The Urethane Blog

Everchem Updates

VOLUME XXI

September 14, 2023

Everchem’s exclusive Closers Only Club is reserved for only the highest caliber brass-baller salesmen in the chemical industry. Watch the hype video and be introduced to the top of the league: — read more

February 27, 2023

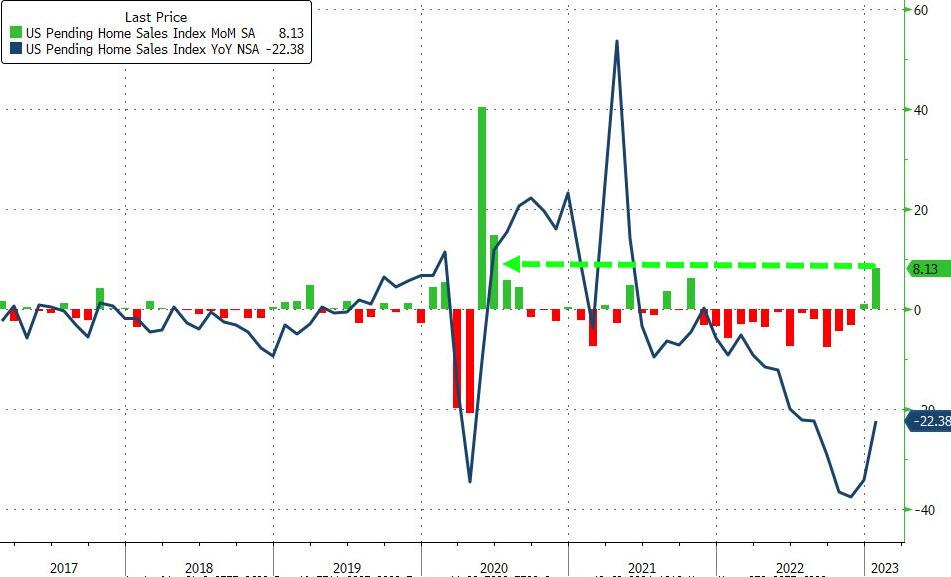

US Pending Home Sales Explode Higher In January

by Tyler Durden

Monday, Feb 27, 2023 – 10:07 AM

Existing home sales plunged, new home sales surged… so today’s pending home sales print will be the decider over what level of bloodbathery is really occurring in the US housing market. After a surprise jump in December (after 6 straight declining months), analysts expected a modest 1.0% MoM jump in pending home sales in January but were blown away by an 8.1% MoM explosion in sales (though Dec was revised down from +2.5% to +1.1%)….

{kind=link}

Source: Bloomberg

“Home sales activity looks to be bottoming out in the first quarter of this year, before incremental improvements will occur,” Lawrence Yun, NAR’s chief economist, said in a statement.

That is the biggest MoM jump since June 2020, pushing the index to its highest since August 2022…

{kind=link}

Source: Bloomberg

“Buyers responded to better affordability from falling mortgage rates in December and January,” said NAR Chief Economist Lawrence Yun.

Sorry Larry… that’s history!

{kind=link}

This surge in pending sales is unlikely to continue since mortgage rates have surged since the period these sales were ‘pending’ for.

We also note that while housing futures have surged in recent months, the last week or two have seen them stagnate as mortgage rates soared…

{kind=link}

Signings rose in all four regions in the month, led by a more than 10% gain in the West.

“An extra bump occurred in the West region because of lower home prices, while gains in the South were due to stronger job growth in that region,” Yun said.

Even with the surge at the start of the year, contract signings were still down 22.4% from January 2022 on an unadjusted basis.

https://www.zerohedge.com/markets/us-pending-home-sales-explode-higher-january

February 27, 2023

BASF SE (BASFY) Q4 2022 Earnings Call Transcript

Feb. 24, 2023 11:26 AM ETBASF SE (BASFY), BFFAF

BASF SE (OTCQX:BASFY) Q4 2022 Earnings Conference Call February 23, 2023 2:00 AM ET

Company Participants

Stefanie Wettberg – SVP, IR

Martin Brudermuller – Chairman & CEO

Hans-Ulrich Engel – Supervisory Board Member

Martin Brudermuller

Good morning, ladies and gentlemen. Hans Engel and I would like to welcome you to our virtual conference for analysts and investors. Exactly 1 year ago, Russia invaded Ukraine. Since then, war has been raging in the middle of Europe. We condemn Russia’s attack. For the Ukrainian people, it is a catastrophe. And the past year has taught us all a harsh lesson. Peace and economic stability must never be taken for granted.

The consequences for the global economy have been tremendous. 2022 was marked by great uncertainties, rising energy prices, inflation and concerns about the widespread economic distortions. On January 17, BASF released preliminary figures for the full year 2022. Today, Hans and I will first provide you with further details regarding our business development in Q4 and the full year 2022. Subsequently, I will present the decisive actions we are taking to strengthen our competitiveness in Europe and particularly in Germany.

Let’s start with the challenging macroeconomic environment. Over the course of 2022, the global macroeconomic environment has deteriorated significantly. There are currently no signals of substantial improvement in the short term. Russia’s war against Ukraine, high inflation and the sharp increase in energy prices led to a slowdown in consumer demand, particularly in Europe. To combat inflation, Central Banks raised interest rates considerably, which further dampened consumer spending. Demand in our consumer industries softened in the course of 2022, with 2 exceptions.

According to the current data, global automotive production reached 82 million units in 2022 and thus increased by 6% compared with the very low level of previous year. Supply shortages, particularly for the semiconductors have gradually eased. For 2023, we expect a slight increase to around 84 million units. Global agriculture production also continued to grow moderately in the course of 2022. However, overall production growth was lower than in 2021, partially due to the normalization of growth rates after higher-than-average growth in 2021. In addition, production growth was impacted by longer spells of trough in several regions as well as production disruptions in Ukraine as a result of the war.

