The Urethane Blog

Everchem Updates

VOLUME XXI

September 14, 2023

Everchem’s exclusive Closers Only Club is reserved for only the highest caliber brass-baller salesmen in the chemical industry. Watch the hype video and be introduced to the top of the league: — read more

January 24, 2023

The owners of Universal Polymers Corporation (A division under General Coatings Manufacturing

Corporation) would like to announce appointment of Mr. Deepak Mittal as the new President of

Universal Polymers Corporation (UPC).

Deepak Mittal has been involved with the American Polymers Corporation for the last 34 years. He

held various leadership roles including President of Ultimate Linings from 2008-2017. Since 2017

he has been Executive Vice President at UPC helping it grow to be a large spray foam systems

house.

“I am honored and thrilled to be named President of UPC and to continue

the vision of our founder, Lax Gupta. It is an exciting time for UPC since we

are uniquely positioned as one of the few family-owned businesses to

remain in our industry. We currently have and are continuing to build an

extremely talented team who is focused on putting our customers first. UPC

is making continuous strides to offer the highest quality products in the

industry.” – Mittal

January 22, 2023

Leggett & Platt: Sturdy Foundation But Underwhelming Projections

Jan. 21, 2023 1:19 AM ETLeggett & Platt, Incorporated (LEG)2 Comments

Summary

- Leggett & Platt maintains a stable performance despite the softening of demand.

- Its liquidity stays decent, allowing it to sustain its capacity and potential headwinds.

- Projections may not be as exciting as they were in 2022.

- Dividend payments are enticing, given the growth and yield.

- The downward momentum of the stock price remains visible but acceptable.

With over a hundred years of existence, Leggett & Platt, Incorporated (NYSE:LEG) has been through a lot of crests and troughs. It has withstood various market challenges, making it a durable industry staple. In the last two years, it has stayed stable and flourishing amidst changing market dynamics.

Today, Leggett shows well-balanced growth and fundamental stability. The demand has softened, but revenues and margins are still manageable. Lower revenues may be anticipated as market demand cools down. Thankfully, furniture companies, including LEG, have already shown inventory recovery. Supply catches up with demand, so inventory management may become easier. Also, it maintains a decent liquidity position to suffice its operational capacity. It derives adequate core operating returns to cover borrowings. As such, it can sustain itself without raising its financial leverage further.

Moreover, the company remains consistent with dividend payments, making it one of the Dividend Champions. However, the stock price seems too high for fundamentals and does not reflect its intrinsic value.

Company Performance

The past two years had caused dramatic changes in the furniture and home furnishing industry. After suffering from pandemic disruptions that limited its operations, its performance spiked in just a year. It has remained an industry staple with solid market positioning. Thanks to lower prices, remote work setups, and the massive shift in consumer behavior. The real estate market boom also drove its growth. As more houses were bought, furniture and fixtures followed the trend. Today, Leggett & Platt keeps stable core operations amidst the current market patterns.

The operating revenue amounts to $1.3 billion, a 2% year-over-year decrease. Several factors contribute to this downtrend. First, the impact of inflation has been reflected. In 2022, we have seen how inflation peaked and set a new forty-year all-time high. It affected the purchasing power of many customers, especially in the US and Europe. Also, the skyrocketing fuel prices made it more challenging to transport raw materials and process products. Even more noticeable is that other countries reacted slower to inflation than the US. As we can see, the US inflation lull began in 3Q 2022. In Europe, inflation has just started to cool down. So the impact of the rising prices in LEG’s international markets remains keenly felt. It is not easy for consumers to adjust to price changes, putting downward pressure on the demand.

We can also attribute it to the cooling home demand. Home sales have slowed down in the last year. It has become more evident in the second half. In turn, the demand for furniture and home furnishings was impacted. Auto demand also showed a slowdown. Both these segments were vital for Leggett.

Despite this, Leggett now still exudes operational stability. It is an attribute an investor must watch. Indeed, it continues to stand the test of time. One way is through its pricing. It remains capable of making up for the lower demand by imposing strategic prices. These appear effective and flexible to market changes.

