we don’t want gasoline right now. You’re always going to get some.

“This imprecision is why we import and export products because some refineries have more diesel than their system needs. Some refineries have more gasoline. Some markets need more diesel than their local refiners produce, so it’s easier to import it rather than to bring it into the U.S. [or] rather than to bring it from somewhere else in the U.S. Refineries are amazingly complex products, but they are not perfect. They’re only so precise.You do get these imbalances, and the imbalances can only really be met by importing or exporting.”

Truck stops have seen unprecedented profits from high diesel prices — but it’s not as sinister as it may appear

FREIGHTWAVES: I want to talk a little bit more about what you mentioned before I turned on the recorder about this idea that truck stops are making so much money right now, so much profit off of diesel and the fact that retail diesel prices have been so much higher than wholesale. Why is it that the decline in diesel prices haven’t been keeping up with wholesale prices? A skeptical reader is going to see that and think, “OK, these truck stops are just trying to profit off of us.” What’s going on behind the scenes?

KINGSTON: “The way the market works is that there’s futures trading. It builds up in four steps. I’m going to oversimplify here.

“There’s future trading, A, and then B, there is physical trading in individual markets (such as the Gulf Coast, the Atlantic Coast and New York Harbor). It might be traded as, in the Gulf Coast, ULSD minus 3 cents one day, then minus three and a half cents the next day, whatever.

“Then, those spot market prices are used as the basis for setting wholesale prices. Wholesale prices serve as the basis for what the retailers pay.

“Then, there’s the retail prices, which are set by the individual station owner, not the oil companies. When the market shoots up rapidly, as it has done, obviously, over the past several months, the wholesale prices shoot up with it. Wholesale will track futures prices pretty closely. Not necessarily one for one but pretty close to one to one.

“When those prices shoot up, it’s difficult for the retailers to keep up. They’re a little nervous about going up all the way, because what if the guy across the street, maybe he’s not going to go up all the way and then I’m going to lose business. It’s real street combat.

“Similarly, when the prices are up there and the wholesale numbers start coming down rapidly, as they’ve done now for really a month, they’re going to hold on to those prices as long as they can. Now, as soon as the guy across the street says, ‘I think I can grab some market share. I got a new, cheaper load from my supplier, and I think I can grab some market share from that jerk across the street by lowering my prices and then I’ll get more people who are going to come into my convenience store and buy beef jerky and all this other stuff,’ then the guy across the street has to go too. He has to move too.

“It’s always going to be slower because it’s probably just a natural economic resistance to lowering your price.

One international shipping regulation is quietlypushing up diesel prices

KINGSTON: “In 2019, in the oil market and at FreightWaves, we were writing quite a bit about IMO 2020. IMO 2020 is the worldwide regulation that went into effect that required all ships to burn fuel with no more than 0.5% sulfur. This was significantly restrictive.

“One of the ways that the marine fuel market was going to get there was to produce a new product called very-low-sulfur fuel oil, VLSFO. That’s a product that really didn’t exist before. “The way that they were going to make it is that they were going to use a lot of something called vacuum gas oil. Vacuum gas oil is an intermediate product that comes off the crude tower, which is the first thing you do in a refinery. You throw crude into the crude tower, you get all these intermediate products and then you further process them into final products.

“The problem is that vacuum gas oil tends to go into making diesel. The fear was always that you were going to divert VGO into making marine VLSFO. This is a whole new source of demand. You were going to tighten up the diesel market in the process.

“There were some signs in the fall of 2019 that maybe the diesel market was starting to tighten up. There was a view out there that maybe this was the early signs of IMO 2020. IMO 2020 goes into effect on Jan. 1, 2020. By March 1, the world’s in a full-blown pandemic. Demand craters, and the test of the theories of the diesel market tightening because of IMO 2020 never really got tested because demand had collapsed.

“Now, of course, demand has come roaring back, and there are some views out there that one of the reasons you’re seeing such strength in the diesel market is because of IMO 2020. It just didn’t announce itself on a single day the way it’s supposed to do the first time.”

FREIGHTWAVES: That’s a potential under-the-radar driver of the tightness in diesel right now, it seems.