Let’s now look at chemical production by region. Full year growth is shown on the middle bar. Based on currently available data, global chemical production grew by only 2.2% in 2022. While the markets in China and North America grew, chemical production declined massively in Europe, and also fell in Asia, excluding China. Chemical production growth in China slowed slightly in 2022 compared with a strong baseline in 2021. This was mainly due to lower demand as a result of COVID-related lockdowns. In North America, chemical production growth increased compared with the previous year. In 2021, growth had been negatively impacted by the freeze in the first quarter and the hurricanes in summer and autumn. Chemical production in Europe declined substantially. Lower demand and higher energy prices led to shutdowns of selected production capacities, especially in the second half of 2022. This was particularly apparent in Germany, where chemical production declined by around 12% in 2022.

Lower demand and higher energy prices were also the main reasons for the decline in chemical production in Asia, excluding China. As the following slides, we’ll mainly focus on BASF’s business performance in Q4 2022, I will also briefly comment on chemical production in the last quarter of the year.

In Q4 2022, global chemical production increased by only 1%, a considerable increase, which was surprising in the overall weak environment was only seen in China. This was particularly driven by a base effect as chemical production in China had been negatively impacted by electricity cuts in the fourth quarter of 2021. All other regions recorded a decline in chemical production, which was most pronounced in Europe.

Moving on to BASF. In Q4 2022, our sales decreased by 2% to €19.3 billion, mainly on account of lower volumes. Sales volumes declined by 15%, with the exception of Agricultural Solutions, all segments recorded lower volumes. Sales prices increased by 9%. All segments were able to increase prices, except for chemicals, where prices declined on account of weak demand. Portfolio effects of minus 1% were mainly caused by the sale of the Kaolin Minerals business, which had been part of the Performance Chemicals division until the divesture. Currency effects of plus 4.5% had a positive impact on sales and were primarily related to the U.S. dollar.

Let’s now move on to our earnings development by segment in Q4 2022 compared with the strong prior year quarter. The overall decline in EBIT before special items resulted largely from considerably lower contributions from the Chemicals and Materials segments. In Q4 2022, these 2 segments contributed only €65 million to BASF’s group EBIT before special items compared with €933 million in the prior year quarter. This was mainly due to lower volumes and margins on the back of low demand in high energy and raw material prices. In total, earnings in BASF’s for downstream segments improved by €229 million and amounted to €393 million.

Hans-Ulrich Engel

Thank you, Martin. Good morning, ladies and gentlemen. In the following, I will provide you with further details of BASF Group’s financial figures in the fourth quarter of 2022 compared with the prior year quarter. I will start with EBITDA before special items, which decreased by 36% and amounted to €1.4 billion. EBITDA amounted to around €1.4 billion to a decrease of €862 million. At €373 million, EBIT before special items declined by 70%. Special items in EBIT amounted to minus €254 million compared with plus €1 million in the fourth quarter of 2021. The special items were mainly related to noncash effective impairments on plans in Ludwigshafen.

EBIT decreased by 90% to €119 million in Q4 2022. Income from nonintegral companies accounted for using the equity method amounted to minus €4.7 billion compared with plus €112 million in Q4 2021. The strong decline was driven by noncash effective impairments on the shareholdings in Wintershall Dea AG in the amount of about €4.7 billion in Q4 2022. These impairments resulted in particular from the deconsolidation of the Russian exploration and production activities of Wintershall Dea due to the loss of actual influence and economic expropriation. The remaining value of the Russian participations of Wintershall Dea declined significantly and further write-downs were made on the European gas transportation business.

Let’s now look at BASF’s operational earnings development from a regional perspective. Our competitiveness in Europe and particularly in Germany, has declined. In 2015, Germany, Europe, excluding Germany and the other regions each contributed around 1/3 to BASF Group’s EBIT before special items. In the strong business year 2021, Europe, including Germany, contributed only 1/3, while the other regions contributed 2/3. After the strongest ever first half, earnings softened in the further course of 2022 and we saw a particular deterioration in our German operations. In the second half of 2022, the contribution of Germany was even negative and we ended the year with an overall year before special items contribution of minus €126 million. This shows how important a balanced regional footprint is for our risk management. We will, therefore, continue to strengthen our business growth outside of Europe while adapting our business in our home region to reflect the changed framework conditions.

One explanation for the earnings decline in Europe are the elevated energy costs in the region. In 2022, our operational earnings were burdened by additional energy cost of €3.2 billion globally. Europe accounted for around 84% or €2.7 billion of this increase which mostly impacted our Verbund site and Ludwigshafen. Higher natural gas costs accounted for 69% or €2.2 billion of the overall increase in energy costs. And again, the main impact was on Europe and on Ludwigshafen. In 2022, we reduced our natural gas consumption by around 1/3 in Europe. This was primarily due to lower production volumes. Nevertheless, as mentioned before, we incurred €2 billion in additional cost for natural gas in Europe alone compared with 2021.

Martin Brudermuller

We anticipate only moderate growth in the majority of our customer industries in 2023. Our forecast assumes that the war in Ukraine will continue but not escalate further. Even so, the further developments of the war and its effects on economic growth are still subject to a high degree of uncertainty. In addition, we are assuming that an acute gas shortage with regulatory cuts to energy-intensive industries in Europe will not materialize. We expect that China’s departure from its Zero COVID strategy will have a positive impact on demand and will stimulate growth globally.

Based on these assumptions, we expect the global economy to grow by only 1.6% in 2023. We forecast growth of 1.8% for global industrial production, while global chemical production is likely to expand by 2% in 2023. Our planning assumes an average exchange ratio of USD 1.05 per euro and an average oil price of USD 90 for a barrel of Brent crude. We anticipate elevated and very volatile gas prices in Europe. In few of these factors, we forecast BASF Group to generate sales of between €84 billion and €87 billion in 2023. EBIT before special items is expected to decline to between €4.8 billion and €5.4 billion.