Moreover, LEG keeps concentrating on aspects it can manage and enhance. First, we can see it in its inventory adjustments. Supply chain bottlenecks have become one of its problems in the last two years. But we can now see a substantial improvement in its inventory levels. This move is in line with the market. It gives them increased flexibility in pricing and cost-reduction management. It has delivered its backlog, helping it through drastic business cycles. Its backlog delivery has been solid, but now, we can see its end. It is no wonder, the industry, including LEG, is starting to return to a normal business flow. Supply is catching up with market demand, so the company is regaining its stride. Although sales are lower, its supply chains are improving. It will help the company maintain a balance in revenue and margin stability.

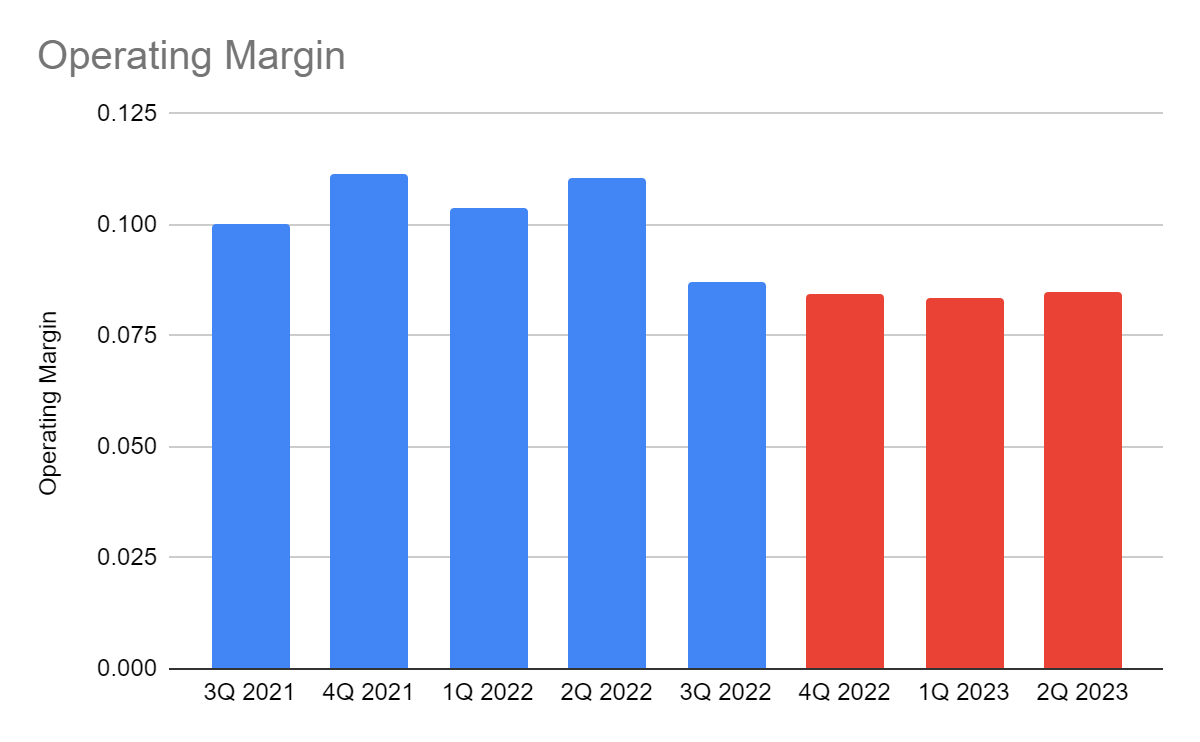

Meanwhile, operating costs and expenses are well-managed despite the high-flying prices. The efficiency of the company is helping it partially offset the revenue decrease. Although it is insufficient, the core operations remain stable and viable. Despite some demand slowdowns, the swift supply chain recovery helps enhance operational efficiency. The operating margin is relatively weaker in sequential values. But it stays decent at 8.7%, down from 10% in the comparative quarter.