KINGSTON: “I mean, let’s just say that it wasn’t under the radar in 2019. Everybody talked about it.”

Diesel inventory remains low, and scheduled refinery “turnarounds” won’t help boost stores

FREIGHTWAVES: What will it take to restock diesel inventories?

KINGSTON: “It’s hard to say because refineries have been running on full blast now for a while. Just in the U.S. over the last four weeks, the utilization has been between 94.5% and 95%, which is a really healthy number. It’s dropped a little bit since then.

“We’re coming up to what’s known as turnaround season, where you have regularly scheduled maintenance. They have turnarounds in September and October to get ready for winter and then they do turnarounds. They don’t turnaround every refinery, but then there’ll be turnarounds, let’s say, in March and April getting ready for summer.

| Year | Refined fuel stocks in the US, end of July (thousand barrels) |

|---|---|

| 2017 | 149,414 |

| 2018 | 124,193 |

| 2019 | 135,922 |

| 2020 | 179,977 |

| 2021 | 138,744 |

| Five-year average | 145,650 |

| 2022 | 109,324 |

We have unusually low stocks of refined fuel. (Source: U.S. Energy Information Administration)

“We were at 95% on the week of June 24. We’re down to 92.2%. We’re getting toward the fall, where it’s inevitably going to slide.

“The refining margins are not as great as they were a few weeks ago. They’re still healthy, but they’re not as good. That creates a little less incentive to produce a lot of product. Inventories can turn around relatively quickly with a change in conditions, but you’d have to have a lot of new supply, margins that really incentivize price, and a drop in demand. Otherwise, it’s going to take a little while to get inventory back, and I still think that’s going to be the primary driving factor in price.”

Goodbye gasoline, long live diesel!

FREIGHTWAVES: I’ve got one more big-picture, long-term question. We’re seeing an increasing adoption of passenger cars. Obviously, finding an electric tractor-trailer is not quite as seamless as buying a Chevy Bolt or a Tesla. Do you think that in the next 10 to 20 years that diesel demand will be more resilient than gasoline demand — or is this an oversimplification?

KINGSTON: “I think you’re right. I think that most refiners are probably looking at the idea that their diesel demand will stay a little more stable. It’s probably less subject to disruption. I think that’s very legitimate. I think that’s in the long-term calculations of a lot of companies – no doubt about it.”

August 2, 2022

Contract Truck Rates Expected to Fall

Contract truckload rates will likely soften in the coming months

Spot rates indicate a strong dip for contracts is imminent

Zach Strickland, FW Market Expert & Market Analyst Follow on Twitter Saturday, July 30, 2022 3 minutes read Listen to this article 0:00 / 4:56 BeyondWords