We expect a weak first half of 2023, followed by an improved earnings environment in the second half of the year due to recovery effects, especially in China. Based on the weaker earnings performance and slightly higher cost of capital base is forecast for BASF Group in 2023, we anticipate a ROCE of between 7.2% and 8%. We expect CO2 emissions of between 18.1 million metric tons and 19.1 million metric tons as a result of moderate growth in production and slightly higher capacity utilization at emission-intensive plants.

We will now move on to the measures to increase the competitiveness and profitability of BASF Group. I will focus on 2 areas in the second part of today’s presentation. We will begin with the cost savings program focusing on Europe that we announced in October. This will be followed by a longer section on the adaption of our Verbund structures in Ludwigshafen. Europe’s competitiveness is increasingly suffering from overregulation, slow and bureaucratic permitting processes and high costs for most of the production input factors. This has resulted in many years of low market growth. High energy prices are putting an additional burden on our profitability and competitiveness in Europe. Our cost savings program, therefore, focuses on rightsizing our cost structures in Europe and particularly in Germany to reflect these circumstances.

We will implement the program from 2023 to 2024. On completion, the program is expected to generate annual savings of more than €500 million in non-production areas. What do we mean with non-production areas? These include service, operating and research and development divisions as well as the corporate center. Roughly half of the cost savings are expected to be realized at the Ludwigshafen site. The measure under the program include the consistent bundling of services and hubs, simplifying structures in divisional management, the rightsizing of business services as well as increasing the efficiency in R&D activities. Globally, the measures are estimated to have a net effect on around 2,600 positions. This includes the creation of new positions, in particular in the hubs and program costs are expected to amount to around €400 million. This will cover training and qualification measures, relocation costs and severance packages. Employee representatives in the relevant bodies have been and will continue to be involved regarding the various measures.

Let’s now move from the non-production areas to production at our largest site worldwide in Ludwigshafen. This is a schematic picture of the Ludwigshafen and Verbund site today in terms of inputs and outputs. We require vast amounts of natural gas as an energy source to power our plants and as a feedstock for our products. Today, renewable energy and renewable feedstocks still play a relatively small role. As outputs, we currently sell significant volumes of several base chemicals to the market. However, we mainly use base chemicals within the Verbund to produce a vast range of around 8,000 downstream products for European and global customers. And as a collateral output, this site emits about 7 million metric tons of carbon dioxide per year. Based on 2021 figures, the Ludwigshafen site accounts for about 4% of Germany’s natural gas consumption. In few of the large amount of gas we consume, it comes as no surprise that our competitiveness in Ludwigshafen suffers in times of elevated energy prices.

European gas prices skyrocketed to unseen levels in August. Since then, prices have declined, but we expect them to stay considerably higher in the long run compared to what they were over the past several years. Furthermore, lower market growth in Europe has negatively impacted supply and demand dynamics in several value chains. We are, therefore, undertaking structural measures to improve our competitiveness over the long term in addition to the cost savings program we have initiated. During the past months, we have carried out a thorough analysis of our Verbund structures in Ludwigshafen. By assessing our asset base in detail, we reached a deep understanding of how to ensure the continuity of profitable business while making necessary adoptions.

Let me now highlight the major changes we will be implementing. Let’s start by looking at the ammonia value chain. Ammonia is the largest consumer of natural gas as a raw material in Ludwigshafen. Currently, we operate 2 ammonia plants at the site, which you see in a simplified diagram on the left side of the slide. Ammonia is an important input factor for caprolactam and with that for polyamide-6, adipic acid as well as nitrogen fertilizers. Caprolactam, in particular, has seen tremendous buildup of capacities in recent years, especially in China. As a result, European exports to Asia were already under pressure before the sharp increase in Europe’s energy prices. To reduce our exposure to the market, we intend to close our caprolactam production in Ludwigshafen. BASF caprolactam in [indiscernible] is sufficient to serve captive and merchant market demand in Europe going forward.

By closing the caprolactam plant in Ludwigshafen, we will significantly reduce captive demand for the precursor ammonia. And in turn, this allows us to close 1 of the 2 ammonia plants as well as associated fertilizer facilities. At the same time, we will use the changes as an opportunity to optimize our polyamide 6 production network and further strengthen this important business for BASF Group. High value-added products such as standard and specialty amines and the AdBlue business, for example, will be unaffected and will remain competitive. They will be supplied via the second ammonia plant at the Ludwigshafen site.

Let us now move on to the next value chain, adipic acid. As 1 of the main precursors of polyamide 6.6, adipic acid is an essential part of our Engineering Plastics business. In addition, to serving captive demand, we sell production volumes to the merchant market. Over recent years, however, margins in this part of the business have been steadily eroded due to overcapacities in Asia and lower-than-anticipated domestic market growth. This situation became even worse with the sharp increase in European energy prices. In response to this changed market environment, we will reduce our adipic acid production capacity in Ludwigshafen and will close the precursor plant for cyclohexanol and cyclohexanone as well as the production of soda ash. With these measures, we will reduce our merchant market exposure while improving our overall earnings. Adipic acid production at our joint venture with Domo in Chalampe in France will remain unchanged and has sufficient capacity to supply our business in Europe. We will also continue to operate our polyamide 6.6 production plants in Ludwigshafen.

The certain value chain I want to address is the TDI production complex in Ludwigshafen. Over the past years, both MDI and TDI have gone through significant demand and profitability cycles. Overall, market demand for MDI is healthy as expected and continues to grow. Demand for TDI for however, did not grow as expected and has been especially weak in Europe, Middle East and Africa. We do not expect this to change. As a result, our TDI complex in Ludwigshafen has been underutilized and has not met our expectations in terms of economic performance. This situation has further worsened with sharply increasing energy and utility costs. We have, therefore, decided to close our TDI plant and the precursor plants for DNT and TDA. We remain fully committed to our European customers, and we’ll continue to serve them via our global production network with our existing TDI plants in Geismar, Louisiana, Yeosu, South Korea and Shanghai, China.