This year, I expect more normality in business flows. Seasonality may also return and become a prevalent factor. Near-term performance may not be as robust as in 2021 and 2022, but stability may remain. As the inflation lull continues, producing, transporting, and transporting raw materials and finished products may be less expensive. As LEG regains a grasp of its supply chains, it may keep improving its cost-reduction strategies. It may be more agile in setting optimal prices. I expect growth to cool down, but core operations may stay manageable. I also expect the first-half revenues to decrease more. Even so, expect the operating margin to stay near its current level as costs and expenses decrease. It is a combination of lower inflation and the production volume adjustment of Leggett & Platt. But it may have to work more on advertising to secure its place in the market.

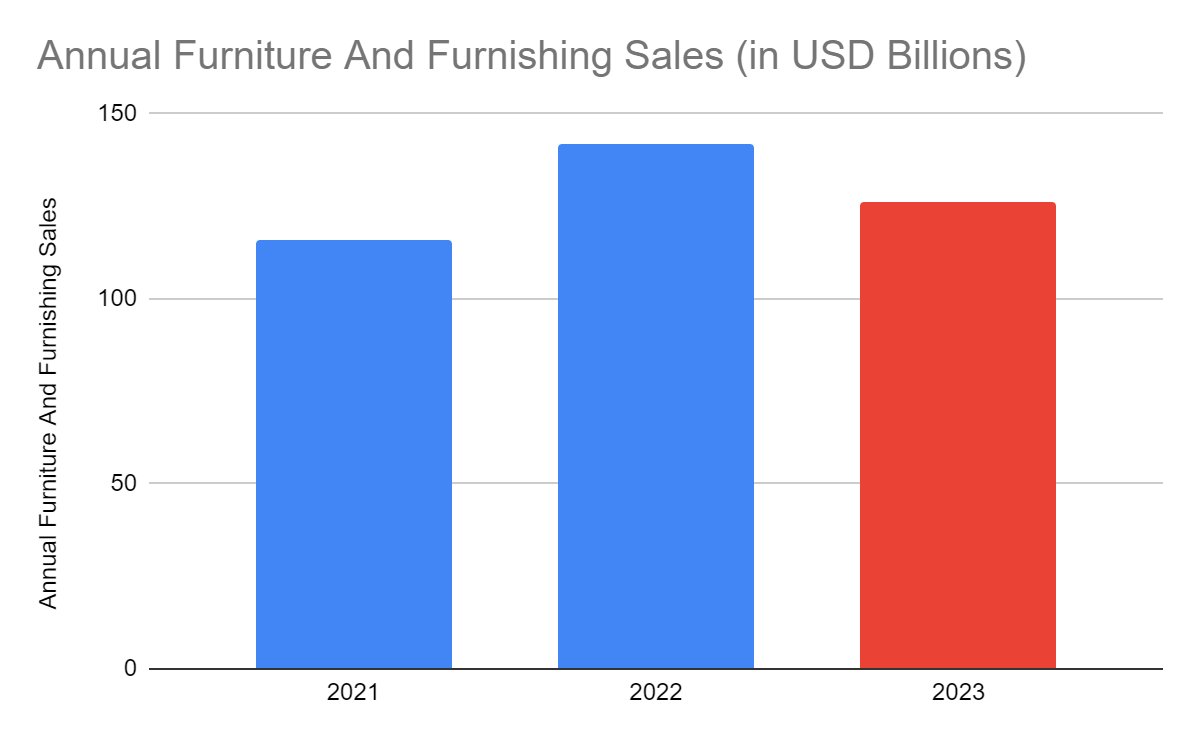

What’s important is that LEG stays consistent with the market trend. As of this writing, the 2022 US furniture and home furnishing sales are 1.6% higher than in 2021. November and December sales are not included yet, so the total value may reach $142 billion. Despite this, the recent market demand and volume trend are in a downtrend and may persist in 2023. Its value may decrease further this year but may stay elevated. But of course, LEG and the whole market must not be complacent. The increased presence of smaller retailers and the rise of e-commerce may become other hurdles.