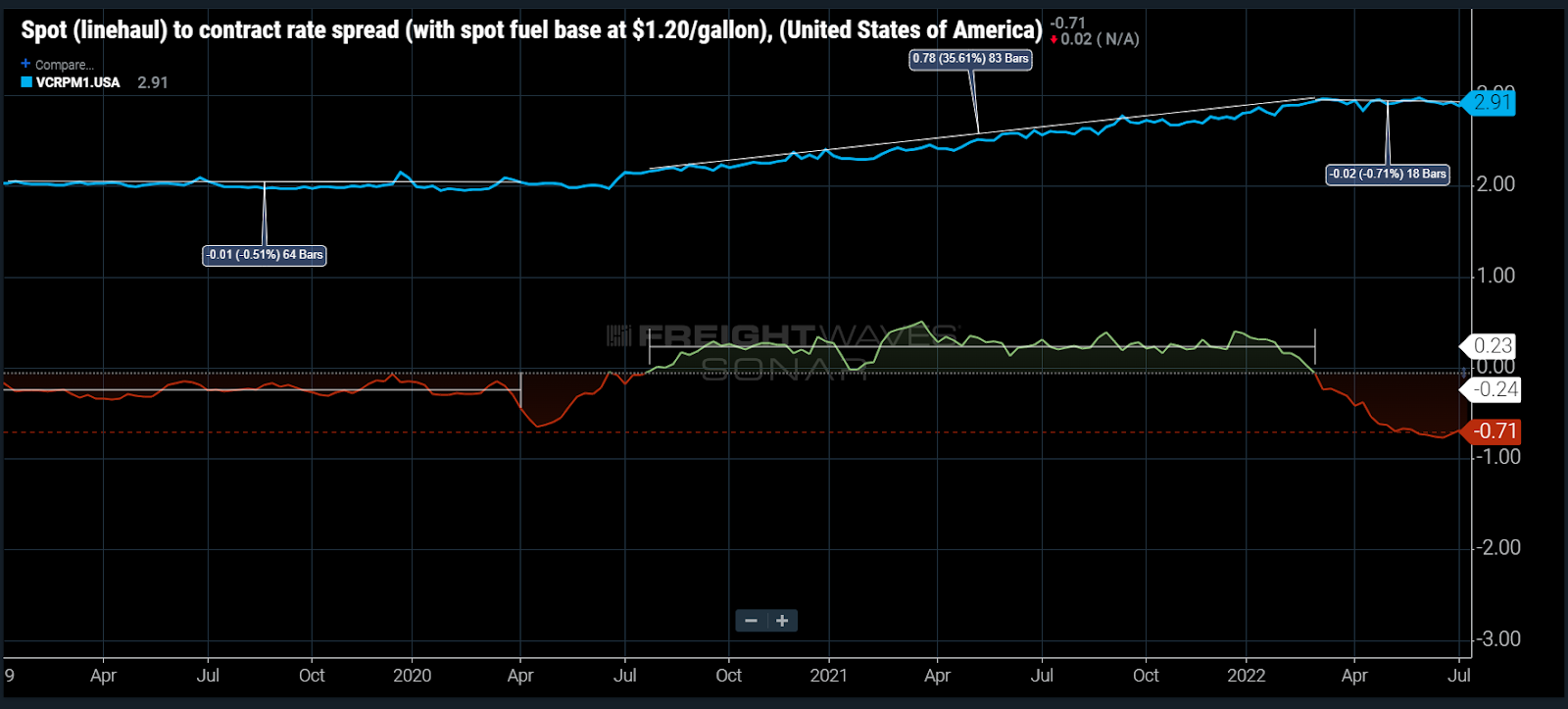

Van rates on the truckload contract market will likely soften in the coming months. But, the decline won’t be as marked as what the industry saw on the spot market side.

The spread between spot and contract rates has averaged around record low levels (~-74 cents a mile) since early May. That will put downward pressure on contract rates for bids negotiated in the second half of the year. There is little precedent for such a dramatic difference, but there’s also little evidence historically that contract rates will fall as fast as they increase.

The contract truckload market behaves very differently from the spot market. Volatility is the main difference. That’s driven primarily by the way pricing is negotiated.

The RATES12 index used in this week’s chart is the difference between spot rates less a level of estimated cost of fuel and contract rates. This is done for a more apples-to-apples comparison of the two rates, as contract rates include a portion of fuel cost and pass a lot of it along in the form of a fuel surcharge. This mechanism is largely absent from spot rates.

Contract truckload rates have barely budged since March, but red flags are already appearing

The contract or published rate market is simply an agreement between shipper and carrier that is in place for an extended period of time. The commitment is somewhat tenuous as neither volume nor service is guaranteed in most instances.

The only binding portion is, if the shipper tenders a load(s) to the carrier and the carrier is willing and able to transport the customer’s freight, it will do it for a predetermined price until the expiration of the agreement. Spot rates are negotiated on the spot and are normally only applicable for a few days with minimal volume.