As I mentioned earlier, we thoroughly analyzed our asset base in Ludwigshafen. This included the gas intensive acetylene value chain as well as olefins from our 2 steam crackers in Ludwigshafen. While we identified some optimization potential in these value chains, our analysis shows that these assets will remain competitive in the long term, even under the changed framework conditions. In total, 10% the replacement — asset replacement value at the site will be affected by the measures. This will likely affect around 700 positions in production. However, we are very confident that we will find suitable positions for most of the affected employees since there are vacancies in production and many colleagues will retire in the next few years.

The measures will be implemented stepwise by the end of 2026 and are expected to reduce fixed costs by more than €200 million per year. These structural changes will also lead to a significant reduction in power and natural gas demand at the Ludwigshafen site. Consequently, CO2 emissions in Ludwigshafen will be reduced by around 0.9 million metric tons per year. This corresponds to a reduction of around 4% in our global CO2 emissions.

Since the start of the Russian war against Ukraine, we had analyzed in depth what factors influence the gas consumption of our Verbund, both positively and negatively. When uncertainties regarding gas supply first arose, we mentioned 50% at a minimum for operating the Ludwigshafen for Verbund site. Now we are able to continue operations even if the gas supply were to drop as far as 30% of our average consumption in 2021. This is thanks to optimization measures that including using the byproduct ethane from our steam crackers to feed our acetylene plant and the recommissioning of sections in the synthesis gas plant that is independent from natural gas.

We are now executing further projects that will reduce gas consumption in Ludwigshafen even further. By the end of this year, we will convert 2 of our 4 natural gas turbines in our combined heat and power plants to allow operation with either natural gas or fuel oil. Gas allocation would nevertheless force us to shut down many production plants at the site, but under optimal conditions and this natural gas consumers taken offline, we would, however, still be able to run the Ludwigshafen site at a supply rate of around 10% of our average gas consumption in 2021. Thanks to a possible partial conversion to fuel oil, we will thus be able to avoid a complete shutdown.

I congratulate the BASF team for its creativity and dedication in developing the required solutions during the last 12 months. Reducing the demand for natural gas is 1 of the elements in the transformation of the Ludwigshafen site. We want to develop Ludwigshafen into the leading low-emission chemical production site in Europe and are initiating further changes needed to achieve this. The green arrows indicate the time lines for preparations and investments while the extended arrows indicate better transformation along the particular levers has more or less ended steady state. We are exploring how we can best accelerate the transformation and how we can move forward most efficiently with regard to abatement costs.

We are making good progress. As part of the gray to green lever, we will secure further supplies of renewable energy in line with our Make & Buy strategy. With regard to the electrification of the Ludwigshafen site, we are taking steps to establish the platforms and infrastructure that we need to supply the site with renewable electricity and hydrogen. We are planning the use of heat pumps and cleaner ways of generating steam. In a transition phase, we are also looking into possibilities for using carbon capture and storage for hard-to-abate CO2 streams before moving to carbon capture and utilization. In addition, we will employ new CO2-free technologies such as water electrolysis to produce hydrogen. And finally, we plan to use the flexible entry options offered by our Verbund to switch from fossil to circular and renewable raw materials.

I’m concluding my remarks, and I want to reemphasize what BASF stands for. You can rely on BASF to continue to deliver what is known and where we are — what is known from us and what we are respected for. Connectedness lies at the core of BASF and is exemplified by our Verbund. The flexibility of our Verbund clearly demonstrated by the measures we have taken, and we will continue to take to reduce our natural gas demand. We will build on the benefit it offers both in Ludwigshafen and at other Verbund sites worldwide. Our global footprint with production assets close to our customers in all regions, proves to be the right setup particularly in a world that is becoming increasingly multipolar.

With our ongoing investments in China and the United States, we continue to improve our regional footprint. We are expanding our global presence in growing market segments, for example, in the battery materials value chain. Our transformation towards Net Zero will enable us to provide our customers with a complete portfolio of products that have reduced or even net zero carbon footprint. This will differentiate us from our competitors. Here, too, the Verbund plays an important role, and we will be — and will be supported by our powerful global R&D teams. All of these things would not be possible without our employees. And I’m therefore proud that we can count on such a great team at BASF, and I thank the team for its commitment in these challenging times. Thus, our shareholders can rely on BASF for value generation over the long term. Thank you.

Stefanie Wettberg

There’s a bit more specific questions on the closures in Ludwigshafen. It’s from Markus Mayer, Baader-Helvea. Why does the closure of plants in Ludwigshafen not trigger further impairments? Do you not need to write down the TDI plant? Is the TDI pant closure more linked to the energy situation or to production issues the plant had?

Martin Brudermuller

I mean, first of all, let me say some of the plants I have mentioned, adipic acid, caprolactam are part of BASF’s structure for a long time. These are rather old plants that have been totally depreciated. So from that point of you don’t see any write-downs or impairments coming with that. I think I mentioned also that they have been under pressure also from market points in terms of utilization. And now really, they get another hit by the energy prices. And this is, I think, while we also have a good opportunity to now, let’s say, restructure 1 of the oldest parts, I think, in the Ludwigshafen part.

The TDI plant is certainly a more new one. And I think I mentioned that also here, I think — the most disappointing part is actually the market development in Europe, which is significantly below what we have expected. It grows below 1%, most probably going forward in the next 10 years. If you look on to the supply balance — supply-demand balance on a global point of view, we have a very low utilization on the global level for all the plants. It is also a product which is not so difficult to transport much easier than actually MDI. So that is — you can run that as a global business. And this is why actually all the assets all over the world can participate in regional markets. And I think this is one of the major aspects also where we see not the scenario that we can really fully load these plants economically in terms of a market development.