How Leggett & Platt Can Sustain Its Operations

Leggett & Platt has always been one of the most indelible figures in the industry. In its long existence, it has maintained operational stability, making it a secure investment. Yet, market dynamics are changing and may become underwhelming this year. The consolation we have now is that inflation keeps decreasing, so I expect interest rate increments to cool down. I am not discounting the potential recession, though. Despite this, I am more optimistic since the recent changes are part of economic recovery. The unemployment rate remains manageable and low. Income levels are higher today. Business reopenings and capital inflows may continue.

But what makes LEG durable despite the underwhelming expectations is its market and financial positioning. The decreasing inventory level can help it cope with cooling demand. It can help improve operational efficiency to stabilize margins. Even better, it maintains adequate cash levels. The only worry we have now is the substantial increase in borrowings. It is still understandable since interest rate hikes make borrowing costs higher. But it must be more careful to maintain adequate liquidity. Thankfully, the company is still earning enough to cover borrowings. The Net Debt/EBITDA Ratio remains acceptable at 3.7x. It is lower than the maximum ratio of 4x, especially since LEG is a capital-intensive company.

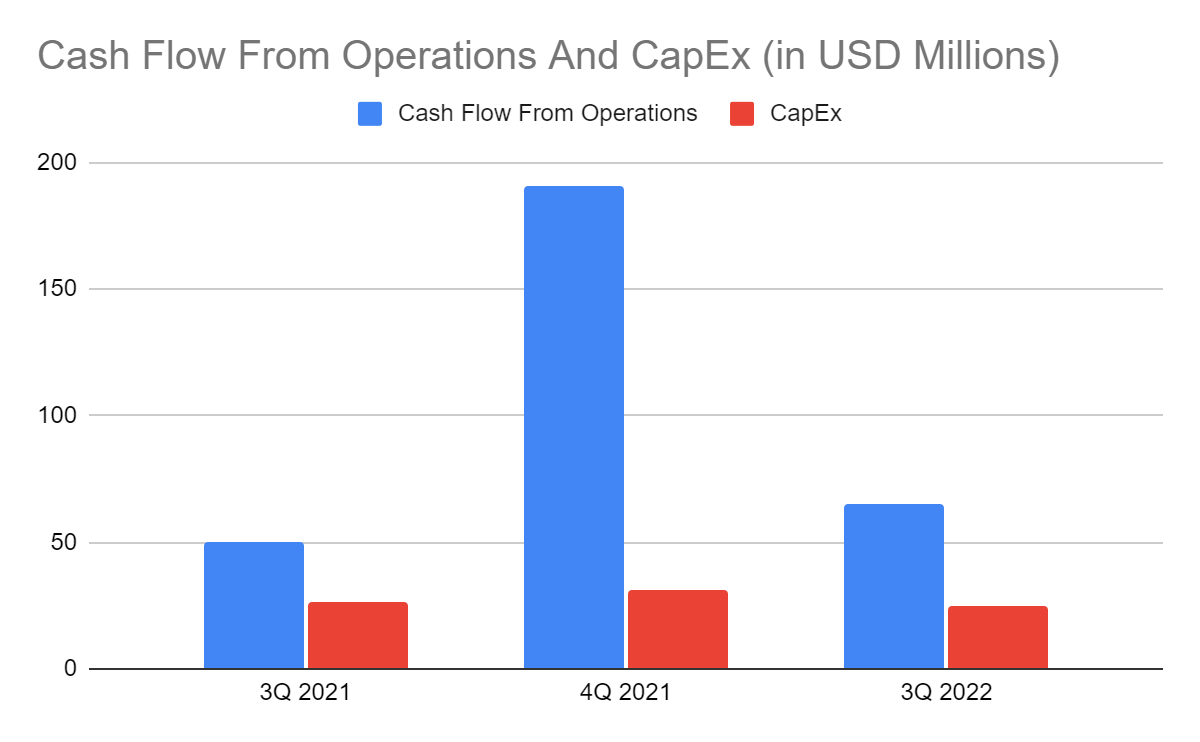

The cash flow of the company can confirm its liquidity. Its operating cash flow of $65 million is more than twice as much as its CapEx of $24 million. With that, it has a remaining amount of $41 million. Its FCF can repay near-term borrowings and dividends. It also has enough cash to preserve its intrinsic value by repurchasing shares.