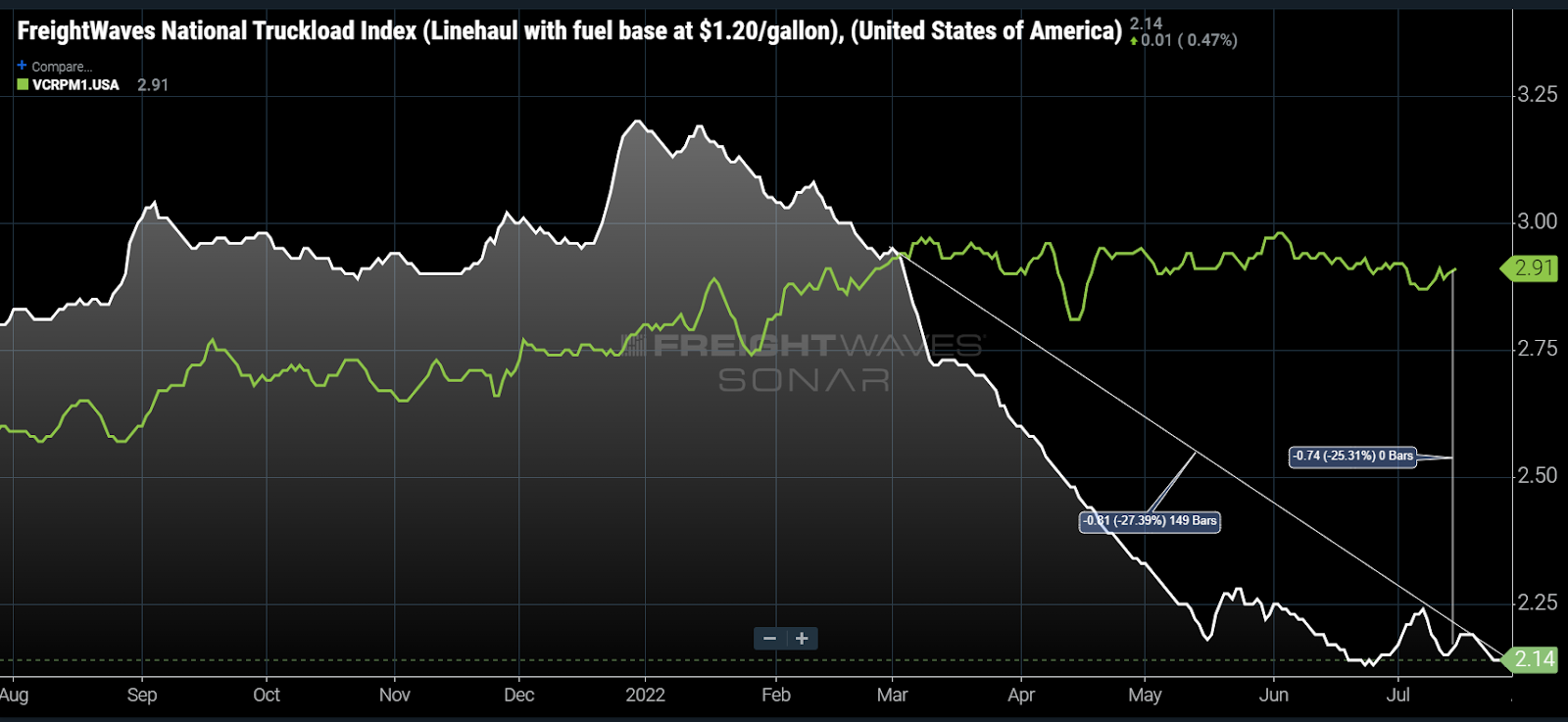

Contract rate agreements typically have a life span of around 12 months but can be longer or shorter. Many shippers transitioned to a shorter procurement cycle during the pandemic thanks to their inability to secure capacity reliably, essentially bidding against one another and driving up rates faster than ever. Contract rates increased ~49% from June 2020 to March 2022.

Since March, there has been minimal movement in contract rates, but they are showing early signs of deterioration, falling about 2% since early June. Spot rates, assuming a base level of fuel cost around $1.20 per gallon, have dropped 27% over the same period. This has created a 74-cent-per-mile difference between the spot (NTIL12) and contract rate (VCRPM1) indices.

In 2019 the spread between spot and contract averaged -24 cents per mile. Contract rates barely moved before falling about 2%-4% in January 2020, which shows that contract rates are less volatile.

The spread today is three times larger than it was in 2019. Shippers may have a stronger appetite for cost reduction after two years of rapid inflation.

A rate decrease will occur if demand-side conditions do not improve

Movements for contract truckload rates will ultimately be decided by the carriers and their need for equipment utilization. And so far, most publicly traded trucking companies have only mentioned minor deterioration at most while reporting strong Q2 results.