When it comes to the depreciation part, I quickly hand over to Hans because that is the only plant that has a little bit less history in BASF and the other ones.

Hans-Ulrich Engel

Yes. And Markus, when you look closely at the Q4 P&L, you see that there is a €0.25 billion in special items there. The vast majority of that are write-down/impairments on plants in Ludwigshafen resulting from the high gas and energy cost or in other words, part of the closures that we are now announcing. And I’d say digesting that in the quarter is a significant number.

Stefanie Wettberg

Okay. So we continue another question related to that topic area. Mubasher Chaudhry from Citi. With regard to the various shutdowns announced, is there any option to bring any of these plants back online? Should the demand picture improve in the medium term?

Martin Brudermuller

No. I think this is more or less excluded because, first of all, when you start to shut down these plants and you really want to reduce the fixed cost. You have also to solve the teams and have really to get the fixed cost off and also not stay with remnant costs or holding a team for such a moment, then you don’t gain anything. We will then clean up the plants, and we will really shut them down. We will not demolish everything on the right on the spot. We don’t need the space in Ludwigshafen. We will then do that or use it or demolish it when we need a certain phases also for growth again. But I think in order to really tap into this roughly €200 million of fixed cost reduction, you really also have to eliminate the structures.

I would also say, once we have started to then bring down an ammonia plant, which is branching out is a very important raw material also, you adapt a lot of service, utility in precursor plants than to the new scenario, you certainly also reduce costs in these plants if they have lower capacities. So if you do that in a way that you actually say, more and a most appalling thing than you do not get the cost reduction. So for that reason, we decided to do that for good.

Stefanie Wettberg

Now there’s a question from Georgina Fraser, Goldman Sachs. It’s a combination of outlook and the measures announced for Ludwigshafen. What are your midterm energy cost assumptions for Europe? What was the scenario under which the site closure decisions have or the plant closure decisions have been taken?

Hans-Ulrich Engel

Georgina, what we’ve done is we worked with the overall assumption that the very competitive, not to say price advantaged gas deliveries from Russia will not play a role in Europe, and in particular, in Northwestern Europe going forward. What does that lead to? That leads to the question, what will be price setting for Northwestern Europe going forward? We think that there is a high likelihood that the price for Northwestern Europe for natural gas and then resulting from that to a certain extent also for power will be set on the basis of LNG imports. What are the key sources for LNG imports, as we all know, that is the U.S. and also Qatar.

We think there is a high likelihood that the base for price will be Henry Hub price plus then the cost of the LNG supply chain. In other words, from the liquefaction transportation to gasification. That cost is somewhere in the order of magnitude of $5 to $6 per million BTU. So Henry Hub plus supply chain costs for LNG is what we think will form the basis for prices going forward. We also think it will take probably about 2 years to get to this situation. This is with all the problems in the entire system currently, probably the time to establish a full LNG supply chain, the situation in Germany, where thankfully, the first FSRUs. So the floating terminals are now up and running, but to create and establish an LNG import structure will take a bit of time. But in the end, these are the assumptions that we used. In other words, with respect to natural gas and also power situation where prices should be higher in Europe than they were in the past.

Martin Brudermuller

And maybe to add 1 part on that because, I mean, competitiveness is a relative thing and not an absolute thing. And if you now hear politicians talking, okay, energy price is getting low now. So — or the danger, everything is off that of the political agenda or the society feel safe. But I think if you actually take the current prices of roughly €50 per megawatt hour you have today and you compare it with the low number you have in the annually up in the moment, you have actually a factor of 6 in between Europe and the U.S. and that is quite significant if you are in the energy-intensive business.

So we have — and that’s what I said this earlier when I got the question of Tim whether there’s more to come. I think we have a robust scenario with different scenarios where we actually back tested that situation. And I can only warn that this is not a topic that is quickly off. I mean we have really to look into the whole value chains in Europe. It’s not only about ours that we have to bring the material still competitively to our customers. But also our customers throughout the value chain, they have to take care about their competitiveness that they keep their market share that they keep their export businesses. If they would actually also fail, then you will see a further softening of the demand in the long run, which makes it difficult to keep the whole ecosystem of Europe, which is 1 of the very last remaining or the only ones where you have full value chains and interlinked value chain.

So I would say we will do our share, but I hope also our customers are bold enough to restructure and take the right steps to ensure that the whole value chain stays competitive. We have talked to a lot of customers about that. but that is also what we cannot totally factor in on our own exercise. We have to do our step and the others have to do their share.

Stefanie Wettberg

Charlie Webb from Morgan Stanley has a related question, but it’s a bit broader, not only focused on BASF, is your TDI production of the cost curve at current energy prices and no longer competitive domestically? It’s hard to talk for others, but — I mean.

Martin Brudermuller

I mean, I think I mentioned it already. I mean I said that competitiveness is a relative term. And I mean if you look into the energy situation in some of the countries where other production positions are, depreciated plants, very well established plants also in their local and regional markets where the base load is then they have also a good — a better, let’s say, competitive position gain now over the recent times since Europe got in this difficult situation. So that also import material is coming into Europe. So for that reason, yes, that’s a good example where Europe, as such, I would say, has lost competitiveness.

Stefanie Wettberg

This related question to, in this case, Region North America. It’s from Sebastian Satz, Barclays. Can you elaborate to what extent BASF may be able to benefit from various government support packages for the energy transition? And specifically thinking about the U.S. Inflation Reduction Act, for example, blue ammonia, or the discussions of an industry power price in Germany?

Hans-Ulrich Engel

Yes. Thank you, Sebastian, for your question. Of course, we are looking into the incentives that come with the Inflation Reduction Act, which, by the way, is the misnomer of the year 2022, but that’s different. That is a different story. As you know, what we do as BASF, we invest in the markets where our customers are. So we are investing in North America for our North American customers. We’re investing in Europe for our European and in Asia for our Asian customers. That’s our basic philosophy. And this basic philosophy will not be changed as a result of support schemes such as, for example, the IRA. Nevertheless, we are looking into it.