Stock Price

The stock price of Leggett & Platt remains in a downtrend. It does not convey any upside or reversal potential. At $33.46, it remains 11% lower than its value last year. But it appears reasonable as some price metrics show. Using the current price-earnings multiple of 12.7x and my estimated EPS of $2.32, the target price is $29.46. NASDAQ has a more optimistic view with an estimated EPS of $2.36, but the target price is still low at $29.97. There may be a 10-12% potential downside. The estimation using the EV Model ($6.64 B – $2.51 B) / 132,619,000 shares agrees with it with $31.37 as the target price.

Meanwhile, dividends stay enticing with yields of 5.15%. It is way better than and more than thrice as much as the S&P 400 average of 1.54%. What’s more interesting is its consistent dividend growth for about fifty years, making it a part of the Dividend Champions. The only concern we have is its Dividend Payout Ratio of 74%. To assess the stock price better, we will use the DCF Model.

FCFF $299,000,000

Cash $226,000,000

Borrowings $2,820,000,000

Perpetual Growth Rate 4.8%

WACC 9.2%

Common Shares Outstanding 132,619,000

Stock Price $33.46

Derived Value $31.68

Bottomline

Leggett & Platt remains a secure and stable company. Growth may not be exciting but fundamental soundness remains evident. Dividend payments are consistent with high yields while staying well-covered. However, the stock price remains in a downtrend but still appears overvalued. The recommendation, for now, is that Leggett & Platt is a hold.

This article was written by

Investigating The Stock Market

770 Followers

January 20, 2023

December trailer orders 2nd highest on record

Catch-up of suppressed orders skews bookings in last month of 2022

· Thursday, January 19, 2023

Listen to this article

0:00 / 2:52BeyondWords

Trailer manufacturers posted 57,300 orders in December, the second-highest monthly intake since ACT Research began tracking in 1996. The volume appeared to be a catch-up after OEMs blocked many orders from April to August because they lacked pricing visibility.

“I cannot speak for other OEMs. However, our higher booking in December was driven by the later opening of the order books as we awaited required quoting information from the supply base,” Sean Kenney, chief sales officer for Hyundai Translead, told FreightWaves.

“Hyundai Translead is anticipating continued higher-than-normal orders for the next few months as we work through the impact of this.”

December net U.S. trailer orders came in 46% higher compared to November and 115% above December 2021, ACT Research reported. The highest month on record was September 2018, with 57,800 net orders.

Some manufacturers report that the supply of parts has deteriorated despite their acceptance of the huge number of December orders.

Lingering supply chain concerns for future trailer orders

“Supply-chain concerns still linger,” with no short-term improvement in sight, Jennifer McNealy, ACT director of commercial vehicle market research and publications, said in a news release. “Regarding demand, most trailer makers continue to see demand exceeding capacity through the end of 2023.”

One major OEM, Wabash, announced a long-term supply agreement Jan. 10 with J.B. Hunt Transport covering up to 15,000 trailers over the next few years.

Some OEMs mentioned an erosion in confidence to ACT, but so far it is not showing up in order cancellations.

Mike Baudendistel, a FreightWaves market expert, expressed surprise at the order volume in December.

“It could be some makeup orders to compensate for the supply constraints the past couple years,” he said. “I would think the orders were even more heavily weighted toward the large enterprise carriers than they usually are since they are well capitalized and their business holds up better in a weakening market.”

Total net orders placed in 2022 were 361,500 compared to 249,400 in 2021. The industry produced approximately 306,000 trailers in 2022.

“Our projections point to a continuation of that upward trend into 2023,” McNealy said.