Accepted contract load volumes support this for now, showing only a marginal decline in July versus June. Compared to last July, volumes are down 3%-5%.

As for the supply side of the equation, most of the capacity growth over the past two years has been on the small fleet/owner-operator side, which heavily relies on spot market freight. The larger fleet heavy contract market has better structure to maintain elevated rate levels.

That said, the rate differential is too large to sustain for long. Some level of rate decrease will occur if demand-side conditions remain at or below current levels. Judging from history, it would appear a conservatively estimated 3%-5% decrease is all but imminent in the coming months.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new datasets each week and enhancing the client experience.

August 2, 2022

Contract Truck Rates Expected to Fall

Contract truckload rates will likely soften in the coming months

Spot rates indicate a strong dip for contracts is imminent

Zach Strickland, FW Market Expert & Market Analyst Follow on Twitter Saturday, July 30, 2022 3 minutes read Listen to this article 0:00 / 4:56 BeyondWords

Van rates on the truckload contract market will likely soften in the coming months. But, the decline won’t be as marked as what the industry saw on the spot market side.

The spread between spot and contract rates has averaged around record low levels (~-74 cents a mile) since early May. That will put downward pressure on contract rates for bids negotiated in the second half of the year. There is little precedent for such a dramatic difference, but there’s also little evidence historically that contract rates will fall as fast as they increase.

The contract truckload market behaves very differently from the spot market. Volatility is the main difference. That’s driven primarily by the way pricing is negotiated.

The RATES12 index used in this week’s chart is the difference between spot rates less a level of estimated cost of fuel and contract rates. This is done for a more apples-to-apples comparison of the two rates, as contract rates include a portion of fuel cost and pass a lot of it along in the form of a fuel surcharge. This mechanism is largely absent from spot rates.

Contract truckload rates have barely budged since March, but red flags are already appearing

The contract or published rate market is simply an agreement between shipper and carrier that is in place for an extended period of time. The commitment is somewhat tenuous as neither volume nor service is guaranteed in most instances.

The only binding portion is, if the shipper tenders a load(s) to the carrier and the carrier is willing and able to transport the customer’s freight, it will do it for a predetermined price until the expiration of the agreement. Spot rates are negotiated on the spot and are normally only applicable for a few days with minimal volume.

Contract rate agreements typically have a life span of around 12 months but can be longer or shorter. Many shippers transitioned to a shorter procurement cycle during the pandemic thanks to their inability to secure capacity reliably, essentially bidding against one another and driving up rates faster than ever. Contract rates increased ~49% from June 2020 to March 2022.

Since March, there has been minimal movement in contract rates, but they are showing early signs of deterioration, falling about 2% since early June. Spot rates, assuming a base level of fuel cost around $1.20 per gallon, have dropped 27% over the same period. This has created a 74-cent-per-mile difference between the spot (NTIL12) and contract rate (VCRPM1) indices.

In 2019 the spread between spot and contract averaged -24 cents per mile. Contract rates barely moved before falling about 2%-4% in January 2020, which shows that contract rates are less volatile.

The spread today is three times larger than it was in 2019. Shippers may have a stronger appetite for cost reduction after two years of rapid inflation.

A rate decrease will occur if demand-side conditions do not improve

Movements for contract truckload rates will ultimately be decided by the carriers and their need for equipment utilization. And so far, most publicly traded trucking companies have only mentioned minor deterioration at most while reporting strong Q2 results.

Accepted contract load volumes support this for now, showing only a marginal decline in July versus June. Compared to last July, volumes are down 3%-5%.

As for the supply side of the equation, most of the capacity growth over the past two years has been on the small fleet/owner-operator side, which heavily relies on spot market freight. The larger fleet heavy contract market has better structure to maintain elevated rate levels.

That said, the rate differential is too large to sustain for long. Some level of rate decrease will occur if demand-side conditions remain at or below current levels. Judging from history, it would appear a conservatively estimated 3%-5% decrease is all but imminent in the coming months.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new datasets each week and enhancing the client experience.