There can be certain activities that clearly benefit. As you know, we have big activities in the U.S. Gulf Coast. We have a major investment in our site at Geismar, Louisiana, the new MDI plant there. You look at what we’ve just announced with respect to the 5-year CapEx plan were around about €4 billion to €4.5 billion is earmarked for North America for the next 5 years. So you see this is a significant investment that we intend to do there. And in a scenario such as, for example, carbon capture and storage, the IRA provides, I would say, highly attractive incentives and we’ll certainly look into that. But again, basic philosophy is we produce where our customers are.

Stefanie Wettberg

I think with that, you answered, there were a few more questions from Laurent Favre, Sebastian Bray on Wintershall Dea, but that is covered. So I switch back to TDI and a question from Sebastian Bray, Berenberg. There’s quite a lot of TDI capacity exiting the market as a result of changes announced, will BASF need to spend on expanding assets elsewhere to compensate for this. Will you need additional shipping capacity for TDI? Also how much soda ash capacity is being shut?

Martin Brudermuller

I mean, first of all, a clear no. No, we don’t need additional CapEx to expand capacities in other sites. So we really can use existing capacities for covering our European market position. Certainly, we have to increase logistics. This is clear, you have to organize this. You have then to establish the supply chain that you also ensure that you have enough volumes here then in Europe from the imports to be on the safe side for your customers. This is all very clear. Please understand for the competitive reasons that I’m not going to talk about capacities now also for soda ash.

Interesting to note that all questions went through Stefanie. I’ll have to research if this is standard procedure for BASF or a one time thing, but it isn’t for other companies. Editor Comments

February 24, 2023

![]()

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited

take no responsibility for the contents of this announcement, make no representation as to

its accuracy or completeness and expressly disclaim any liability whatsoever for any loss

howsoever arising from or in reliance upon the whole or any part of the contents of this

announcement.

Sinomax Group Limited

盛諾集團有限公司

(Incorporated under the laws of the Cayman Islands with limited liability)

(Stock Code: 1418)

PROFIT WARNING

This announcement is made by Sinomax Group Limited (the “Company”, together with its

subsidiaries, collectively the “Group”) pursuant to Rule 13.09(2)(a) of the Rules Governing

the Listing of Securities on The Stock Exchange of Hong Kong Limited (the “Listing Rules”)

and the Inside Information Provisions (as defined in the Listing Rules) under Part XIVA of the

Securities and Futures Ordinance (Chapter 571 of the Laws of Hong Kong).

The board of directors of the Company (the “Board”) wishes to inform the shareholders of

the Company and potential investors that, based on a preliminary review of the unaudited

consolidated management accounts of the Group for the year ended 31 December 2022

(“FY2022”) and other information currently available to the Board, the Group is expected to

record a loss after taxation for FY2022 of not less than HK$35 million as compared to a profit

after taxation for the year ended 31 December 2021 of approximately HK$31 million. This

was primarily attributable to the continual outbreak of the COVID-19 which had critically

weakened both local and global consumption market and also the sales of the Group, and the

impact of the above also resulted in higher supply chain and logistic costs of the Group.

The Company is in the process of finalising the Group’s audited consolidated financial results

for FY2022. This announcement is made based on a preliminary review of the unaudited

consolidated management accounts of the Group for FY2022 and other financial information

currently available, which are subject to finalisation and possible adjustments upon review and

audit by the Company’s auditors or audit committee. Further details of the Group’s financial

results for FY2022 will be disclosed in the annual results announcement of the Company,

which is expected to be published on 28 March 2023.

Shareholders and potential investors of the Company are advised to exercise caution

when dealing in the shares of the Company.

By order of the Board

Sinomax Group Limited

Lam Chi Fan

Chairman

Hong Kong, 10 February 2023

As at the date of this announcement, the executive Directors are Mr. Lam Chi Fan (Chairman

of the Board), Mr. Cheung Tung (President), Mr. Chen Feng, Mr. Lam Kam Cheung

(Chief Financial Officer and Company Secretary) and Ms. Lam Fei Man; and the independent

non-executive Directors are Mr. Wong Chi Keung, Professor Lam Sing Kwong Simon,

Mr. Zhang Hwo Jie and Mr. Wu Tak Lung.

https://www1.hkexnews.hk/listedco/listconews/sehk/2023/0210/2023021000667.pdf

February 24, 2023

Covestro to build its largest TPU site in China

February 24, 2023Rekha NairBusiness0

Covestro will build its largest Thermoplastic Polyurethanes (TPU) site in Zhuhai, China. With an overall investment in the low three-digit million Euro range it will also be the company’s largest investment in its TPU business. TPU are a highly versatile plastic material, a real multi-talent that offers a broad range of properties for a diverse set of applications like sports shoe soles, IT devices such as sweepers, smart speakers and phonecases or automotive applications.

“This investment shows our ongoing commitment to growth in our Solutions & Specialties business entities”, said Covestro CCO Sucheta Govil. “With this new plant for TPU we want to capture the expected fast and high market growth of the TPU market globally, and especially in Asia and China. The production site will be able to serve both the growing Asian markets, as well as demand in Europe and North America.”

Located in the Zhuhai Gaolan Port Economic Development Zone in Guangdong province, the new site will eventually span across 45,000 square meters. It shall be completed by 2033 and is expected to achieve a production capacity of nearly 120,000 tons of TPU per year. It will be built in three phases. The mechanical completion of the first phase is estimated for the end of 2025. This will lead to a production capacity of about 30,000 tons per year and the creation of about 80 new jobs. The initial investment for this phase lies in the mid double-digit million Euro range.