January 19, 2023

Covestro names new president and chairman for US operations

In This Article

By Paul J. Gough – Reporter, Pittsburgh Business Times

Jan 18, 2023

Listen to this article 2 min

Covestro LLC has named Samir Hifri as chairman and president leading the company’s U.S. operations and replacing the retiring Haakan Jonsson on July 1.

Covestro, with its U.S. headquarters off the Parkway West, has 2,800 employees in the United States.

Hifri, a graduate of Duquesne University, joined Covestro in 1998 as a commercial trainee at the headquarters in Pittsburgh. He is now SVP and managing director of Covestro Hong Kong and leads the Asia Pacific Supply Chain & Logistics company for the polymers manufacturer. He has worked at 10 sites and six countries for Covestro over the past more than two decades.

“With his passion for people, deep knowledge of Covestro’s global business and strong ties to America, Samir is well suited to lead the U.S. organization into the future,” said Covestro CFO Thomas Toepfer.

Jonsson joined Covestro in 1992 and became chairman and president in January 2020. He has also integrated the DSM resins and functional materials acquisition into Covestro and started the Covestro Circular Economy Program at the University of Pittsburgh. He is a C-Suite Award winner from the Pittsburgh Business Times in 2022.

“Haakan steered the U.S. organization through one of the most challenging and transformative periods in our history, while continuing to foster a more diverse, inclusive and innovative culture,” Toepfer said.

January 18, 2023

BASF Group releases preliminary figures for full year 2022

- Expected sales of €87,327 million and expected EBIT before special items of €6,878 million at the level of average analyst estimates

- EBIT expected to be €6,548 million, below analyst consensus due to non-cash-effective impairments

- Net income expected to be –€1,376 million due to non-cash-effective impairments on the shareholding in Wintershall Dea, below analyst consensus

Ludwigshafen – January 17, 2023 – BASF has released preliminary figures for the full year 2022. Expected sales of €87,327 million and expected income from operations (EBIT) before special items of €6,878 million are in line with the ranges forecast by BASF and at the level of average analyst estimates for 2022.

The BASF Group’s EBIT amounted to an expected €6,548 million in 2022, below the figure for the prior year (2021: €7,677 million) and below analyst consensus for 2022 (Vara: €6,836 million). This includes non-cash-effective impairments on a plant in the Chemicals segment.

Net income of BASF Group is expected to amount to –€1,376 million in 2022. This is considerably below the prior-year figure (2021: €5,523 million) and the average analyst estimates for 2022 (Vara: €4,768 million). Net income contains non-cash-effective impairments on the shareholding in Wintershall Dea AG in the amount of about €7.3 billion, of which €5.4 billion in Q4 2022. These impairments result in particular from the deconsolidation of the Russian exploration and production activities of Wintershall Dea due to the extensive loss of actual influence and economic expropriation. Wintershall Dea intends to fully exit Russia in an orderly manner complying with all applicable legal obligations. Accordingly, the Russian participations of Wintershall Dea have been re-evaluated and write-downs on the European gas transportation business have been made, including a complete write-down on the participation in Nord Stream AG.

Sales rose by 11 percent in 2022 to an expected €87,327 million (2021: €78,598 million) and were thus in line with the €86 billion to €89 billion range forecast by BASF. The average analyst estimates for sales 2022 of the BASF Group were €87,950 million according to Vara. The increase in sales was mainly driven by higher prices and positive currency effects. Volumes reduced sales.

EBIT before special items amounted to an expected €6,878 million, a decrease of €890 million compared with the prior year (2021: €7,768 million) and in line with the €6.8 billion to €7.2 billion range forecast by BASF. On average analysts had expected EBIT before special items of €6,949 million in 2022 according to Vara.

The average analyst estimates for EBIT before special items of the segments were exceeded in 2022 by Agricultural Solutions and Surface Technologies. EBIT before special items of Materials and Industrial Solutions almost matched average analyst estimates. EBIT before special items fell short of average analyst estimates in the Nutrition & Care and Chemicals segments. In Other, EBIT before special items was better than expected by analysts on average.