“I’m delighted to share this important news for our Business Entity. This new plant will enable us to be in close proximity to our customers and the value chains in the IT, consumer electronics, footwear and other industries”, said Dr. Andrea Maier-Richter, Head of TPU at Covestro. “The majority of the TPU market and its growth prospects are in Asia and particularly in China. Our investment there shows our clear intention: We want to remain successful with our customers and partners in the long run.”

An innovation center will also be part of the investment, enabling researchers on-site to design customized material formulas and to do formula adjustment to meet customer demands within very short cycles. Sustainable and ever more circular solutions are among the long-term core target for these efforts. This shall also support broadening the offerings under the recently introduced, sustainable “CQ” product line. Products labelled as such consist of at least 25% alternative, non-fossil raw materials. The site will furthermore utilize the most advanced production technologies and be run on 100% green power. It will produce injection molding grades for footwear and a wide range of IT devices, as well as extrusion grades for cables, hoses and tubes or automotive applications.

Covestro to build its largest TPU site in China

February 24, 2023

BASF shows resilience in a challenging market environment and implements measures to strengthen competitiveness

- Sales: €87.3 billion (plus 11.1 percent)

- EBIT before special items: €6.9 billion (minus 11.5 percent)

- Cash flows from operating activities: €7.7 billion (plus 6.4 percent); Free cash flow: €3.3 billion (minus 10.2 percent)

- Proposed dividend of €3.40 per share for business year 2022 (2021: €3.40 per share)

- Presentation of concrete measures to save costs in Europe and to adapt Verbund structures in Ludwigshafen

Outlook 2023:

- Sales of between €84 billion and €87 billion expected

- EBIT before special items of between €4.8 billion and €5.4 billion expected

BASF Group has shown resilience in the 2022 business year in a challenging market environment that was dominated by the consequences of the war in Ukraine and in particular by increased raw material and energy prices. As Dr. Martin Brudermüller, Chairman of the Board of Executive Directors, and Dr. Hans-Ulrich Engel, Chief Financial Officer, explained during the presentation of the figures for 2022, BASF increased sales by 11.1 percent to €87.3 billion. Sales growth was mainly driven by higher prices across almost all segments due to an increase in raw materials and energy prices. The Materials and Chemicals segments implemented the highest price increases. Significantly lower volumes overall dampened sales growth in the BASF Group. Volumes development was primarily driven by lower sales volumes in the Surface Technologies and Chemicals segments.

At €6.9 billion, income from operations (EBIT) before special items was 11.5 percent below the prior-year figure, but within the forecast range. The earnings development was attributable to a strong decline in earnings contributions from the Chemicals and Materials segments. Both segments recorded lower margins and volumes as well as higher fixed costs.

By contrast, EBIT before special items rose in all other segments. The Agricultural Solutions segment increased EBIT before special items considerably, in particular as a result of the positive sales performance due to increases in volumes and prices. The Nutrition & Care segment also achieved a considerable increase, mainly due to price-driven margin growth. The Surface Technologies segment recorded considerably higher earnings, especially due to increased earnings contributions from the automotive catalysts and battery materials businesses. Higher prices and volumes in the Coatings division additionally supported the segment’s earnings performance. The Industrial Solutions segment slightly increased EBIT before special items as a result of price-driven margin growth. EBIT before special items attributable to Other improved slightly.

In 2022, BASF Group’s operational earnings were burdened by additional energy costs of €3.2 billion globally. Europe accounted for around 84 percent of this increase, which mostly impacted the Verbund site in Ludwigshafen. Higher natural gas costs accounted for 69 percent of the overall increase in energy costs globally.

Special items in EBIT amounted to minus €330 million in 2022 compared with minus €91 million in the previous year. At €6.5 billion, EBIT for the BASF Group in 2022 was considerably lower than in the previous year. This figure includes income from integral companies accounted for using the equity method, which declined by €289 million to €386 million.

Exceptionally high impairments on the shareholding in Wintershall Dea AG negatively affected the BASF Group’s net income from shareholdings. In 2022, net income from shareholdings amounted to minus €4.9 billion, after €207 million in 2021. The significant decline was due to special charges of around €6.3 billion, mainly from non-cash-effective impairment losses on the shareholding in Wintershall Dea AG. These were especially due to the deconsolidation of Wintershall Dea’s Russian exploration and production activities, which subsequently resulted in a revaluation of Wintershall Dea’s Russian shareholdings. Further write-downs were made on Wintershall Dea’s European gas transportation business, including a complete impairment on the shareholding in Nord Stream AG and the financing of the Nord Stream 2 project. Wintershall Dea’s operating earnings contribution for 2022 rose to approximately €1.5 billion, after €335 million in the previous year.

As a result of the significantly lower net income from shareholdings, net income for the BASF Group was minus €627 million compared with €5.5 billion in 2021.

Development of sales and earnings of the BASF Group in the fourth quarter of 2022

In the fourth quarter of 2022, BASF Group sales decreased by 2.3 percent to €19.3 billion, mainly on account of lower volumes. Fourth-quarter EBIT before special items fell by 69.6 percent to €373 million compared with the prior-year quarter.

Special items in EBIT amounted to minus €254 million compared with plus €1 million in the fourth quarter of 2021. The special items were mainly related to non-cash-effective impairments on plants in Ludwigshafen. In the fourth quarter of 2022, EBIT decreased by 90.3 percent to €119 million. Net income amounted to minus €4.8 billion compared with €898 million in the fourth quarter of 2021. The decline was driven by the impairments on the shareholding in Wintershall Dea.

Cash flows of the BASF Group in 2022 and in the fourth quarter of 2022

For 2022, cash flows from operating activities amounted to €7.7 billion compared with €7.2 billion in the previous year. Free cash flow amounted to €3.3 billion in 2022 after €3.7 billion in 2021.

Compared with the prior-year quarter, cash flows from operating activities improved by €1.1 billion to €4.5 billion in the fourth quarter of 2022. Free cash flow increased by €749 million to €2.6 billion in the fourth quarter.

Dividend proposal of €3.40 per share

At the Annual Shareholders’ Meeting, the Board of Executive Directors and the Supervisory Board will propose a dividend of €3.40 per share, equal to the prior-year dividend. Based on the year-end share price, the BASF share would thus offer a high dividend yield of around 7.3 percent. This would represent a payment of €3.0 billion to shareholders.

Outlook for 2023 for the BASF Group

The high level of uncertainty that arose over the course of 2022 due to the war in Ukraine, high raw materials and energy costs in Europe, rising prices and interest rates, inflation and the development of the coronavirus pandemic will continue in 2023. All of these factors will negatively impact global demand. BASF thus only expects moderate growth of 1.6 percent for the global economy in 2023 (2022: 3.0 percent). For global chemical production, BASF expects growth of 2.0 percent (2022: 2.2 percent). The company assumes an average oil price of $90 for a barrel of Brent crude and an average exchange rate of $1.05 per euro.

Based on these assumptions, the BASF Group is expected to generate sales of between €84 billion and €87 billion in 2023. The BASF Group’s EBIT before special items is expected to decline to between €4.8 billion and €5.4 billion. The company expects a weak first half of 2023 followed by an improved earnings environment in the second half of the year due to recovery effects, especially in China.

BASF specifies measures to save costs in Europe and to adapt Verbund structures in Ludwigshafen

In his presentation, Martin Brudermüller also announced concrete cost savings measures focused on Europe as well as measures to adapt the production structures at the Verbund site in Ludwigshafen. “Europe’s competitiveness is increasingly suffering from overregulation, slow and bureaucratic permitting processes, and in particular, high costs for most production input factors,” said Brudermüller. “All this has already hampered market growth in Europe in comparison with other regions. High energy prices are now putting an additional burden on profitability and competitiveness in Europe.”

Annual costs savings of more than €500 million by the end of 2024

The cost savings program, which will be implemented in 2023 and 2024, focuses on rightsizing BASF’s cost structures in Europe, and particularly in Germany, to reflect the changed framework conditions. On completion, the program is expected to generate annual cost savings of more than €500 million in non-production areas, that is in service, operating and research & development (R&D) divisions as well as the corporate center. Roughly half of the cost savings are expected to be realized at the Ludwigshafen site.

The measures under the program include the consistent bundling of services in hubs, simplifying structures in divisional management, the rightsizing of business services as well as increasing the efficiency of R&D activities. Globally, the measures are expected to have a net effect on around 2,600 positions; this figure includes the creation of new positions, in particular in hubs.

Adaptations to the Verbund structures in Ludwigshafen are expected to lower fixed costs by over €200 million annually by the end of 2026

In addition to the cost savings program, BASF is also implementing structural measures to make the Ludwigshafen site better equipped for the intensifying competition in the long term. “We are doing this because we believe in the future of the Ludwigshafen site, which is now in its 158th year. We believe in the people who work here, and we believe in the region Europe. We remain committed to this site and have the courage to further develop it,” said Brudermüller.

During the past months, the company carried out a thorough analysis of its Verbund structures in Ludwigshafen. This showed how to ensure the continuity of profitable businesses while making necessary adaptations. An overview of the major changes at the Ludwigshafen site:

- Closure of the caprolactam plant, one of the two ammonia plants and associated fertilizer facilities: The capacity of BASF’s caprolactam plant in Antwerp, Belgium, is sufficient to serve captive and merchant market demand in Europe going forward. High value-added products, such as standard and specialty amines and the Adblue® business, will be unaffected and will continue to be supplied via the second ammonia plant at the Ludwigshafen site.

- Reduction of the adipic acid production capacity and closure of the plants for cyclohexanol and cyclohexanone as well as soda ash: Adipic acid production at the joint venture with Domo in Chalampé, France, will remain unchanged and has sufficient capacity – in the changed market environment – to supply the business in Europe. Cyclohexanol and cyclohexanoneare precursors for adipic acid; the soda ash plant uses by-products of the adipic acid production. BASF will continue to operate the production plants for polyamide 6.6 in Ludwigshafen, which need adipic acid as a precursor.

- Closure of the TDI plant and the precursor plants for DNT and TDA: Demand for TDI has developed only very weakly especially in Europe, Middle East and Africa and has been significantly below expectations. The TDI complex in Ludwigshafen has been underutilized and has not met expectations in terms of economic performance. This situation has further worsened with sharply increased energy and utility costs. BASF’s European customers will continue to be reliably supplied with TDI from BASF’s global production network with plants in Geismar, Louisiana; Yeosu, South Korea; and Shanghai, China.

In total, 10 percent of the asset replacement value at the site will be affected by the adaptation of Verbund structures – and likely around 700 positions in production. Brudermüller stressed: “We are very confident that we will be able to offer most of the affected employees employment in other plants. It is very much in the company’s interest to retain their wide-ranging experience, especially since there are vacancies and many colleagues will retire in the next few years.” The measures will be implemented stepwise by the end of 2026 and are expected to reduce fixed costs by more than €200 million per year.

The structural changes will also lead to a significant reduction in the power and natural gas demand at the Ludwigshafen site. Consequently, CO2 emissions in Ludwigshafen will be reduced by around 0.9 million metric tons per year. This corresponds to a reduction of around 4 percent in BASF’s global CO2 emissions.

“We want to develop Ludwigshafen into the leading low-emission chemical production site in Europe,” said Brudermüller. BASF aims to secure greater supplies of renewable energy for the Ludwigshafen site. The company plans to make use of heat pumps and cleaner ways of generating steam. In addition, new CO2-free technologies, such as water electrolysis to produce hydrogen are to be implemented.

https://www.basf.com/global/en/media/news-releases/2023/02/p-23-131.html